International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 4 (April 2025), Pages: 193-199

----------------------------------------------

Original Research Paper

Noise trader risk and its effect on market volatility: Evidence from Vietnam’s stock market

Author(s):

Affiliation(s):

1School of Banking and Finance, National Economics University, Hanoi, Vietnam

2School of Advanced Education Program, National Economics University, Hanoi, Vietnam

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0003-0170-8636

Corresponding author's ORCID profile: https://orcid.org/0000-0003-0170-8636

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.04.021

Abstract

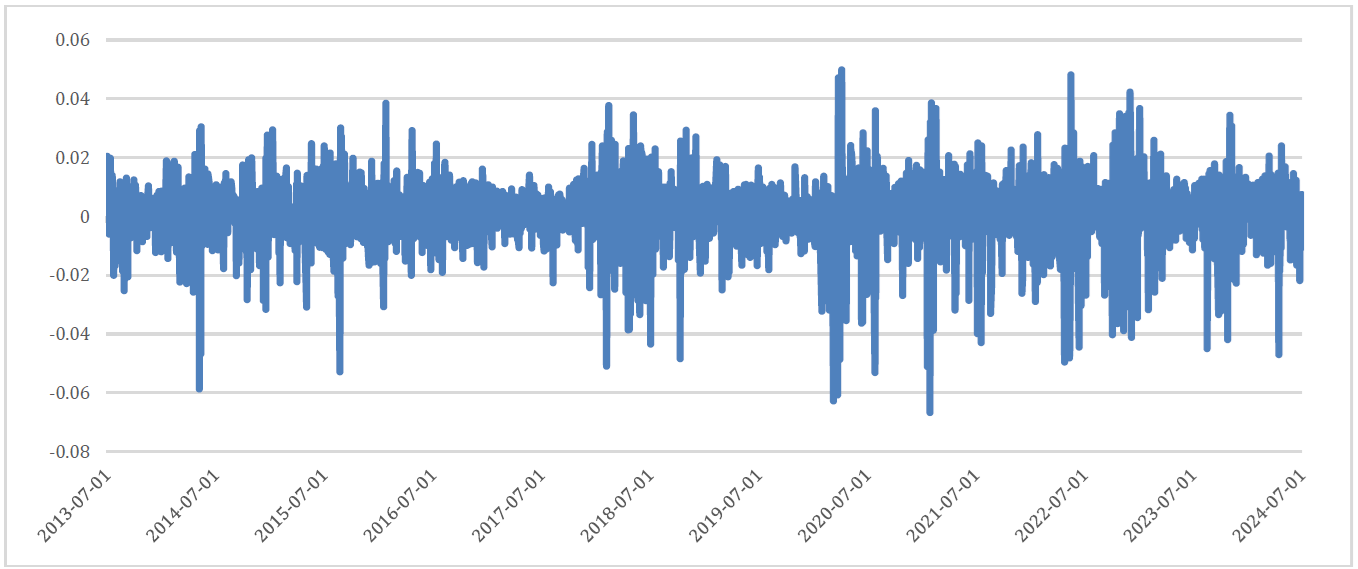

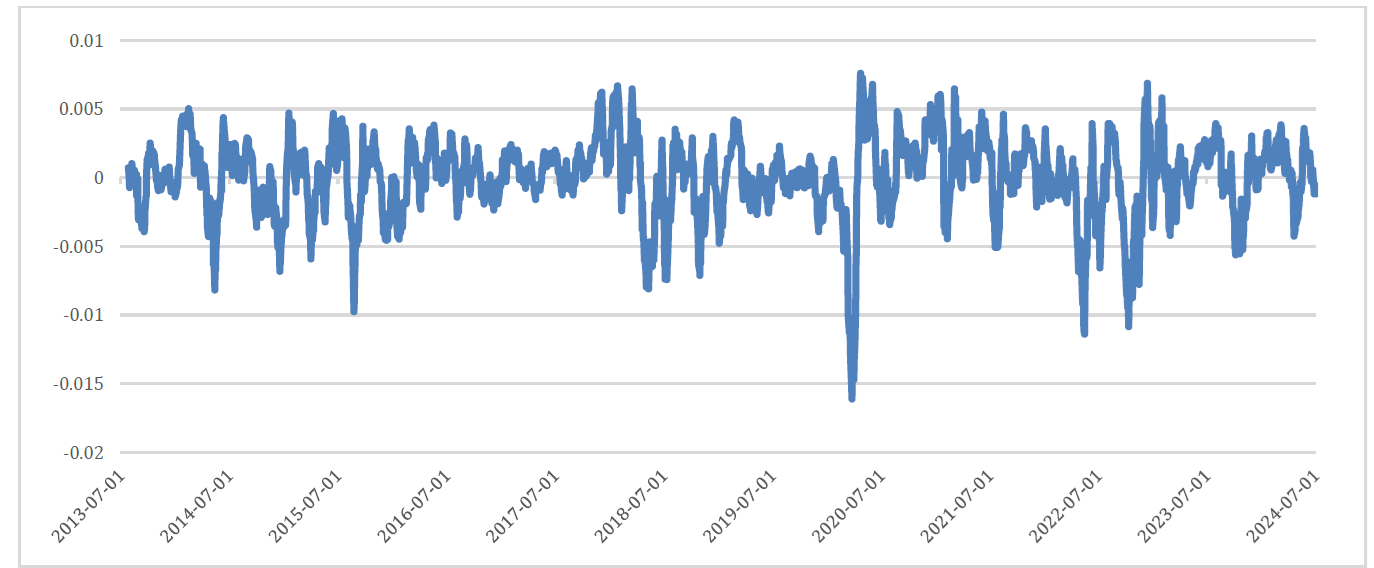

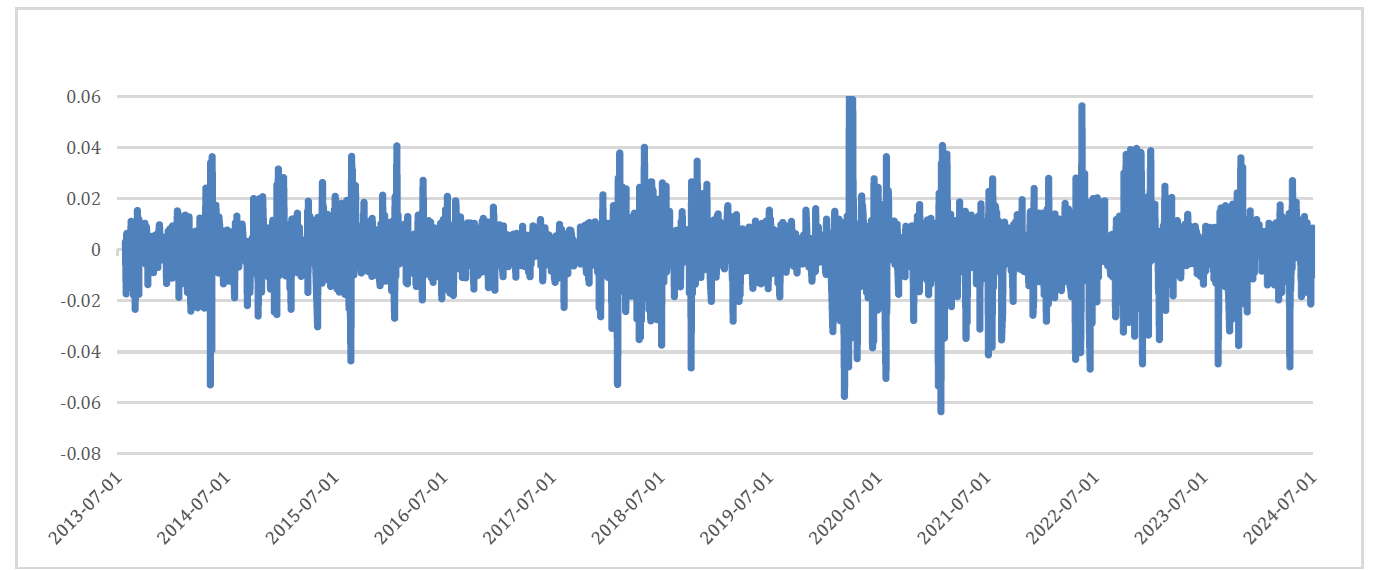

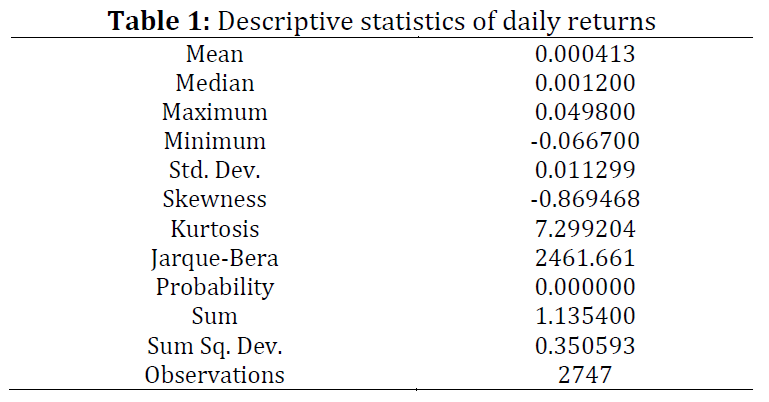

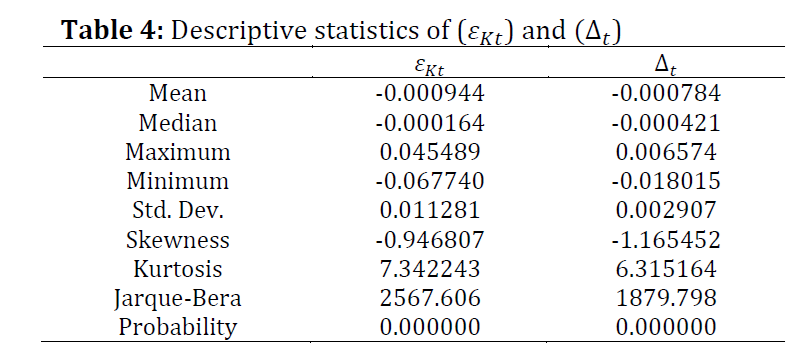

This study examines the presence of noise trader risk in Vietnam’s stock market and its impact on daily stock returns. The research employs GARCH (1,1), EGARCH, and PGARCH models to filter residuals, followed by a moving average approach to measure the effect of informed traders. Noise trader risk, defined as the risk arising from irrational traders, is calculated by subtracting the influence of rational traders from the residuals. The results show that noise trader risk exists in Vietnam’s stock market, but its effect on daily returns is unpredictable. In contrast, informed traders have a positive impact on stock returns, helping to correct market prices toward their fundamental values.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Noise trader risk, Stock market returns, GARCH models, Market efficiency, Investor behavior

Article history

Received 13 November 2024, Received in revised form 13 April 2025, Accepted 26 April 2025

Acknowledgment

This research is funded by the National Economics University, Hanoi, Vietnam.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Pham TD and Pham DK (2025). Noise trader risk and its effect on market volatility: Evidence from Vietnam’s stock market. International Journal of Advanced and Applied Sciences, 12(4): 193-199

Figures

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (18)

- Black F (1986). Noise. The Journal of Finance, 41(3): 528–543. https://doi.org/10.1111/j.1540-6261.1986.tb04513.x [Google Scholar]

- Campbell JY and Kyle AS (1993). Smart money, noise trading and stock price behaviour. The Review of Economic Studies, 60(1): 1–34. https://doi.org/10.2307/2297810 [Google Scholar]

- De Long JB, Shleifer A, Summers LH, and Waldmann RJ (1990). Noise trader risk in financial markets. Journal of Political Economy, 98(4): 703–738. https://doi.org/10.1086/261703 [Google Scholar]

- Dhameja SK (2019). Measurement of time varying volatility and its relation with noise trading: A study on Indian stock market using GARCH model. Research Journal of Humanities and Social Sciences, 10(2): 479-483. https://doi.org/10.5958/2321-5828.2019.00079.2 [Google Scholar]

- Feng J, Lin DP, and Yan XB (2014). Research on measure of noise trading in stock market based on EGARCH-m model. In the International Conference on Management Science and Engineering 21 st Annual Conference Proceedings, IEEE, Helsinki, Finland: 1183-1189. https://doi.org/10.1109/ICMSE.2014.6930363 [Google Scholar]

- Flynn SM (2012). Noise-trading, costly arbitrage, and asset prices: Evidence from us closed-end funds. Journal of Financial Markets, 15(1): 108-125. https://doi.org/10.1016/j.finmar.2011.06.001 [Google Scholar]

- Inuduka T, Yokose A, and Managi S (2024). Noise trader impact: Bitcoin market evidence from Telegram and X. Social Network Analysis and Mining, 14(1): 189. https://doi.org/10.1007/s13278-024-01350-6 [Google Scholar]

- Koski JL, Rice EM, and Tarhouni A (2004). Noise trading and volatility: Evidence from day trading and message boards. https://dx.doi.org/10.2139/ssrn.533943 [Google Scholar]

- Podolski–Boczar E, Kalev PS, and Duong HN (2009). Deafened by noise: do noise traders affect volatility and returns? Working Paper, Monash University, Clayton, Australia. https://doi.org/10.1007/s13278-024-01350-6 [Google Scholar]

- Qiang Z and Shu-e Y (2009). Noise trading, investor sentiment volatility, and stock returns. Systems Engineering-Theory and Practice, 29(3): 40-47. https://doi.org/10.1016/S1874-8651(10)60010-5 [Google Scholar]

- Ryan N, Ruan X, Zhang JE, and Zhang JA (2021). Choosing factors for the Vietnamese stock market. Journal of Risk and Financial Management, 14(3): 96. https://doi.org/10.3390/jrfm14030096 [Google Scholar]

- Schneider M and Nunez M (2024). A decision theoretic foundation for noise traders and correlated speculation. Decision Analysis, 21(1): 4-22. https://doi.org/10.1287/deca.2023.0473 [Google Scholar]

- Scruggs JT (2007). Noise trader risk: Evidence from the Siamese twins. Journal of Financial Markets, 10(1): 76-105. https://doi.org/10.1016/j.finmar.2006.04.002 [Google Scholar]

- Shefrin H and Statman M (1994). Behavioral capital asset pricing theory. Journal of Financial and Quantitative Analysis, 29(3): 323-349. https://doi.org/10.2307/2331334 [Google Scholar]

- Sias RW, Starks LT, and Tiniç SM (2001). Is noise trader risk priced? Journal of Financial Research, 24(3): 311-329. https://doi.org/10.1111/j.1475-6803.2001.tb00772.x [Google Scholar]

- Sinha DPC (2015). Dynamics of noise traders’ risk in the NSE and BSE markets. International Journal of Financial Management, 5(4): 36-64. https://doi.org/10.21863/ijfm/2015.5.4.021 [Google Scholar]

- Truong LD, Friday HS, and Nguyen ATK (2022). The effects of index futures trading volume on spot market volatility in a frontier market: Evidence from Ho Chi Minh stock exchange. Risks, 10(12): 234. https://doi.org/10.3390/risks10120234 [Google Scholar]

- Verma R and Verma P (2007). Noise trading and stock market volatility. Journal of Multinational Financial Management, 17(3): 231-243. https://doi.org/10.1016/j.mulfin.2006.10.003 [Google Scholar]