International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 11, Issue 8 (August 2024), Pages: 119-126

----------------------------------------------

Original Research Paper

Forecasting Kenya's public debt using time series analysis

Author(s):

Affiliation(s):

Department of Mathematics and Statistics, University of Embu, Embu, Kenya

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0009-0009-1692-4893

Corresponding author's ORCID profile: https://orcid.org/0009-0009-1692-4893

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2024.08.013

Abstract

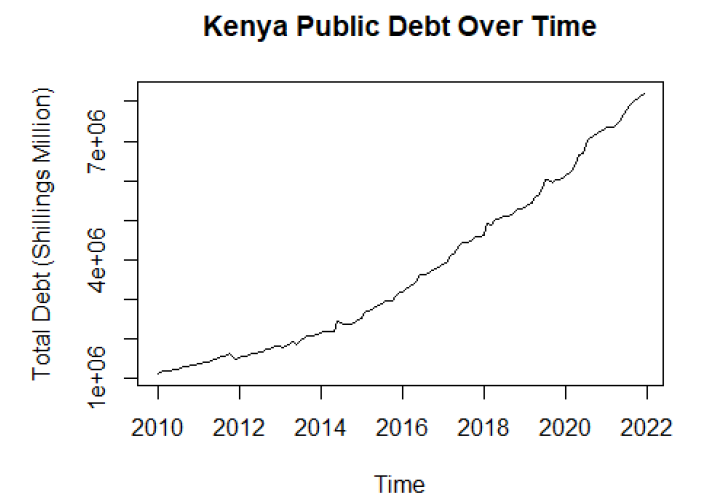

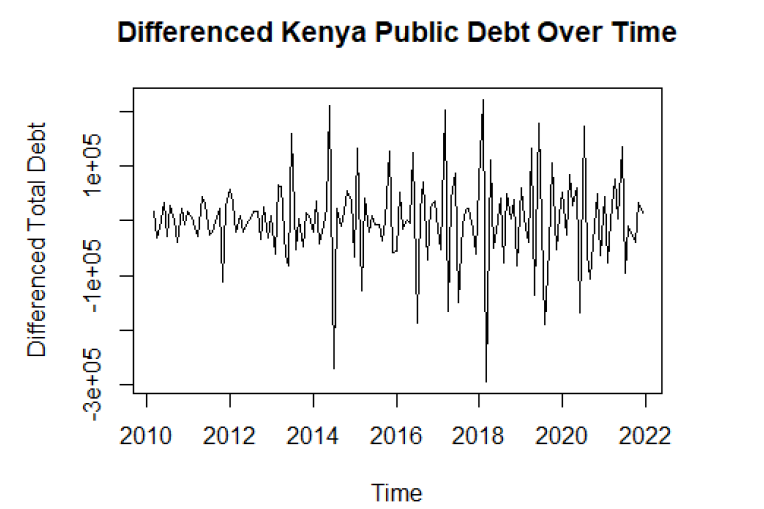

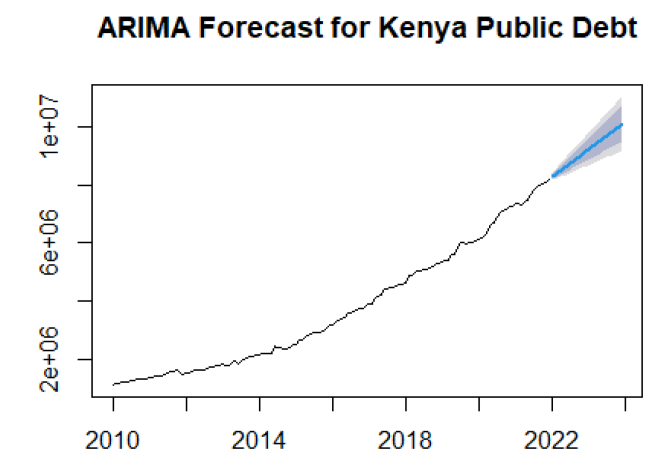

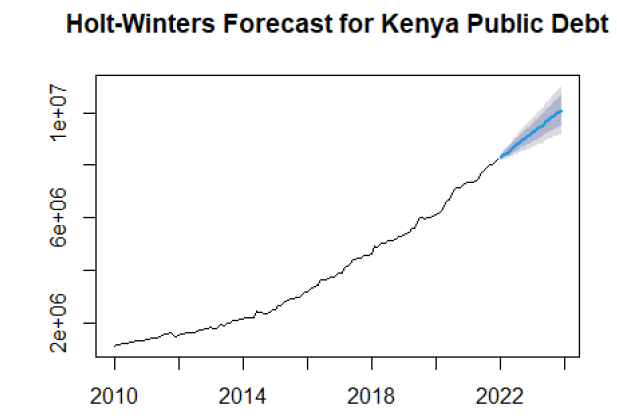

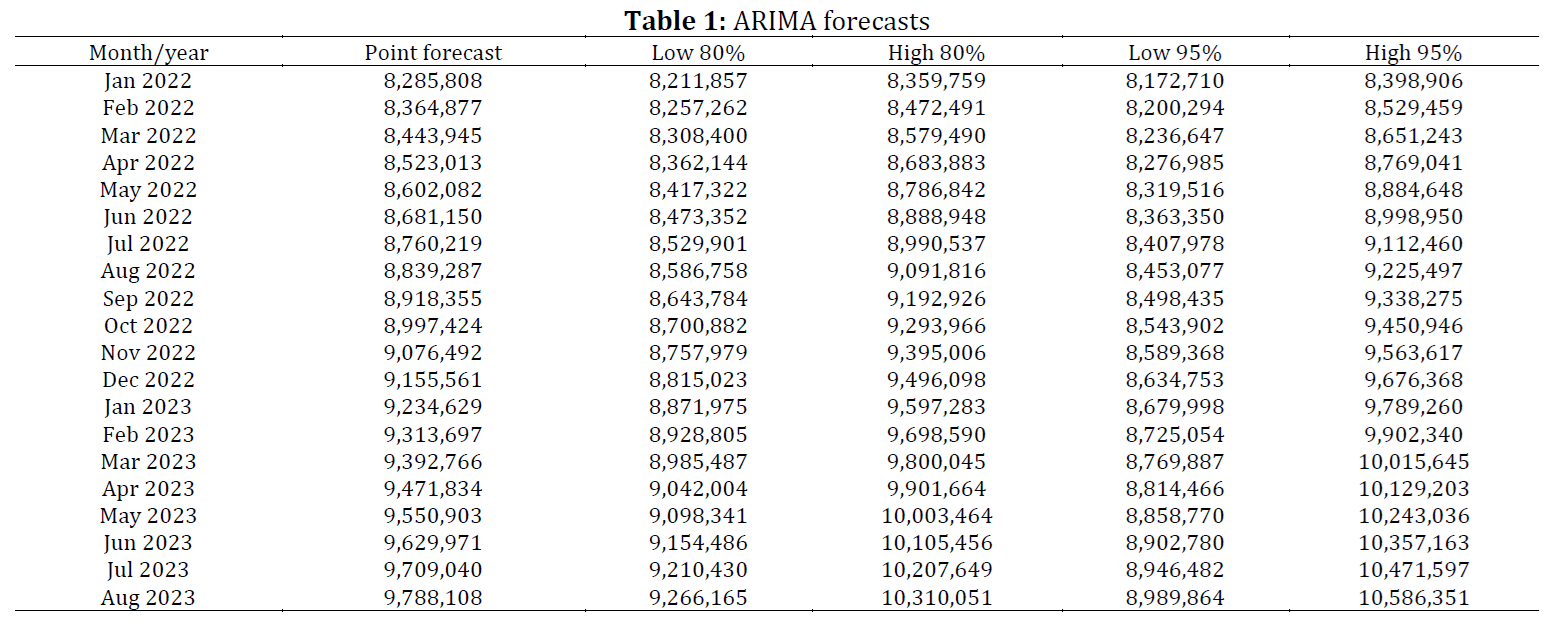

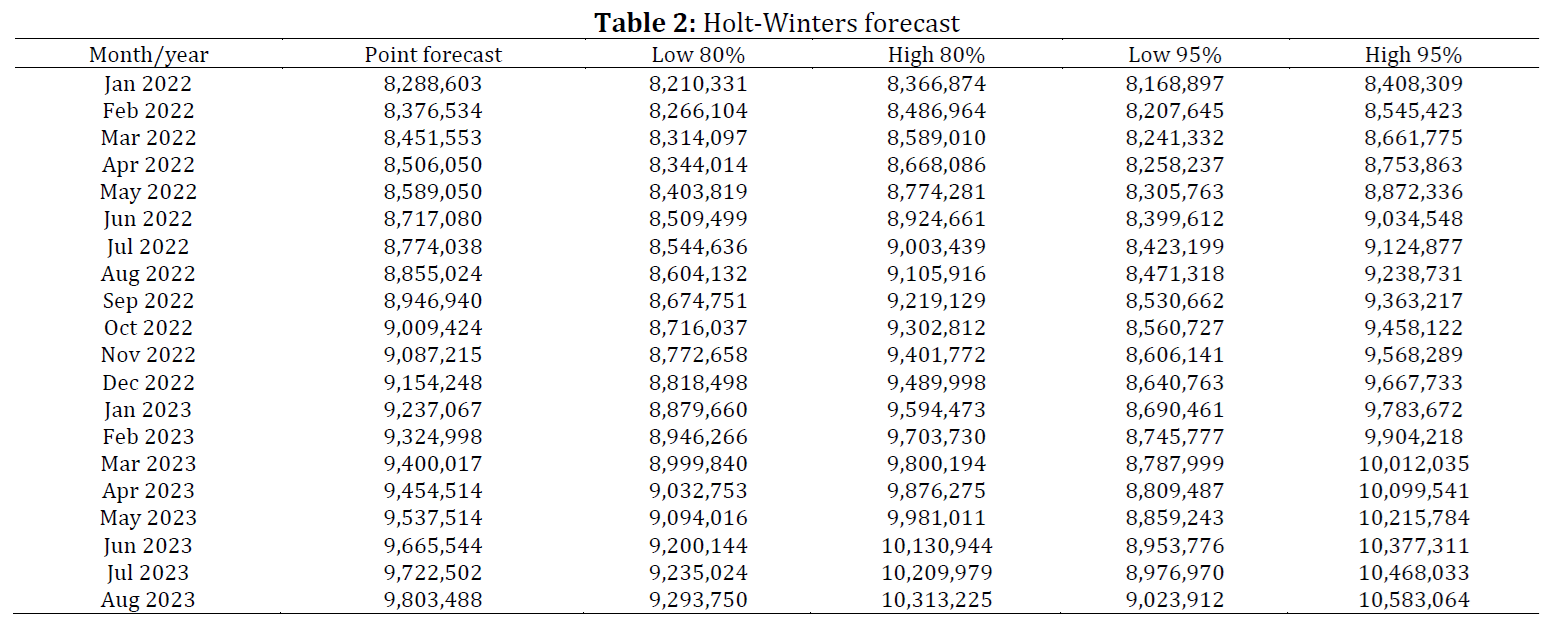

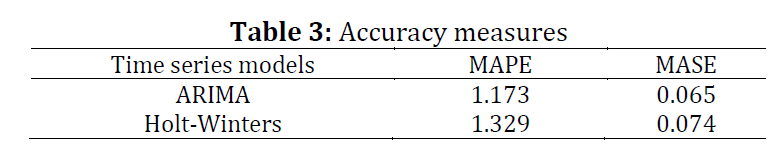

Accurately forecasting public debt is essential for developing countries like Kenya to maintain fiscal sustainability and economic stability. This study aimed to identify the best time series forecasting model for predicting Kenya's future public debt to help policymakers create effective fiscal reforms. The Autoregressive Integrated Moving Average (ARIMA) and Holt-Winters exponential smoothing models were tested due to their ability to handle complex patterns and seasonality in time series data. Public debt data from Kenya from 2001 to 2021 were analyzed, and both models were applied to the processed data. The ARIMA (0,2,1) model, which uses second-order differencing and a moving average component, was found to be the best model based on information criteria. The Holt-Winters additive method also showed good performance, adapting well to recent data and seasonal trends with optimized smoothing parameters. Both models produced forecasts that closely matched the actual debt figures for 2022 and 2023, with an error margin of only 0.73. Measures of accuracy, such as Mean Absolute Percentage Error (MAPE) and Mean Absolute Scaled Error (MASE), confirmed the reliability of the models, with ARIMA performing slightly better than Holt-Winters. While previous studies have looked at debt forecasting for Kenya, this research offers a thorough evaluation and comparison of two strong time series models. Unlike existing literature, this study provides a rigorous out-of-sample forecasting assessment, identifying the best approach for reliably predicting Kenya's debt. However, the study is limited by its focus on univariate time series models, which could be improved by including relevant external economic variables. The findings show that the ARIMA and Holt-Winters models are accurate tools for forecasting Kenya's public debt, helping policymakers to develop sustainable debt management strategies and fiscal reforms based on reliable future projections.

© 2024 The Authors. Published by IASE.

This is an

Keywords

Public debt forecasting, Fiscal sustainability, ARIMA model, Holt-Winters method, Time series analysis

Article history

Received 20 February 2024, Received in revised form 23 June 2024, Accepted 3 August 2024

Acknowledgment

We thank the Central Bank of Kenya (CBK) for giving free access to these high-quality historical data, which provided a solid modeling basis.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Keraro OF, Morris ZN, Kitavi DM, and Wanyonyi M (2024). Forecasting Kenya's public debt using time series analysis. International Journal of Advanced and Applied Sciences, 11(8): 119-126

Figures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (29)

- Barro RJ (1979). On the determination of the public debt. Journal of Political Economy, 87(5, Part 1): 940–971. https://doi.org/10.1086/260807 [Google Scholar]

- Box GEP, Jenkins GM, and Reinsel GC (1970). Time series analysis: Forecasting and control. 4th Edition, John Wiley and Sons, Hoboken, USA. [Google Scholar]

- Dassanayake W, Ardekani I, Jayawardena C, Sharifzadeh H, and Gamage N (2019). Forecasting accuracy of Holt-Winters exponential smoothing: Evidence from New Zealand. New Zealand Journal of Applied Business Research, 17(1): 11-30. [Google Scholar]

- Dinh DV (2020). Forecasting domestic credit growth based on ARIMA model: Evidence from Vietnam and China. Management Science Letters, 10(5): 1001-1010. https://doi.org/10.5267/j.msl.2019.11.010 [Google Scholar]

- Djakaria I, and Saleh SE (2021). COVID-19 forecast using Holt-Winters exponential smoothing. Journal of Physics: Conference Series, 1882(1): 012033. https://doi.org/10.1088/1742-6596/1882/1/012033 [Google Scholar]

- Filatova H and Aiyedogbon JO (2020). Government debt forecasting based on the ARIMA model. Public and Municipal Finance, 8(1): 120-127. https://doi.org/10.21511/pmf.08(1).2019.11 [Google Scholar]

- Gechore DO, Atitwa EB, Kimani P, and Wanyonyi M (2022). Predicting the number of tourists in-flow to Kenya using seasonal autoregressive integrated moving average model. African Journal of Hospitality, Tourism and Leisure, 11(6): 1913-1923. [Google Scholar]

- Habibur Rahman M, Salma U, Moyazzem Hossain M, and Tareq Ferdous Khan M (2016). Revenue forecasting using Holt–Winters exponential smoothing. Research and Reviews: Journal of Statistic, 5(3): 19-25. [Google Scholar]

- Kinyili M and Wanyonyi M (2021). Forecasting of COVID-19 deaths in South Africa using the autoregressive integrated moving average time series model. General Letters in Mathematics, 11(2): 26-35. https://doi.org/10.31559/glm2021.11.2.2 [Google Scholar]

- Kithure ME (2021). Use of time series models on forecasting of value added tax revenue in Kenya revenue authority. African Tax and Customs Review, 4(2): 22-22. [Google Scholar]

- Machagua J and Naikumi M (2023). Effect of external public debt on private investments in Kenya. Kenya Institute for Public Policy Research and Analysis, Nairobi, Kenya. [Google Scholar]

- Makatjane KD and Moroke ND (2016). Comparative study of Holt-Winters triple exponential smoothing and seasonal ARIMA: Forecasting short term seasonal car sales in South Africa. Journal of Chemical Information and Modeling, 6(1): 1689– 1699. https://doi.org/10.22495/rgcv6i1art8 [Google Scholar]

- Makau J, Ocharo K, and Njuru S (2018). Fiscal policy and public debt in Kenya. IOSR Journal of Economics and Finance, 9(5): 12–24. [Google Scholar]

- Maurice W, Kitavi DM, Mugo DM, and Atitwa EB (2021). COVID-19 prediction in Kenya using the ARIMA model. International Journal of Electrical Engineering and Technology, 12(8): 105-114. [Google Scholar]

- Mini KG, Kuriakose S, and Sathianandan TV (2015). Modeling CPUE series for the fishery along northeast coast of India: A comparison between the Holt-Winters, ARIMA and NNAR models. Journal of the Marine Biological Association of India, 57(2): 75-82. [Google Scholar]

- Mohamedamin AH (2021). The effect of national public debt on economic growth in Kenya. Ph.D. Dissertation, University of Nairobi, Nairobi, Kenya. [Google Scholar]

- Montgomery D, Jennings C, and Kulahci M (2008). Introduction to time series analysis and forecasting. 5th Edition, John Wiley and Sons, Hoboken, USA. [Google Scholar]

- Motonu JO, Waititu AG, and Mung’atu JK (2016). Modeling extremal events: A case study of the Kenyan public debt. American Journal of Theoretical and Applied Statistics, 5: 334-341. https://doi.org/10.11648/j.ajtas.20160506.11 [Google Scholar]

- Mutunga PM (2020). Public debt and its implication on Kenya’s future economic growth. International Journal of Research and Innovation in Social Science, 4(8): 218-223. [Google Scholar]

- Mutwiri RM (2019). Forecasting of tomatoes wholesale prices of Nairobi in Kenya: Time series analysis using SARIMA model. International Journal of Statistical Distributions and Applications, 5(3): 46–53. https://doi.org/10.11648/j.ijsd.20190503.11 [Google Scholar]

- Mwaniki GW (2016). Effect of public debt on the gross domestic product in Kenya. Journal of Economics and Finance, 7(6): 59–72. [Google Scholar]

- Njoroge L (2020). Impact of Kenya’s public debt on economic stability. Ph.D. Dissertation, Walden University, Minneapolis, USA. [Google Scholar]

- Nyaga RK and Ng’ang’a JC (2015). Forecasting Kenya’s manufacturing output with time series data. Journal of Business and Entrepreneurship, 27(1): 131-153. [Google Scholar]

- Omane-Adjepong M, Oduro FT, and Oduro SD (2013). Determining the better approach for short-term forecasting of Ghana’s inflation: Seasonal-ARIMA vs Holt-Winters. International Journal of Business, Humanities and Technology, 3(1): 69–79. [Google Scholar]

- Qader MR, Khan S, Kamal M, Usman M, and Haseeb M (2021). Forecasting carbon emissions due to electricity power generation in Bahrain. Environmental Science and Pollution Research, 29: 17346-17357. https://doi.org/10.1007/s11356-021-16960-2 [Google Scholar]

- Salles R, Belloze K, Porto F, Gonzalez PH, and Ogasawara E (2019). Nonstationary time series transformation methods: An experimental review. Knowledge-Based Systems, 164: 274-291. https://doi.org/10.1016/j.knosys.2018.10.041 [Google Scholar]

- Siddiqui R, Azmat M, Ahmed S, and Kummer S (2022). A hybrid demand forecasting model for greater forecasting accuracy: The case of the pharmaceutical industry. Supply Chain Forum: An International Journal, 23(2): 124-134. https://doi.org/10.1080/16258312.2021.1967081 [Google Scholar]

- Tofallis C (2015). A better measure of relative prediction accuracy for model selection and model estimation. Journal of the Operational Research Society, 66: 1352-1362. https://doi.org/10.1057/jors.2014.103 [Google Scholar]

- Verma P, Reddy SV, Ragha L, and Datta D (2021). Comparison of time-series forecasting models. In the International Conference on Intelligent Technologies, IEEE, Hubli, India: 1-7. https://doi.org/10.1109/CONIT51480.2021.9498451 [Google Scholar]