International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 11, Issue 7 (July 2024), Pages: 226-236

----------------------------------------------

Original Research Paper

The influence of auditor ethics on audit quality: Analyzing key factors in Vietnamese audit firms

Author(s):

Affiliation(s):

1Faculty of Business and Economics, Phenikaa University, Yen Nghia, Ha Dong, Hanoi 12116, Vietnam

2Faculty of Accounting and Auditing, Thuongmai University, Hanoi, Vietnam

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0009-0003-6330-6699

Corresponding author's ORCID profile: https://orcid.org/0009-0003-6330-6699

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2024.07.025

Abstract

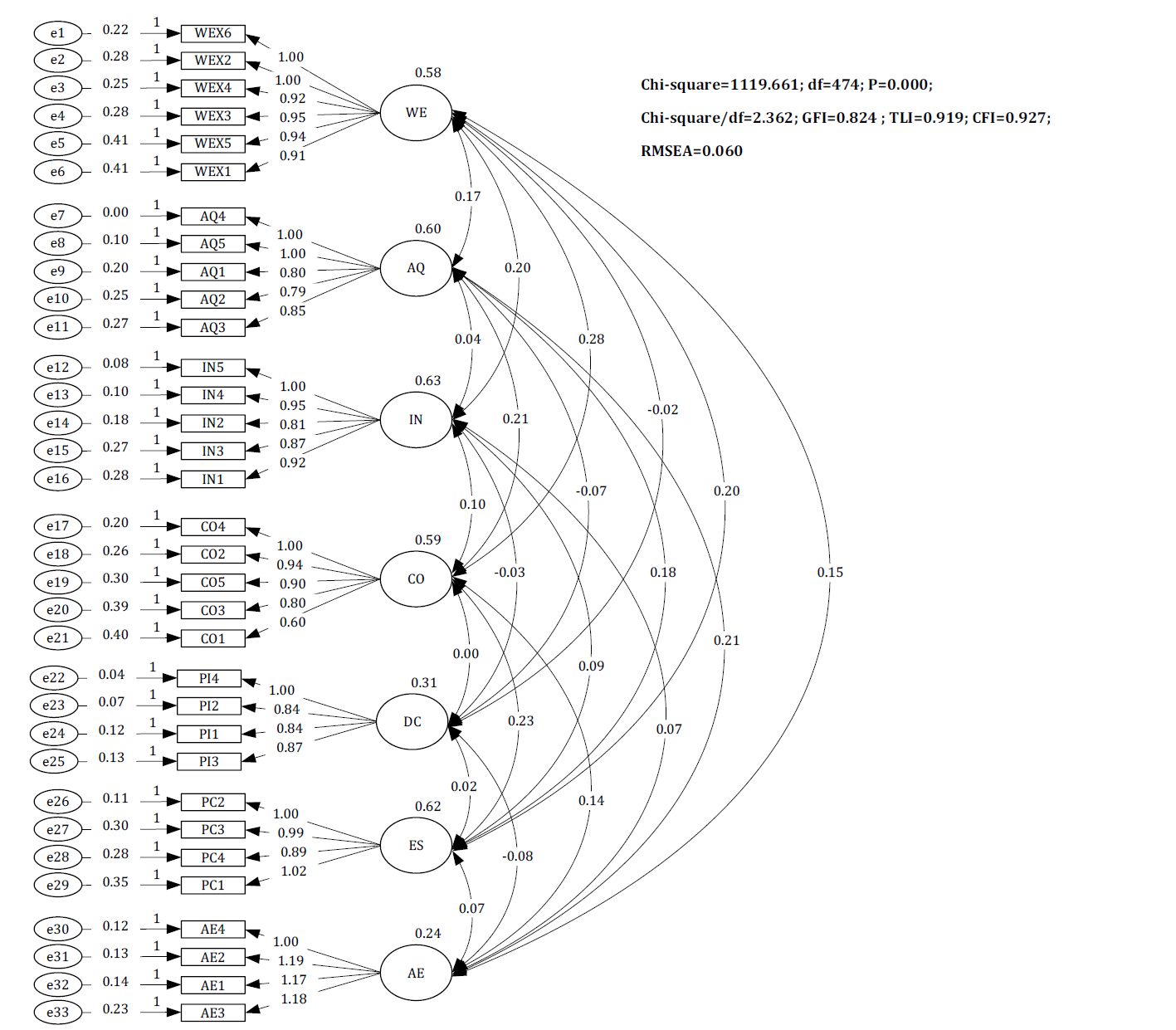

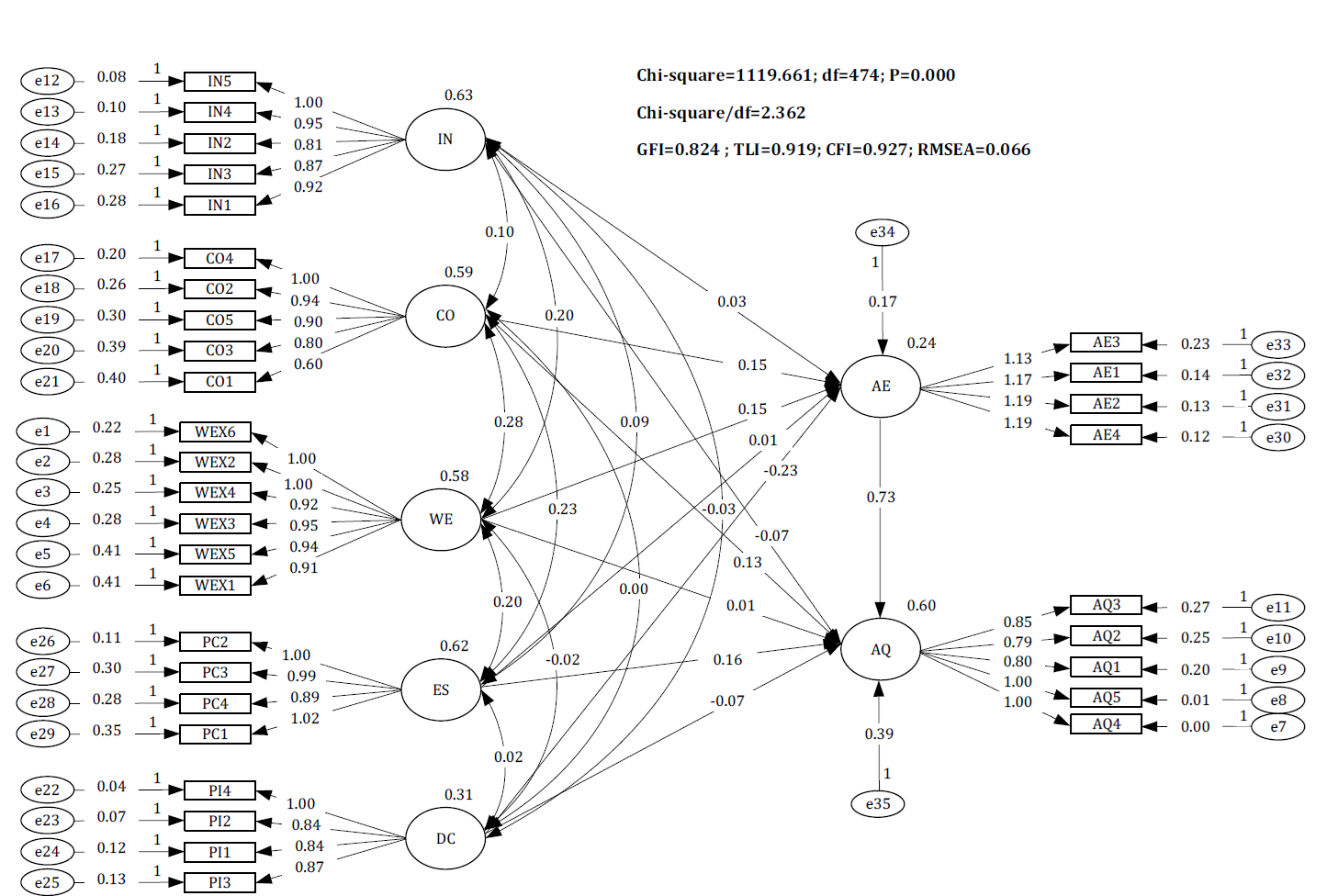

This paper aims to analyze the possible influence of auditor ethics (AE) factors on audit quality (AQ). Additionally, this study examines whether AE can mediate the relationship between various factors and AQ. These factors include independence, competence, work experience, ethical standards, and due care. Data were collected using structured questionnaires sent by post or email to auditors, audit team leaders, and deputy managers/heads of 314 independent audit firms in Vietnam. Using SPSS 26 and AMOS 24 for analysis, the results show positive relationships between competence, work experience, ethical standards, and AE, as well as between competence, due care, and AQ. Negative relationships were found between independence, due care, and AE and between independence, work experience, ethical standards, and AQ. These findings provide important recommendations for auditing companies to enhance ethics and AQ, helping them maintain loyal customers, attract potential clients, and further develop audit services in Vietnam.

© 2024 The Authors. Published by IASE.

This is an

Keywords

Auditor ethics, Audit quality, Independence, Competence, Ethical standards

Article history

Received 10 March 2024, Received in revised form 10 July 2024, Accepted 17 July 2024

Acknowledgment

The authors are thankful to Phenikaa University, the University of Transportation Technology, and Thuongmai University for funding this research. Especially thanks to the participants who took part in the study. I would like to thank the referees for their helpful comments and suggestions.

Compliance with ethical standards

Ethical considerations

All participants in this study provided informed consent, and their confidentiality was strictly maintained throughout the research process. The study followed ethical guidelines and received approval from the relevant institutional review boards.

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Nguyen TT, Nguyen HL, Le TN, and Tran NBH (2024). The influence of auditor ethics on audit quality: Analyzing key factors in Vietnamese audit firms. International Journal of Advanced and Applied Sciences, 11(7): 226-236

Figures

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (50)

- Abdelmoula L (2020). Impact of auditor’s competence, independence and reputation on the joint audit quality: The Tunisian context. Academy of Accounting and Financial Studies Journal, 24(3): 2-11. [Google Scholar]

- Alsughayer SA (2021). Impact of auditor competence, integrity, and ethics on audit quality in Saudi Arabia. Open Journal of Accounting, 10(4): 125-140. https://doi.org/10.4236/ojacct.2021.104011 [Google Scholar]

- Arens A, Elder R, Beasley M, and Hogan C (2017). Auditing and assurance services. Pearson Education, Harlow, UK. [Google Scholar]

- Beatty RP (1989). Auditor reputation and the pricing of initial public offerings. Accounting Review, 64(4): 693-709. [Google Scholar]

- Beckmerhagen IA, Berg HP, Karapetrovic SV, and Willborn WO (2004). On the effectiveness of quality management system audits. The TQM Magazine, 16(1): 14-25. https://doi.org/10.1108/09544780410511443 [Google Scholar]

- Boon K, McKinnon J, and Ross P (2008). Audit service quality in compulsory audit tendering: Preparer perceptions and satisfaction. Accounting Research Journal, 21(2): 93-122. https://doi.org/10.1108/10309610810905917 [Google Scholar]

- Cameran M, Campa D, and Francis JR (2022). The relative importance of auditor characteristics versus client factors in explaining audit quality. Journal of Accounting, Auditing and Finance, 37(4): 751-776. https://doi.org/10.1177/0148558X20953059 [Google Scholar]

- Conroy S, Emerson T, and Pons F (2010). Ethical attitudes of accounting practitioners: Are rank and ethical attitudes related? Journal of Business Ethics, 91 (2): 183-194. https://doi.org/10.1007/s10551-009-0076-2 [Google Scholar]

- Copley PA and Doucet MS (1993). Auditor tenure, fixed fee contracts, and the supply of substandard single audits. Public Budgeting and Finance, 13(3): 23-35. https://doi.org/10.1111/1540-5850.00980 [Google Scholar]

- Darmawan D, Sinambela EA, and Mauliyah NI (2017). The effect of competence, independence, and workload on audit quality. Journal of Academic Research and Sciences, 2(2): 47-57. https://doi.org/10.30957/jares.v2i2.404 [Google Scholar]

- Davidson RA and Neu D (1993). A note on association between audit firm size and audit quality. Contemporary Accounting Research, 9(2): 479-488. https://doi.org/10.1111/j.1911-3846.1993.tb00893.x [Google Scholar]

- DeAngelo LE (1981). Auditor size and audit quality. Journal of Accounting and Economics, 3(3): 183-199. https://doi.org/10.1016/0165-4101(81)90002-1 [Google Scholar]

- DeFond M and Zhang J (2014). A review of archival auditing research. Journal of Accounting and Economics, 58(2–3): 275–326. https://doi.org/10.1016/j.jacceco.2014.09.002 [Google Scholar]

- Douglas PC, Davidson RA, and Schwartz BN (2001). The effect of organizational culture and ethical orientation on accountants' ethical judgments. Journal of Business Ethics, 34: 101-121. https://doi.org/10.1023/A:1012261900281 [Google Scholar]

- Fatemi D, Hasseldine J, and Hite P (2018). The influence of ethical codes of conduct on professionalism in tax practice. Journal of Business Ethics, 164: 133-149. https://doi.org/10.1007/s10551-018-4081-1 [Google Scholar]

- Fornell C and Larcker DF (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1): 39-50. https://doi.org/10.1177/002224378101800104 [Google Scholar]

- Francis JR (2004). What do we know about audit quality? The British Accounting Review, 36(4): 345-368. https://doi.org/10.1016/j.bar.2004.09.003 [Google Scholar]

- Haenlein M and Kaplan AM (2004). A beginner's guide to partial least squares analysis. Understanding Statistics, 3(4): 283-297. https://doi.org/10.1207/s15328031us0304_4 [Google Scholar]

- Hair JF, Black WC, and Babin BJ (2010). Multivariate data analysis. Pearson Prentice Hall, Upper Saddle River, USA. [Google Scholar]

- Hajering MS (2019). Moderating ethics auditors influence of competence, accountability on audit quality. Jurnal Akuntansi, 23(3): 468-481. https://doi.org/10.24912/ja.v23i3.614 [Google Scholar]

- Hardiningsih P, Januarti I, Oktaviani RM, Srimindarti C, and Udin U (2019). Determinants of audit quality: An empirical insight from Indonesia. International Journal of Scientific and Technology Research, 8(7): 570-578. [Google Scholar]

- Harris J and Sutton C (1995). Unraveling the ethical decision-making process: Clues from an empirical study comparing Fortune 1000 executives and MBA students. Journal of Business Ethics, 14(10): 805-817. https://doi.org/10.1007/BF00872347 [Google Scholar]

- Helyer R (2015). Learning through reflection: The critical role of reflection in work-based learning (WBL). Journal of Work-Applied Management, 7(1): 15-27. https://doi.org/10.1108/JWAM-10-2015-003 [Google Scholar]

- Hope OK, Thomas WB, and Vyas D (2013). Financial reporting quality of US private and public firms. The Accounting Review, 88(5): 1715-1742. https://doi.org/10.2308/accr-50494 [Google Scholar]

- Kaiser HF (1974). An index of factorial simplicity. Psychometrika, 39(1): 31-36. https://doi.org/10.1007/BF02291575 [Google Scholar]

- Kertarajasa AY, Marwa T, and Wahyudi T (2019). The effect of competence, experience, independence, due professional care, and auditor integrity on audit quality with auditor ethics as moderating variable. Journal of Accounting, Finance and Auditing Studies, 5(1): 80-99. https://doi.org/10.32602/jafas.2019.4 [Google Scholar]

- Khan H, Rehmat M, Butt TH, Farooqi S, and Asim J (2020). Impact of transformational leadership on work performance, burnout and social loafing: A mediation model. Future Business Journal, 6: 40. https://doi.org/10.1186/s43093-020-00043-8 [Google Scholar]

- Knechel WR, Krishnan GV, Pevzner, M, Shefchik LB, and Velury UK (2013). Audit quality: Insights from the academic literature. Auditing: A Journal of Practice and Theory, 32(Supplement 1): 385-421. https://doi.org/10.2308/ajpt-50350 [Google Scholar]

- Krinsky I and Rotenberg W (1989). The valuation of initial public offerings. Contemporary Accounting Research, 5(2): 501-515. https://doi.org/10.1111/j.1911-3846.1989.tb00719.x [Google Scholar]

- Krishnan J and Schauer PC (2000). The differentiation of quality among auditors: evidence from the not-for-profit sector. Journal of Practice and Theory, 19(2): 9-25. https://doi.org/10.2308/aud.2000.19.2.9 [Google Scholar]

- Laitinen EK and Laitinen T (2015). A probability tree model of audit quality. European Journal of Operational Research, 243(2): 665-677. https://doi.org/10.1016/j.ejor.2014.12.021 [Google Scholar]

- Maree KW and Radloff S (2007). Factors affecting ethical judgement of South African chartered accountants. Meditari: Research Journal of the School of Accounting Sciences, 15(1): 1-18. https://doi.org/10.1108/10222529200700001 [Google Scholar]

- Meidawati N and Assidiqi A (2019). The influences of audit fees, competence, independence, auditor ethics, and time budget pressure on audit quality. Jurnal Akuntansi dan Auditing Indonesia, 23(2): 117-128. https://doi.org/10.20885/jaai.vol23.iss2.art6 [Google Scholar]

- Melinawati M and Prima AP (2020). Pengaruh kompetensi, independensi dan etika auditor terhadap kualitas audit di kantor akuntan publik kota batam. Jurnal Akrab Juara, 5(3): 60-70. https://doi.org/10.35906/ja001.v5i1.531 [Google Scholar]

- Mita DW (2016). Pengaruh kompetensi dan independensi terhaadap kualitas audit dengan etika auditor sebagai variabel intervening di kantor akuntan publik baihaqi and rekan. Jurnal Akuntansi Manajerial, 1(2): 20-30. https://doi.org/10.52447/jam.v1i2.745 [Google Scholar]

- Muslumov A and Aras G (2005). The analysis of factors affecting ethical judgements: The Turkish evidence. Representation of Social Responsibility: 161-172. Available online at: https://ssrn.com/abstract=890075

- Oktari KA, Widnyana IW, and Sapta IKS (2020). Effect of competence and independence on quality of audit result moderated by auditor ethics at the regional inspectorate of Klungkung. International Journal of Contemporary Research and Review, 11(9): 21846-21855. [Google Scholar]

- Partha M, Ajit D, Sudershan K, and Athira A (2021). Audit partner rotation, and its impact on audit quality: Evidence from India. Cogent Economics and Finance, 9(1): 1938379. https://doi.org/10.1080/23322039.2021.1938379 [Google Scholar]

- Patriandari and Heryanto P (2019). Pengaruh kompetensi, independensi dan due professional care terhadap kualitas internal audit pada PT. OTO multiartha Jakarta. Akrual: Jurnal Akuntansi dan Keuangan, 1(1): 49-64. https://doi.org/10.34005/akrual.v1i1.1014 [Google Scholar]

- Peštović K, Milicevic N, Djokic N, and Djokic I (2021). Audit service quality perceived by customers: Formative modelling measurement approach. Sustainability, 13(21): 11724. https://doi.org/10.3390/su132111724 [Google Scholar]

- Pflugrath G, Martinov‐Bennie N, and Chen L (2007). The impact of codes of ethics and experience on auditor judgments. Managerial Auditing Journal, 22(6): 566-589. https://doi.org/10.1108/02686900710759389 [Google Scholar]

- Pinatik S (2021). The effect of auditor's emotional intelligence, competence, and independence on audit quality. International Journal of Applied Business and International Management, 6(2): 55-67. https://doi.org/10.32535/ijabim.v6i2.1147 [Google Scholar]

- Pinto M, Rosidi R, and Baridwan Z (2020). Effect of competence, independence, time pressure and professionalism on audit quality (Inspeção Geral Do Estado in Timor Leste). International Journal of Multicultural and Multireligious Understanding, 7(8): 658-667. https://doi.org/10.18415/ijmmu.v7i8.2013 [Google Scholar]

- Puspitasari A, Baridwan Z, and Rahman AF (2019). The effect of audit competence, independence, and professional skepticism on audit quality with auditor’s ethics as moderation variables. International Journal of Business, Economics, and Law, 18(5): 135-144. [Google Scholar]

- Skinner DJ and Srinivasan S (2012). Audit quality and auditor reputation: Evidence from Japan. The Accounting Review, 87(5): 1737-1765. https://doi.org/10.2308/accr-50198 [Google Scholar]

- Soundarapandiyan K, Kumar TP, and Priyadarshini MK (2018). Effects of workplace fun on employee behaviors: An empirical study. International Journal of Mechanical and Production Engineering Research and Development, 8(3): 1040-1050. [Google Scholar]

- Tarigan MU and Susanti PB (2013). Pengaruh kompetensi, etika dan fee audit terhadap kualitas audit. Jurnal Akuntansi, 13(1): 803-832. [Google Scholar]

- Titman S and Trueman B (1986). Information quality and the valuation of new issues. Journal of Accounting and Economics, 8(2): 159-172. https://doi.org/10.1016/0165-4101(86)90016-9 [Google Scholar]

- Yuhan E (2022). Pengaruh due professional care, independensi, pengalaman auditor dan kompetensi auditor terhadap kualitas audit dengan locus of control internal sebagai variabel moderasi. PARSIMONIA: Jurnal Akuntansi, Manajemen dan Bisnis, 9(2): 58-76. https://doi.org/10.33479/parsimonia.v9i2.601 [Google Scholar]

- Zahmatkesh S and Rezazadeh J (2017). The effect of auditor features on audit quality. Tékhne, 15(2): 79-87. https://doi.org/10.1016/j.tekhne.2017.09.003 [Google Scholar]