International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 11, Issue 7 (July 2024), Pages: 199-207

----------------------------------------------

Original Research Paper

How internal auditing impacts governance mechanisms in small and medium-sized businesses

Author(s):

Affiliation(s):

Applied College, Imam Mohammad Ibn Saud Islamic University, Riyadh, Saudi Arabia

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0009-0007-2540-4983

Corresponding author's ORCID profile: https://orcid.org/0009-0007-2540-4983

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2024.07.022

Abstract

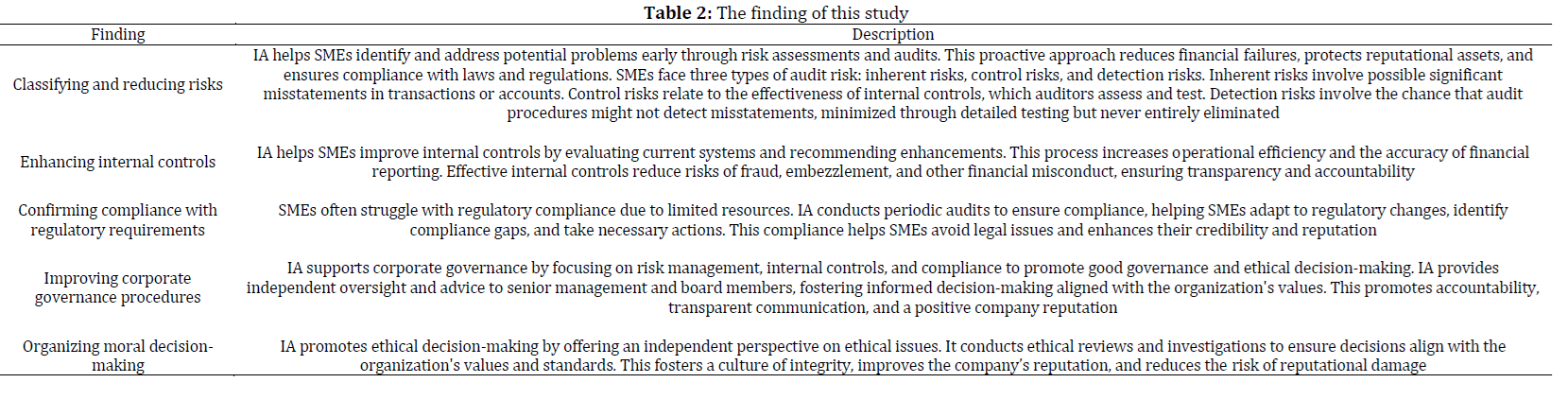

Small and medium-sized businesses (SMEs) use internal auditing (IA) as a key tool to start governance processes in their organizations. SMEs can gain several advantages from IA, such as identifying and managing risks, creating a strong control environment, ensuring compliance, improving operational efficiency, and aligning their strategies with their objectives. By using IA, SMEs can build a solid foundation for success and adapt to today's changing business environment. SMEs encounter specific challenges in initiating governance processes because they lack the resources and infrastructure that larger organizations have. Integrating IA into a company's management process can be difficult for smaller businesses, so they need to make full use of IA. Therefore, this study aims to examine how IA influences the activation of governance mechanisms in SMEs. The study uses the design science method (DSM). The results show that IA significantly affects the activation of governance mechanisms in SMEs. IA helps identify and manage risks, improve internal controls, ensure regulatory compliance, and address issues of concern. Effective IA functions can enhance corporate governance practices, promote ethical decision-making within the organization, and improve the overall effectiveness and success of the organization.

© 2024 The Authors. Published by IASE.

This is an

Keywords

Internal auditing, Small and medium-sized businesses, Governance processes, Risk management, Corporate governance

Article history

Received 17 March 2024, Received in revised form 12 July 2024, Accepted 14 July 2024

Acknowledgment

This work was supported and funded by the Deanship of Scientific Research at Imam Mohammad Ibn Saud Islamic University (IMSIU) (IMSIU, RG23O35).

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Alotaibi KO (2024). How internal auditing impacts governance mechanisms in small and medium-sized businesses. International Journal of Advanced and Applied Sciences, 11(7): 199-207

Figures

{kind=link}

Tables

{kind=link}

{kind=link}

----------------------------------------------

References (42)

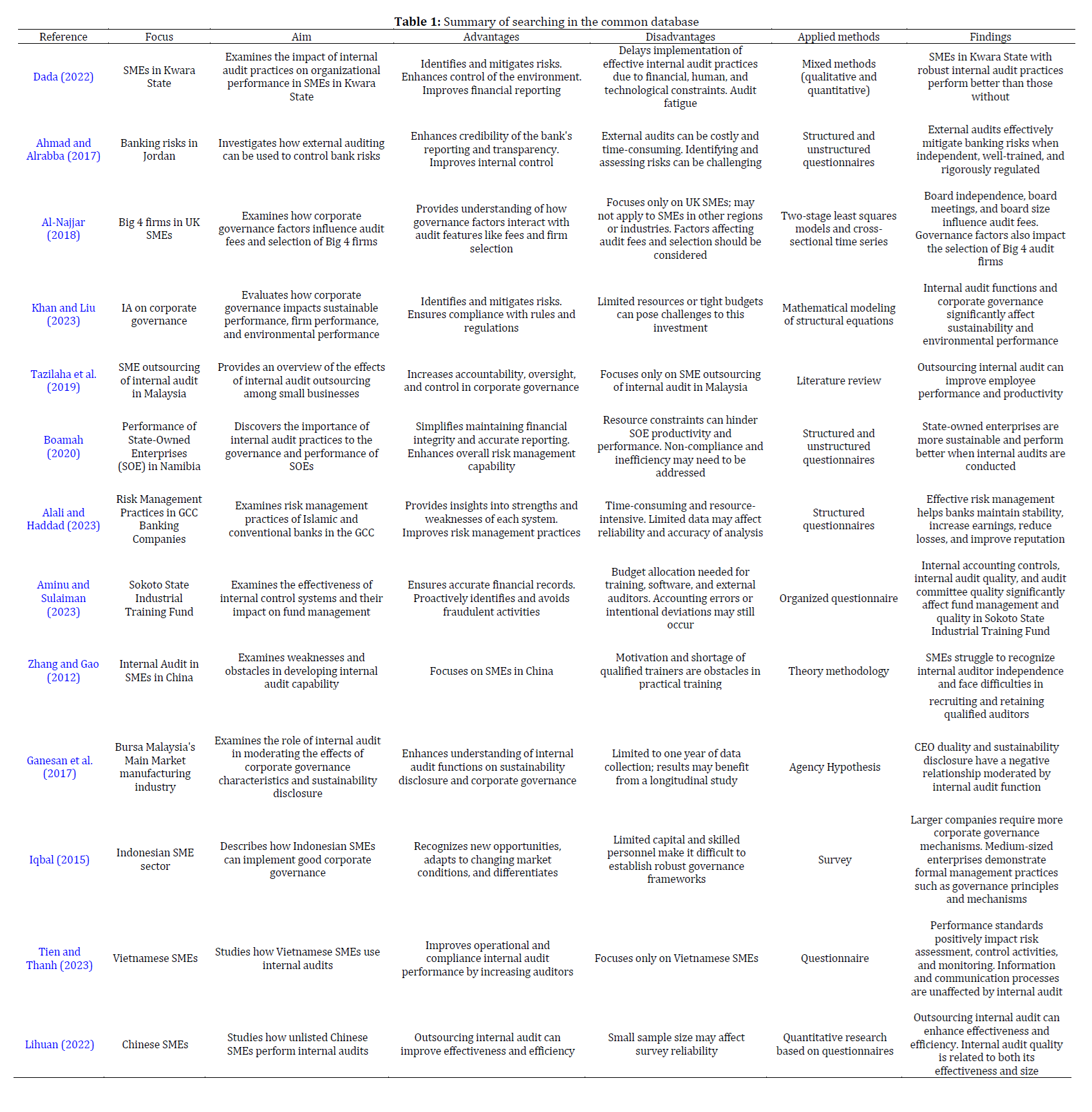

- Ahmad MA and Alrabba HM (2017). The role of external auditing in activating the governance for controlling banking risk. Corporate Ownership and Control, 14: 96-112. https://doi.org/10.22495/cocv14i3art10 [Google Scholar]

- Alali H and Haddad AE (2023). GCC banking companies risk management practices and its impact on their financial performance. Global Business Review. https://doi.org/10.1177/09721509231197718 [Google Scholar]

- Allegrini M, D’Onza G, Melville R, Paape L, and Sarens G (2008). CBOK Europe a state of the art of the internal audit profession in Europe. In the 1st Global Academic Conference on Internal Auditing and Corporate Governance, Emerald Publishing Limited, Kuala Lumpur, Malaysia: 20-22. [Google Scholar]

- Allegrini M, D'Onza G, Paape L, Melville R, and Sarens G (2006). The European literature review on internal auditing. Managerial Auditing Journal, 21(8): 845-853. https://doi.org/10.1108/02686900610703787 [Google Scholar]

- Almasria NA (2018). The relationship between internal corporate governance mechanisms and the quality of external audit process-empirical evidence from Jordan. Ph.D. Dissertation, University of Bedfordshire, London, UK. [Google Scholar]

- Al-Najjar B (2018). Corporate governance and audit features: SMEs evidence. Journal of Small Business and Enterprise Development, 25(1): 163-179. https://doi.org/10.1108/JSBED-08-2017-0243 [Google Scholar]

- Aminu HA and Sulaiman SM (2023). Effect of internal accounting control, internal audit quality and audit committees’ quality on fund management in Sokoto State industrial training fund. International Journal of Multidisciplinary Research and Growth Evaluation, 4(3): 315-321. [Google Scholar]

- Anderson JC, Rungtusanatham M, and Schroeder RG (1994). A theory of quality management underlying the Deming management method. Academy of Management Review, 19(3): 472-509. https://doi.org/10.5465/amr.1994.9412271808 [Google Scholar]

- Barac K and Motubatse KN (2009). Internal audit outsourcing practices in South Africa. African Journal of Business Management, 3(13): 969-979. [Google Scholar]

- Barac K, Plant K, Kunz R, and Kirstein M (2021). Audit practice: A straightforward trade or a complex system? International Journal of Auditing, 25(3): 797-812. https://doi.org/10.1111/ijau.12249 [Google Scholar]

- Beck U (2002). The terrorist threat: World risk society revisited. Theory, Culture and Society, 19(4): 39-55. https://doi.org/10.1177/0263276402019004003 [Google Scholar]

- Boamah K (2020). Impact of internal audit and corporate governance practices on the performance of state-owned enterprises in Namibia. Ph.D. Dissertation, Cape Peninsula University of Technology, Cape Town, South Africa. [Google Scholar]

- Dada AA (2022). Internal audit practices and organizational effectiveness among SMEs in Kwara State. Ph.D. Dissertation, Kwara State University, Kwara, Nigeria. [Google Scholar]

- De Zwaan L, Stewart J, and Subramaniam N (2011). Internal audit involvement in enterprise risk management. Managerial Auditing Journal, 26(7): 586-604. https://doi.org/10.1108/02686901111151323 [Google Scholar]

- DeLoach JW (2000). Enterprise-wide risk management: Strategies for linking risk and opportunity. Financial Times Prentice Hall, Harlow, UK. [Google Scholar]

- Dykstra J and Sherman AT (2013). Design and implementation of FROST: Digital forensic tools for the OpenStack cloud computing platform. Digital Investigation, 10: S87-S95. https://doi.org/10.1016/j.diin.2013.06.010 [Google Scholar]

- Formentini M and Taticchi P (2016). Corporate sustainability approaches and governance mechanisms in sustainable supply chain management. Journal of Cleaner Production, 112: 1920-1933. https://doi.org/10.1016/j.jclepro.2014.12.072 [Google Scholar]

- Ganesan Y, Hwa YW, Jaaffar AH and Hashim F (2017). Corporate governance and sustainability reporting practices: The moderating role of internal audit function. Global Business and Management Research, 9(4s): 159-179. [Google Scholar]

- Gofe TE (2020). A study on the role and effectiveness of internal audit in public enterprises: The case of Nekemte city administration. Public Policy and Administration Research, 10(10): 25-37. [Google Scholar]

- Hay D (2021). Perspectives on where international auditing research is going. International Journal of Auditing, 25(3): 619-620. https://doi.org/10.1111/ijau.12251 [Google Scholar]

- Holm C and Laursen PB (2007). Risk and control developments in corporate governance: Changing the role of the external auditor? Corporate Governance: An International Review, 15(2): 322-333. https://doi.org/10.1111/j.1467-8683.2007.00563.x [Google Scholar]

- Inua OI and Abianga EU (2015). The effect of the internal audit outsourcing on auditor independence: The Nigerian experience. Research Journal of Finance and Accounting, 6(10): 36-44. [Google Scholar]

- Iqbal M (2015). SME governance in Indonesia–A survey and insight from private companies. Procedia Economics and Finance, 31: 387-398. https://doi.org/10.1016/S2212-5671(15)01214-9 [Google Scholar]

- Kapoor G and Brozzetti M (2012). The transformation of internal auditing. The CPA Journal, 82(8): 32-35. [Google Scholar]

- Khan U and Liu W (2023). The role of internal auditing on corporate governance: Its effects of economic and environmental performance. Environmental Science and Pollution Research, 30(52): 112877-112891. https://doi.org/10.1007/s11356-023-30363-5 [Google Scholar] PMid:37840078

- Leung P, Cooper BJ, and Perera L (2011). Accountability structures and management relationships of internal audit: An Australian study. Managerial Auditing Journal, 26(9): 794-816. https://doi.org/10.1108/02686901111171457 [Google Scholar]

- Lihuan Z (2022). Factors affecting internal audit effectiveness: A research in China SMEs. Academic Journal of Business and Management, 4(15): 118-124. https://doi.org/10.25236/AJBM.2022.041519 [Google Scholar]

- Liu X, Li W, and Parsons K (2020). Exploring the antecedents of internal auditors' voice in environmental issues: Implications from China. International Journal of Auditing, 24(3): 396-411. https://doi.org/10.1111/ijau.12204 [Google Scholar]

- Mihret DG (2014). How can we explain internal auditing? The inadequacy of agency theory and a labor process alternative. Critical Perspectives on Accounting, 25(8): 771-782. https://doi.org/10.1016/j.cpa.2014.01.003 [Google Scholar]

- Mihret DG, James K, and Mula JM (2010). Antecedents and organisational performance implications of internal audit effectiveness: Some propositions and research agenda. Pacific Accounting Review, 22(3): 224-252. https://doi.org/10.1108/01140581011091684 [Google Scholar]

- Moll J and Yigitbasioglu O (2019). The role of internet-related technologies in shaping the work of accountants: New directions for accounting research. The British Accounting Review, 51(6): 100833. https://doi.org/10.1016/j.bar.2019.04.002 [Google Scholar]

- Nagy AL and Cenker WJ (2002). An assessment of the newly defined internal audit function. Managerial Auditing Journal, 17(3): 130-137. https://doi.org/10.1108/02686900210419912 [Google Scholar]

- Nickell EB and Roberts RW (2014). Organizational legitimacy, conflict, and hypocrisy: An alternative view of the role of internal auditing. Critical Perspectives on Accounting, 25(3): 217-221. https://doi.org/10.1016/j.cpa.2013.10.005 [Google Scholar]

- Peffers K, Tuunanen T, Rothenberger MA, and Chatterjee S (2007). A design science research methodology for information systems research. Journal of Management Information Systems, 24(3): 45-77. https://doi.org/10.2753/MIS0742-1222240302 [Google Scholar]

- Roussy M (2013). Internal auditors’ roles: From watchdogs to helpers and protectors of the top manager. Critical Perspectives on Accounting, 24(7-8): 550-571. https://doi.org/10.1016/j.cpa.2013.08.004 [Google Scholar]

- Soh DS and Martinov‐Bennie N (2011). The internal audit function: Perceptions of internal audit roles, effectiveness and evaluation. Managerial Auditing Journal, 26(7): 605-622. https://doi.org/10.1108/02686901111151332 [Google Scholar]

- Spira LF and Page M (2003). Risk management: The reinvention of internal control and the changing role of internal audit. Accounting, Auditing and Accountability Journal, 16(4): 640-661. https://doi.org/10.1108/09513570310492335 [Google Scholar]

- Tazilaha MDAK, Majid M, and Suffari NF (2019). Effects of outsourcing internal audit functions among small and medium enterprises (SMEs). International Journal of Business and Technology Management, 1(1): 17-22. [Google Scholar]

- Tien DN and Thanh HH (2023). The impacts of internal audit practices on the quality of internal control in Vietnamese SMEs. International Journal of Professional Business Review, 8(5): e01897. https://doi.org/10.26668/businessreview/2023.v8i5.2027 [Google Scholar]

- Walker PL, Shenkir WG, and Barton TL (2002). Enterprise risk management: Pulling it all together. Institute of Internal Auditors Research Foundation, Lake Mary, USA. [Google Scholar]

- Yasseen Y (2011). Outsourcing the internal audit function: A survey of the South African public and private sectors. Ph.D. Dissertation, University of the Witwatersrand, Johannesburg, South Africa. [Google Scholar]

- Zhang J and Gao S (2012). How do SMEs build internal audit capabilities? A grounded theory approach. World Review of Business Research, 2(1): 98-108. [Google Scholar]