International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 11, Issue 5 (May 2024), Pages: 121-128

----------------------------------------------

Original Research Paper

Analyzing microeconomic determinants of non-performing loans in Saudi Arabian banks: Implications for banking sector health and risk management

Author(s):

Affiliation(s):

Department of Finance and Insurance, College of Business Administration, Northern Border University, Arar, Saudi Arabia

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0009-0001-3914-3928

Corresponding author's ORCID profile: https://orcid.org/0009-0001-3914-3928

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2024.05.013

Abstract

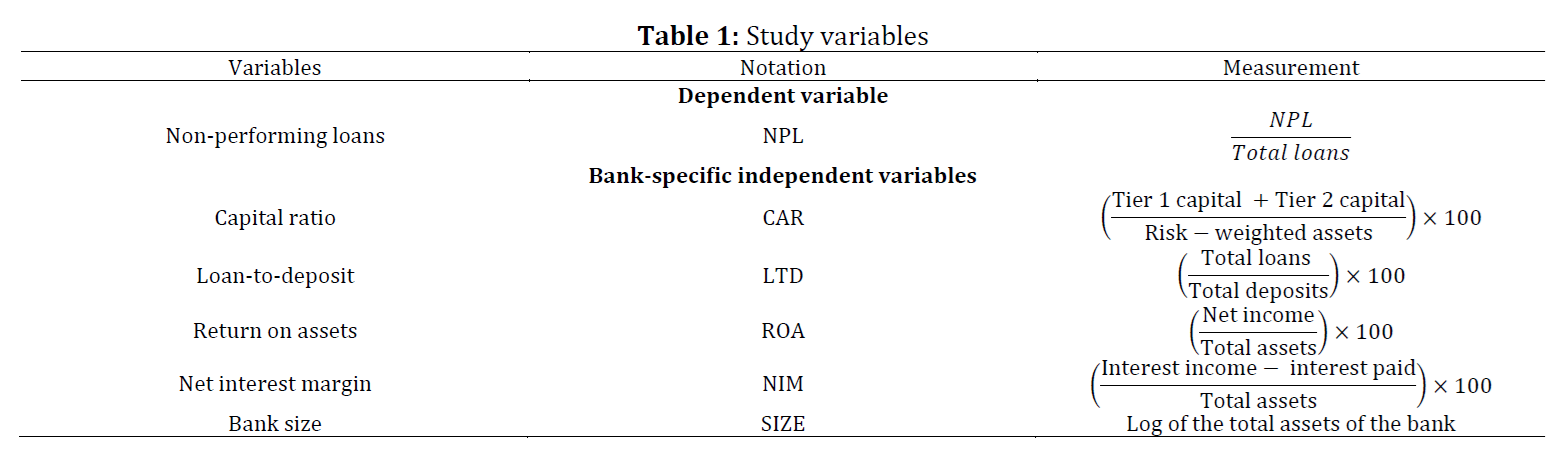

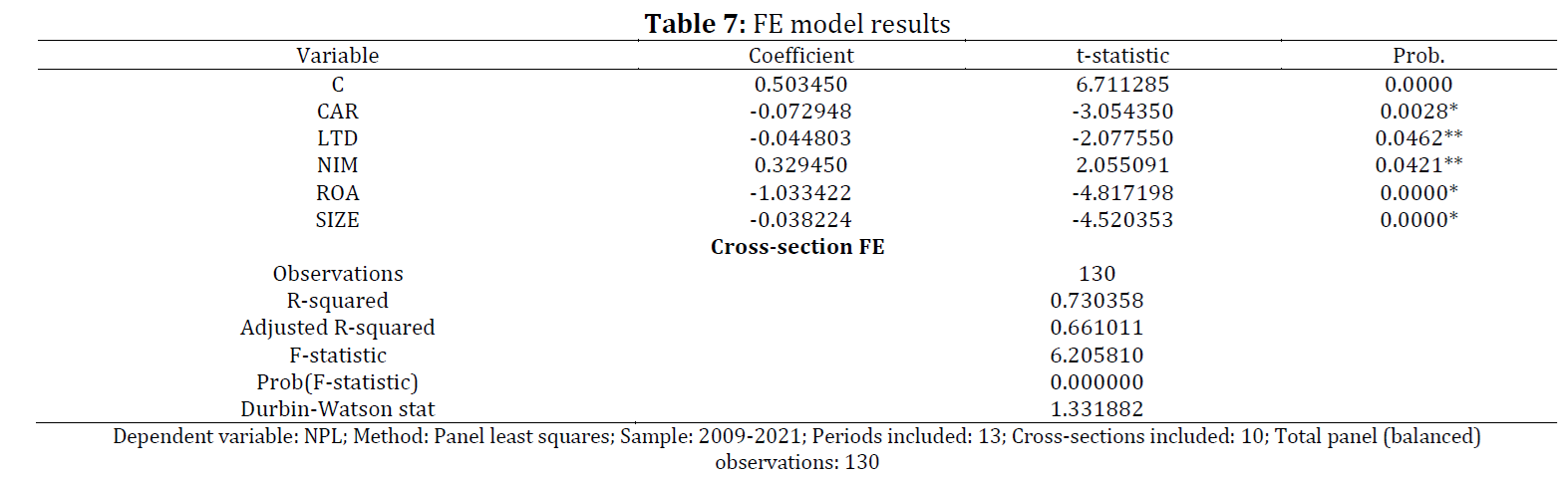

This research aims to study the smaller economic factors that influence the percentage of loans that banks in Saudi Arabia have given out but are not getting repaid. It uses data from 10 Saudi Arabian banks, covering 130 instances from the years 2009 to 2021, to figure out which economic factors at the bank level matter most. These factors are taken from the banks' yearly financial statements. The study looks at five specific factors suggested by earlier research, which are believed to impact the percentage of these non-repaying loans in the banking sector. These factors are the ratio of loans to deposits, the capital adequacy ratio (CAR), the return on assets (ROA), the net interest margin (NIM), and the size of the bank. The findings reveal that the size of the bank, its CAR, its ROA, its ratio of loans to deposits (which has a reverse effect), and its NIM (which has a direct effect) all play significant roles in determining the percentage of non-repaying loans in Saudi Arabian banks. Understanding these factors is crucial for getting insights into the health of the banking system. Monitoring and evaluating the ratio of non-repaying loans is important for keeping the financial system healthy and supporting steady economic growth. The study suggests that to manage the risks of loans not being repaid and to keep the banking system stable, effective policies and risk management practices are needed. It advises that banks improve their lending processes to manage non-repaying loans better and ensure profits for their shareholders.

© 2024 The Authors. Published by IASE.

This is an

Keywords

Non-performing loans, Microeconomic determinants, Banking sector health, Risk management

Article history

Received 17 December 2023, Received in revised form 17 April 2024, Accepted 1 May 2024

Acknowledgment

The author extends their appreciation to the Deanship of Scientific Research at Northern Border University, Arar, KSA, for funding this research work “through the Project number “NBU-FFR–2024–2453–01.”

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Twairesh AE (2024). Analyzing microeconomic determinants of non-performing loans in Saudi Arabian banks: Implications for banking sector health and risk management. International Journal of Advanced and Applied Sciences, 11(5): 121-128

Figures

No Figure

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (37)

- Abid L, Ouertani MN, and Zouari-Ghorbel S (2014). Macroeconomic and bank-specific determinants of household's non-performing loans in Tunisia: A dynamic panel data. Procedia Economics and Finance, 13: 58-68. https://doi.org/10.1016/S2212-5671(14)00430-4 [Google Scholar]

- Ahmad F (2013). Corruption and information sharing as determinants of non-performing loans. Business Systems Research: International Journal of the Society for Advancing Innovation and Research in Economy, 4(1): 87-98. https://doi.org/10.2478/bsrj-2013-0008 [Google Scholar]

- Akinlo O and Emmanuel M (2014). Determinants of non-performing loans in Nigeria. Accounting and Taxation, 6(2): 21-28. [Google Scholar]

- Anita SS, Tasnova N, and Nawar N (2022). Are non-performing loans sensitive to macroeconomic determinants? An empirical evidence from banking sector of SAARC countries. Future Business Journal, 8: 7. https://doi.org/10.1186/s43093-022-00117-9 [Google Scholar]

- Ari MA, Chen S, and Ratnovski ML (2019). The dynamics of non-performing loans during banking crises: a new database. ECB Working Paper Series, No 2395, International Monetary Fund, Washington, D.C., USA. https://doi.org/10.5089/9781513521152.001 [Google Scholar]

- Berger AN and DeYoung R (1997). Problem loans and cost efficiency in commercial banks. Journal of Banking and Finance, 21(6): 849-870. https://doi.org/10.1016/S0378-4266(97)00003-4 [Google Scholar]

- Boudriga A, Taktak NB, and Jellouli S (2010). Bank specific, business and institutional environment determinants of banks nonperforming loans: Evidence from Mena countries. In the Economic Research Forum, Working Paper, 547: 1-28. https://doi.org/10.1108/17576380911050043 [Google Scholar]

- Bruce C, Gearing ME, DeMatteis J, Levin K, Mulcahy T, Newsome J, and Wivagg J (2022). Financial vulnerability and the impact of COVID-19 on American households. PLOS ONE, 17(1): e0262301. https://doi.org/10.1371/journal.pone.0262301 [Google Scholar] PMid:35030175 PMCid:PMC8759691

- Curak M, Pepur S, and Poposki K (2013). Determinants of non-performing loans–evidence from Southeastern European banking systems. Banks and Bank Systems, 8(1): 45-53. [Google Scholar]

- Dao LKO, Nguyen TY, Hussain S, and Nguyen VC (2020). Factors affecting non-performing loans of commercial banks: The role of bank performance and credit growth. Banks and Bank Systems, 15(3): 44-54. https://doi.org/10.21511/bbs.15(3).2020.05 [Google Scholar]

- De Lis FS, Pagés JM, and Saurina J (2001). Credit growth, problem loans and credit risk provisioning in Spain. Bank for International Settlements, Marrying the Macro- and Micro-aspects of Financial Stability, BIS Papers No. 1: 331–353. [Google Scholar]

- Ekanayake EMNN and Azeez AA (2015). Determinants of non-performing loans in licensed commercial banks: Evidence from Sri Lanka. Asian Economic and Financial Review, 5(6): 868-882. https://doi.org/10.18488/journal.aefr/2015.5.6/102.6.868.882 [Google Scholar]

- Ferreira C (2022). Determinants of non-performing loans: A panel data approach. International Advances in Economic Research, 28(3): 133-153. https://doi.org/10.1007/s11294-022-09860-9 [Google Scholar]

- Godlewski CJ (2005). Bank capital and credit risk taking in emerging market economies. Journal of Banking Regulation, 6(2): 128-145. https://doi.org/10.1057/palgrave.jbr.2340187 [Google Scholar]

- Gujarati DN and Porter DC (2009). Basic econometrics. McGraw-Hill, Boston, USA. [Google Scholar]

- Hausman JA (1978). Specification tests in econometrics. Econometrica: Journal of the Econometric Society, 46(6): 1251-1271. https://doi.org/10.2307/1913827 [Google Scholar]

- Im KS, Pesaran MH and Shin Y (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics 115(1): 53-74. https://doi.org/10.1016/S0304-4076(03)00092-7 [Google Scholar]

- Jabbouri I and Naili M (2019). Determinants of nonperforming loans in emerging markets: Evidence from the Mena region. Review of Pacific Basin Financial Markets and Policies, 22(4): 1950026. https://doi.org/10.1142/S0219091519500267 [Google Scholar]

- Jameel K (2014). Crucial factors of nonperforming loans evidence from Pakistani banking sector. International Journal of Scientific and Engineering Research, 5(7): 704-710. [Google Scholar]

- Jolevski L (2017). Non-performing loans and profitability indicators: The case of the republic of Macednia. Journal оf Contemporary Economic аnd Business Issues, 4(2): 5-20. https://doi.org/10.7251/EMC1702184J [Google Scholar]

- Kartikasary M, Marsintauli F, Serlawati E, and Laurens S (2020). Factors affecting the non-performing loans in Indonesia. Accounting, 6(2): 97-106. https://doi.org/10.5267/j.ac.2019.12.003 [Google Scholar]

- Khafid M, Fachrurrozie, and Anisykurlillah I (2020). Investigating the determinants of non-performing loan: Loan monitoring as a moderating variable. KnE Social Sciences, 4(6): 126-136. https://doi.org/10.18502/kss.v4i6.6592 [Google Scholar]

- Klein N (2013). Non-performing loans in CESEE: Determinants and impact on macroeconomic performance. International Monetary Fund, Washington, USA. https://doi.org/10.5089/9781484318522.001 [Google Scholar]

- Le CDH and Le AH (2023). Macroeconomic determinants of non-performing loans: A quantile regression approach evidence from Vietnam's banking system. Journal of Eastern European and Central Asian Research, 10(5): 813-826. https://doi.org/10.15549/jeecar.v10i5.1255 [Google Scholar]

- Long VM, Yen NT, and Long PD (2020). Factors affecting non-performing loans (NPLs) of banks: The case of Vietnam. Ho Chi Minh City Open University Journal of Science-Economics and Business Administration, 10(2): 83-93. https://doi.org/10.46223/HCMCOUJS.econ.en.10.2.967.2020 [Google Scholar]

- Louzis DP, Vouldis AT, and Metaxas VL (2012). Macroeconomic and bank-specific determinants of non-performing loans in Greece: A comparative study of mortgage, business and consumer loan portfolios. Journal of Banking and Finance, 36(4): 1012-1027. https://doi.org/10.1016/j.jbankfin.2011.10.012 [Google Scholar]

- Makri V, Tsagkanos A, and Bellas A (2014). Determinants of non-performing loans: The case of Eurozone. Panoeconomicus, 61(2): 193-206. https://doi.org/10.2298/PAN1402193M [Google Scholar]

- Memdani L (2017). Macroeconomic and bank specific determinants of non-performing loans (NPLs) in the Indian banking sector. Studies in Business and Economics, 12(2): 125-135. https://doi.org/10.1515/sbe-2017-0026 [Google Scholar]

- Morakinyo AE and Sibanda M (2016). The determinants of non-performing loans in the MINT economies. Journal of Economics and Behavioral Studies, 8(5): 39-55. https://doi.org/10.22610/jebs.v8i5(J).1430 [Google Scholar]

- Rachman RA, Kadarusman YB, Anggriono K, and Setiadi R (2018). Bank-specific factors affecting non-performing loans in developing countries: Case study of Indonesia. The Journal of Asian Finance, Economics and Business, 5(2): 35-42. https://doi.org/10.13106/jafeb.2018.vol5.no2.35 [Google Scholar]

- Saba I, Kouser R, and Azeem M (2012). Determinants of non performing loans: Case of US banking sector. The Romanian Economic Journal, 44(6): 125-136. [Google Scholar]

- Salas V and Saurina J (2002). Credit risk in two institutional regimes: Spanish commercial and savings banks. Journal of Financial Services Research, 22(3): 203-224. https://doi.org/10.1023/A:1019781109676 [Google Scholar]

- Shingjergji A (2013). The impact of macroeconomic variables on the non performing loans in the Albanian banking system during 2005-2012. Academic Journal of Interdisciplinary Studies, 2(9): 335-339. https://doi.org/10.5901/ajis.2013.v2n9p335 [Google Scholar]

- Škarica B (2014). Determinants of non-performing loans in Central and Eastern European countries. Financial Theory and Practice, 38(1): 37-59. https://doi.org/10.3326/fintp.38.1.2 [Google Scholar]

- Swamy V (2012). Impact of macroeconomic and endogenous factors on non performing bank assets. The International Journal of Banking and Finance, 9 (1): 27-47. https://doi.org/10.32890/ijbf2012.9.1.8447 [Google Scholar]

- Thakor AV (2015). The financial crisis of 2007–2009: Why did it happen and what did we learn? The Review of Corporate Finance Studies, 4(2): 155-205. https://doi.org/10.1093/rcfs/cfv001 [Google Scholar]

- Touny MA and Shehab MA (2015). Macroeconomic determinants of non-performing loans: An empirical study of some Arab countries. American Journal of Economics and Business Administration, 7(1): 11-22. https://doi.org/10.3844/ajebasp.2015.11.22 [Google Scholar]