International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 11, Issue 4 (April 2024), Pages: 216-227

----------------------------------------------

Original Research Paper

Impact of Saudi corporate governance code and governance structures on industrial firms' performance in Saudi Arabia

Author(s):

Affiliation(s):

Department of Accounting, College of Business, Al Imam Mohammad Ibn Saud Islamic University, Riyadh, Saudi Arabia

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0009-0005-7651-9209

Corresponding author's ORCID profile: https://orcid.org/0009-0005-7651-9209

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2024.04.023

Abstract

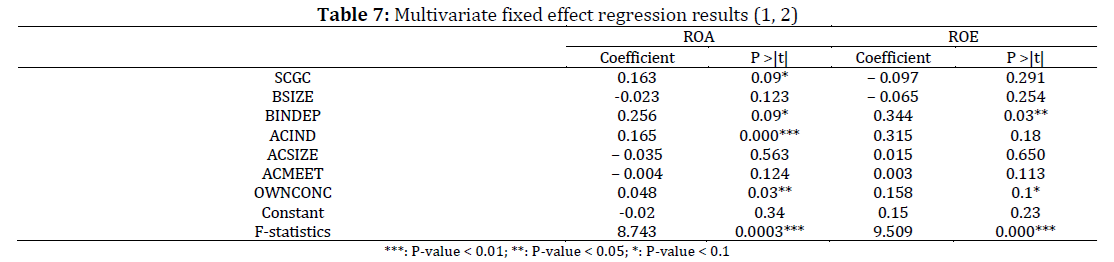

This research focuses on examining how the recent Saudi Corporate Governance Code (SCGC) and internal governance structures within companies affect the performance of industrial firms listed on the Saudi Stock Exchange. The authors studied 62 industrial firms from 2012 to 2020. They analyzed data using two models to test their hypotheses, looking at firm performance through two financial indicators: return on assets (ROA) for the first model and return on equity (ROE) for the second. Both models considered the same factors: SCGC, the size and independence of the board, the size and independence of the audit committee, how often the audit committee meets, and how concentrated the ownership is. The results indicated that applying the SCGC leads to better company performance based on ROA. However, there was no noticeable impact on performance from the board or audit committee size. Likewise, having more audit committee meetings did not improve performance. On the other hand, the independence of the board and audit committee, along with ownership concentration, did have a positive effect on performance. This study adds to the discussion on the economic impacts of the SCGC in the Saudi market, offering valuable insights for companies, investors, and policymakers like the Capital Market Authority (CMA) and the Saudi Organization for Chartered and Professional Accountants (SOCPA). These insights could guide adjustments to the SCGC that better suit the unique aspects of the Saudi market.

© 2024 The Authors. Published by IASE.

This is an

Keywords

Saudi corporate governance code, Firm performance, Industrial listed companies, Corporate governance structures, Saudi stock exchange

Article history

Received 2 December 2023, Received in revised form 11 April 2024, Accepted 18 April 2024

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Zehri F and Flah IB (2024). Impact of Saudi corporate governance code and governance structures on industrial firms' performance in Saudi Arabia. International Journal of Advanced and Applied Sciences, 11(4): 216-227

Figures

No Figure

Tables

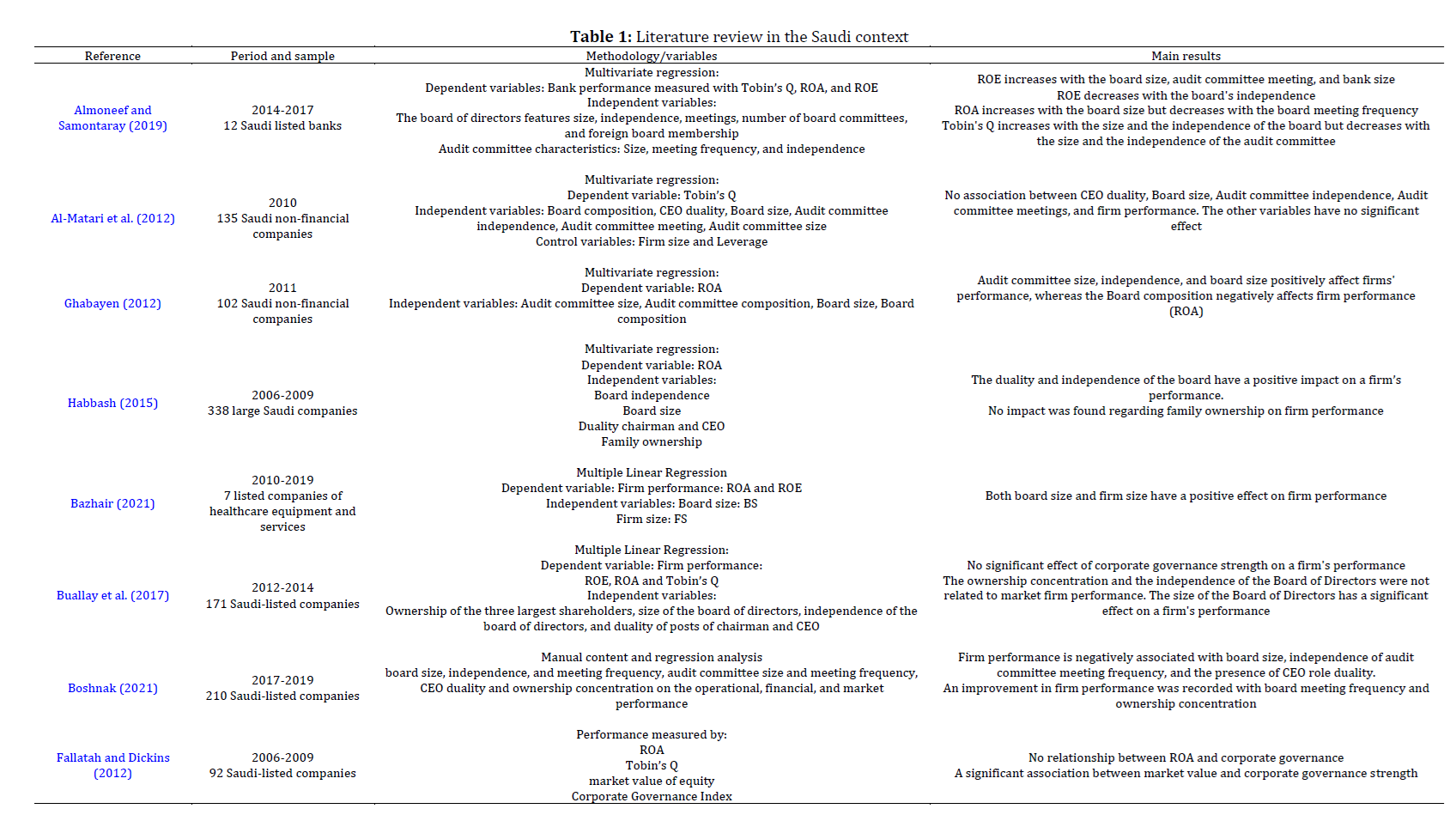

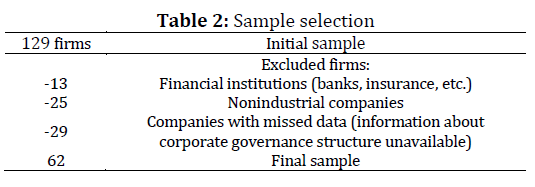

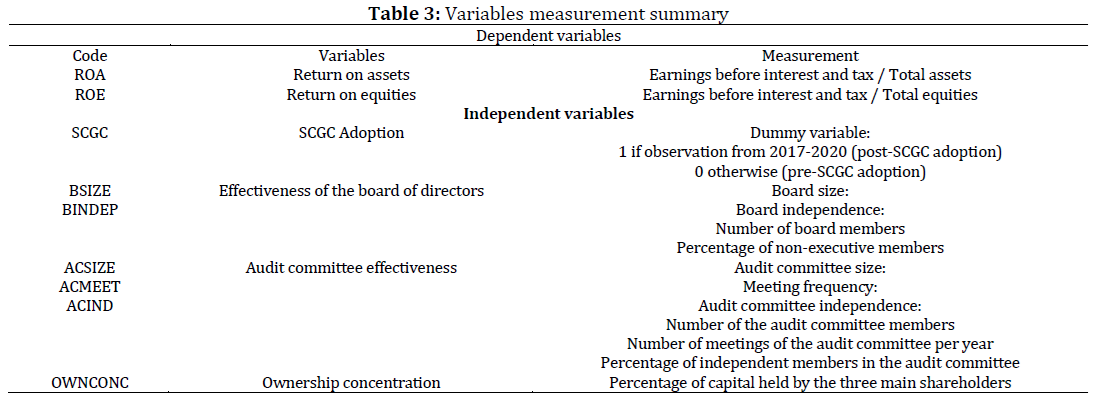

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (48)

- Abbott LJ, Parker S, and Peters GF (2004). Audit committee characteristics and restatements. Auditing: A Journal of Practice and Theory, 23(1): 69-87. https://doi.org/10.2308/aud.2004.23.1.69 [Google Scholar]

- Alajlan W (2004). Ownership patterns and the Saudi market. In: Hirschey M, John K, and Makhija AK (Eds.), Corporate governance: Advances in financial economics: 161-186. Volume 9, Emerald Group Publishing Limited, Leeds, UK. https://doi.org/10.1016/S1569-3732(04)09007-3 [Google Scholar]

- Al-Faryan MAS and Dockery E (2021). Testing for efficiency in the Saudi stock market: Does corporate governance change matter? Review of Quantitative Finance and Accounting, 57(1): 61-90. https://doi.org/10.1007/s11156-020-00939-0 [Google Scholar]

- Al-Gamrh B, Al-Dhamari R, Jalan A, and Jahanshahi AA (2020). The impact of board independence and foreign ownership on financial and social performance of firms: Evidence from the UAE. Journal of Applied Accounting Research, 21(2): 201-229. https://doi.org/10.1108/JAAR-09-2018-0147 [Google Scholar]

- Al-Malkawi HAN, Pillai R, and Bhatti MI (2014). Corporate governance practices in emerging markets: The case of GCC countries. Economic Modelling, 38: 133-141. https://doi.org/10.1016/j.econmod.2013.12.019 [Google Scholar]

- Al-Matari YA, Al-Swidi AK, FADZİL FH BH, and Al-Matari EM (2012). Board of directors, audit committee characteristics and the performance of Saudi Arabia listed companies. International Review of Management and Marketing, 2(4): 241-251. https://doi.org/10.5296/ijafr.v2i2.2384 [Google Scholar]

- Almoneef A and Samontaray DP (2019). Corporate governance and firm performance in the Saudi banking industry. Banks and Bank Systems, 14(1): 147-158. https://doi.org/10.21511/bbs.14(1).2019.13 [Google Scholar]

- Alshowish AM (2016). An evaluation of the current rules and regulatory framework of corporate governance in Saudi Arabia: A critical study in order to promote an attractive business environment. Ph.D. Dissertation, Lancaster University, Lancaster, UK. [Google Scholar]

- Asiri B and Alzeera H (2013). Is the Saudi stock market efficient? A case of weak-form efficiency. Research Journal of Finance and Accounting, 4(6): 35-48. [Google Scholar]

- Bajaher M, Habbash M, and Alborr A (2020). Board governance, ownership structure and foreign investment in the Saudi capital market. Review of Economics and Finance, 18: 117-125. https://doi.org/10.55365/1923.x2020.18.13 [Google Scholar]

- Bazhair AH (2021). Corporate governance mechanism and firm performance in Saudi Arabia. Studies of Applied Economics, 39: 4. https://doi.org/10.25115/eea.v39i4.4317 [Google Scholar]

- Bebchuk L, Cohen A, and Ferrell A (2009). What matters in corporate governance? The Review of Financial Studies, 22(2): 783-827. https://doi.org/10.1093/rfs/hhn099 [Google Scholar]

- Bhagat S and Bolton B (2008). Corporate governance and firm performance. Journal of Corporate Finance, 14(3): 257-273. https://doi.org/10.1016/j.jcorpfin.2008.03.006 [Google Scholar]

- Bhatt PR and Bhatt RR (2017). Corporate governance and firm performance in Malaysia. Corporate Governance: The International Journal of Business in Society, 17(5): 896-912. https://doi.org/10.1108/CG-03-2016-0054 [Google Scholar]

- Boshnak HA (2021). Corporate governance mechanisms and firm performance in Saudi Arabia. International Journal of Financial Research, 12(3): 446-465. https://doi.org/10.5430/ijfr.v12n3p446 [Google Scholar]

- Brown LD and Caylor ML (2004). Corporate governance and firm performance. https://doi.org/10.2139/ssrn.586423 [Google Scholar]

- Buallay A, Hamdan A, and Zureigat Q (2017). Corporate governance and firm performance: Evidence from Saudi Arabia. Australasian Accounting, Business and Finance Journal, 11(1): 78-98. https://doi.org/10.14453/aabfj.v11i1.6 [Google Scholar]

- Buchholz RA (1989). Business environment and public policy: Implications for management and strategy formulation. 3rd Edition, Prentice-Hall, Englewood Cliffs, USA. [Google Scholar]

- Chen JJ and Zhang H (2014). The impact of the corporate governance code on earnings management–Evidence from Chinese listed companies. European Financial Management, 20(3): 596-632. https://doi.org/10.1111/j.1468-036X.2012.00648.x [Google Scholar]

- Fallatah Y and Dickins D (2012). Corporate governance and firm performance and value in Saudi Arabia. African Journal of Business Management, 6(36): 10025-10034. https://doi.org/10.5897/AJBM12.008 [Google Scholar]

- Freeman RE (1984). Strategic management: A stakeholder approach. Pitman, Boston, USA. [Google Scholar]

- Fuzi SFS, Halim SAA, and Julizaerma MK (2016). Board independence and firm performance. Procedia Economics and Finance, 37: 460-465. https://doi.org/10.1016/S2212-5671(16)30152-6 [Google Scholar]

- Ghabayen M (2012). Board characteristics and firm performance: Case of Saudi Arabia. International Journal of Accounting and Financial Reporting, 2(2): 168-200. https://doi.org/10.5296/ijafr.v2i2.2145 [Google Scholar]

- Ghasemi MAA, Shakeri A, and Aghdam AN (2017). Introducing a model to measure the corporate governance index in usury-free banking. Journal of Money and Economy, 12(1): 55-71. [Google Scholar]

- Ghuslan MI, Jaffar R, Mohd Saleh N, and Yaacob MH (2021). Corporate governance and corporate reputation: The role of environmental and social reporting quality. Sustainability, 13(18): 10452. https://doi.org/10.3390/su131810452 [Google Scholar]

- Gompers P, Ishii J, and Metrick A (2003). Corporate governance and equity prices. The Quarterly Journal of Economics, 118(1): 107-156. https://doi.org/10.1162/00335530360535162 [Google Scholar]

- Gujarati D (2003). Basic econometrics. 4th Edition, McGraw Hill, New York, USA. [Google Scholar]

- Habbash M (2015). Corporate governance, ownership, company structure and environmental disclosure: Evidence from Saudi Arabia. Journal of Governance and Regulation, 4(4): 460-470. https://doi.org/10.22495/jgr_v4_i4_c4_p3 [Google Scholar]

- Haji AA and Mubaraq S (2015). The implications of the revised code of corporate governance on firm performance: A longitudinal examination of Malaysian listed companies. Journal of Accounting in Emerging Economies, 5(3): 350-380. https://doi.org/10.1108/JAEE-11-2012-0048 [Google Scholar]

- Hamdan AM and Al-Sartawi AM (2013). Corporate governance and institutional ownership: Evidence from Kuwait's financial sector. Jordan Journal of Business Administration, 9(1): 191-203. https://doi.org/10.12816/0002053 [Google Scholar]

- Hammad FB (2019). The Vision 2030: Corporate governance perspective in Saudi Arabia. Journal of System and Management Sciences, 9(1): 48-68. [Google Scholar]

- Kao MF, Hodgkinson L, and Jaafar A (2019). Ownership structure, board of directors and firm performance: Evidence from Taiwan. Corporate Governance: The International Journal of Business in Society, 19(1): 189-216. https://doi.org/10.1108/CG-04-2018-0144 [Google Scholar]

- Kijkasiwat P, Hussain A, and Mumtaz A (2022). Corporate governance, firm performance and financial leverage across developed and emerging economies. Risks, 10: 185. https://doi.org/10.3390/risks10100185 [Google Scholar]

- Koldertsova A (2011). The second corporate governance wave in the Middle East and North Africa. OECD Journal: Financial Market Trends, 2010(2): 219-226. https://doi.org/10.1787/fmt-2010-5kggc0z1jw7k [Google Scholar]

- Lee SY and Ko EJ (2022). Effects of founder CEO duality and board size on foreign IPOs’ survival in US markets. Corporate Governance: The International Journal of Business in Society, 22(5): 1054-1077. https://doi.org/10.1108/CG-04-2021-0151 [Google Scholar]

- Mallin CA (2004). Corporate governance. Oxford University Press, Oxford, UK. [Google Scholar]

- Mansour M, Hashim HA, Salleh Z, Al-ahdal WM, Almaqtari FA, and Qamhan MA (2022). Governance practices and corporate performance: Assessing the competence of principal-based guidelines. Cogent Business and Management, 9(1): 2105570. https://doi.org/10.1080/23311975.2022.2105570 [Google Scholar]

- Nguyen NPA and Dao TTB (2022). Liquidity, corporate governance and firm performance: A meta-analysis. Cogent Business and Management, 9(1): 2137960. https://doi.org/10.1080/23311975.2022.2137960 [Google Scholar]

- Nurunnabi M (2017). Transformation from an oil-based economy to a knowledge-based economy in Saudi Arabia: The direction of Saudi Vision 2030. Journal of the Knowledge Economy, 8: 536-564. https://doi.org/10.1007/s13132-017-0479-8 [Google Scholar]

- Oudat MS, ALI BJ, and Qeshta MH (2021). Financial performance and audit committee characteristics: An empirical study on Bahrain services sector. The Journal of Contemporary Issues in Business and Government, 27(2): 4278-4288. https://doi.org/10.47750/cibg.2021.27.02.453 [Google Scholar]

- Pham HN and Islam SM (2022). Corporate governance, ownership structure and firm performance: Mediation models and dynamic approaches. Routledge, New York, USA. https://doi.org/10.4324/9781003255741 [Google Scholar]

- Pillai RR and Al-Malkawi HAN (2016). Corporate governance in the GCC countries: Empirical assessment using conventional and non–conventional indices. The Journal of Developing Areas, 50(6): 69-88. https://doi.org/10.1353/jda.2016.0136 [Google Scholar]

- Puni A and Anlesinya A (2020). Corporate governance mechanisms and firm performance in a developing country. International Journal of Law and Management, 62(2): 147-169. https://doi.org/10.1108/IJLMA-03-2019-0076 [Google Scholar]

- Shleifer A and Vishny RW (1997). A survey of corporate governance. The Journal of Finance, 52(2): 737-783. https://doi.org/10.1111/j.1540-6261.1997.tb04820.x [Google Scholar]

- Solomon MR (2004). Consumer behaviour, buying, having and being. 6th Edition, Pearson Prentice Hall, Hoboken, USA. [Google Scholar]

- Tawfik OI, Alsmady AA, Rahman RA, and Alsayegh MF (2022). Corporate governance mechanisms, royal family ownership and corporate performance: Evidence in Gulf Cooperation Council (GCC) market. Heliyon, 8: e12389. https://doi.org/10.1016/j.heliyon.2022.e12389 [Google Scholar] PMid:36636223 PMCid:PMC9830172

- Yasser QR and Mamun AA (2017). The impact of ownership concentration on firm performance: Evidence from an emerging market. Emerging Economy Studies, 3(1): 34-53. https://doi.org/10.1177/2394901517696647 [Google Scholar]

- Zgarni I, Hlioui K, and Zehri F (2016). Effective audit committee, audit quality and earnings management: Evidence from Tunisia. Journal of Accounting in Emerging Economies, 6(2): 138-155. https://doi.org/10.1108/JAEE-09-2013-0048 [Google Scholar]