International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 2 (February 2025), Pages: 13-22

----------------------------------------------

Original Research Paper

Improving corporate governance to enhance earnings quality: Empirical evidence from the emerging market of Vietnam

Author(s):

Affiliation(s):

School of Economics, Can Tho University, Can Tho City, Vietnam

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-1513-3362

Corresponding author's ORCID profile: https://orcid.org/0000-0002-1513-3362

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.02.002

Abstract

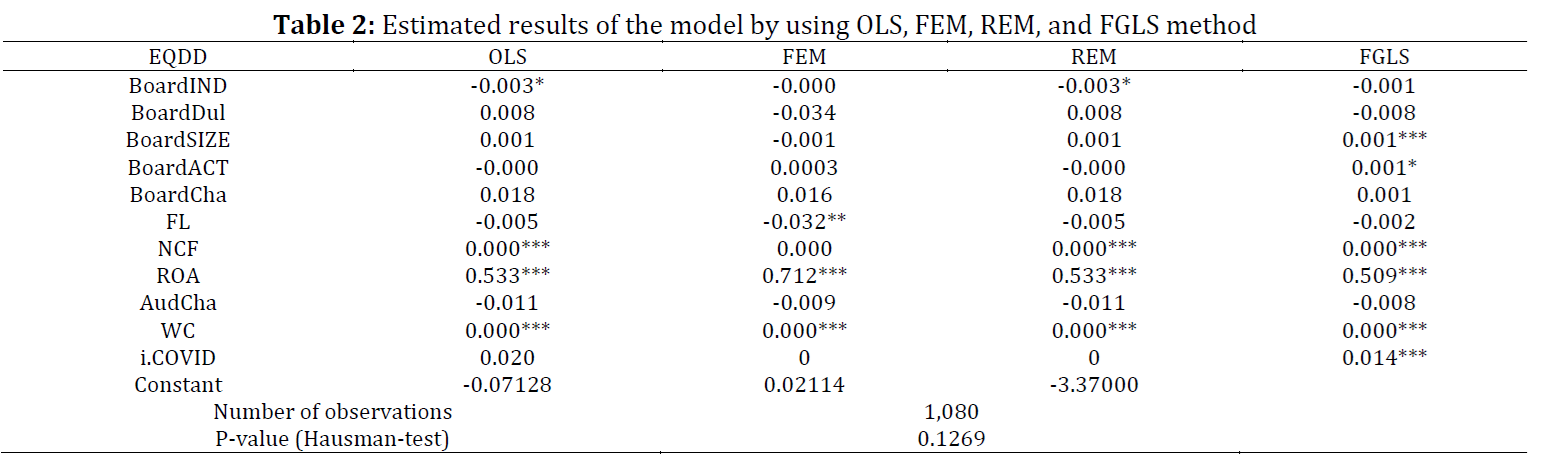

This study aims to provide more evidence on the earnings quality of companies listed in emerging markets by examining how corporate governance factors affect earnings quality in Vietnam. Using panel data analysis, the research analyzed data from 216 firms listed on Vietnam’s two main stock exchanges, the Ho Chi Minh Stock Exchange (HOSE) and the Hanoi Stock Exchange (HNX), between 2017 and 2021. The findings identified six key variables with a significant impact on earnings quality: board size, board activity, net cash flow from operations, return on assets, working capital, and the COVID-19 pandemic. These results highlight the critical role of corporate governance in improving the earnings quality of listed firms. Therefore, this study offers valuable insights for securities analysts, regulatory bodies, and users of accounting information to better understand the relationship between corporate governance and earnings quality in the Vietnamese market.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Corporate governance, Earnings quality, Emerging markets, Panel data analysis, Stock exchanges

Article history

Received 26 August 2024, Received in revised form 5 January 2025, Accepted 16 January 2025

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Thuan LT, Diep NTN, Truc TVT, Trang NTN, Dung NTP, and Trang LTT (2025). Improving corporate governance to enhance earnings quality: Empirical evidence from the emerging market of Vietnam. International Journal of Advanced and Applied Sciences, 12(2): 13-22

Figures

{kind=link}

{kind=link}

Tables

{kind=link}

{kind=link}

----------------------------------------------

References (51)

- Abdul Rahman R and Haneem Mohamed Ali F (2006). Board, audit committee, culture and earnings management: Malaysian evidence. Managerial Auditing Journal, 21(7): 783-804. https://doi.org/10.1108/02686900610680549 [Google Scholar]

- Abdullah S (2006). Directors' remuneration, firm's performance and corporate governance in Malaysia among distressed companies. Corporate Governance: The International Journal of Business in Society, 6(2): 162-174. https://doi.org/10.1108/14720700610655169 [Google Scholar]

- ACFE (2008). Report to the nation on occupational fraud and abuse. Association of Certified Fraud Examiners Austin, Austin, USA. [Google Scholar]

- Aljawaheri BAW, Ojah HK, Machi AH, and ALmagtome AH (2021). COVID-19 lockdown, earnings manipulation and stock market sensitivity: An empirical study in Iraq. The Journal of Asian Finance, Economics and Business, 8(5): 707-715. [Google Scholar]

- Aljifri K and Elrazaz T (2024). Effect of earnings management on earnings quality and sustainability: Evidence from Gulf Cooperation Council distressed and non-distressed companies. Journal of Risk and Financial Management, 17(8): 348. https://doi.org/10.3390/jrfm17080348 [Google Scholar]

- Al‐Najjar B (2015). The effect of governance mechanisms on small and medium‐sized enterprise cash holdings: Evidence from the United Kingdom. Journal of Small Business Management, 53: 303-320. https://doi.org/10.1111/jsbm.12062 [Google Scholar]

- Alzoubi ESS and Selamat MH (2012). The effectiveness of corporate governance mechanisms on constraining earning management: Literature review and proposed framework. International Journal of Global Business, 5(1): 17-35. https://doi.org/10.5296/ijafr.v2i1.1561 [Google Scholar]

- Bahmani D (2014). The relation between disclosure quality and information asymmetry: Empirical evidence from Iran. International Journal of Financial Research, 5(2): 110–114. https://doi.org/10.5430/ijfr.v5n2p110 [Google Scholar]

- Becker CL, DeFond ML, Jiambalvo J, and Subramanyam KR (1998). The effect of audit quality on earnings management. Contemporary Accounting Research, 15(1): 1-24. https://doi.org/10.1111/j.1911-3846.1998.tb00547.x [Google Scholar]

- Bellovary JL, Giacomino DE, and Akers MD (2005). Earnings quality: It's time to measure and report. The CPA Journal, 75(11): 32-37. [Google Scholar]

- Beneish MD (1999). The detection of earnings manipulation. Financial Analysts Journal, 55(5): 24-36. https://doi.org/10.2469/faj.v55.n5.2296 [Google Scholar]

- Berle A and Means G (1932). The modern corporation and private property. Commerce Clearing House, New York, USA. [Google Scholar]

- Boshnak HA (2021). Corporate governance mechanisms and firm performance in Saudi Arabia. International Journal of Financial Research, 12(3): 446-465. https://doi.org/10.5430/ijfr.v12n3p446 [Google Scholar]

- Carcello JV, Hermanson DR, and Ye Z (2011). Corporate governance research in accounting and auditing: Insights, practice implications, and future research directions. Auditing: A Journal of Practice and Theory, 30(3): 1-31. https://doi.org/10.2308/ajpt-10112 [Google Scholar]

- Cascino S, Pugliese A, Mussolino D, and Sansone C (2010). The influence of family ownership on the quality of accounting information. Family Business Review, 23(3): 246-265. https://doi.org/10.1177/0894486510374302 [Google Scholar]

- Claessens S and Fan JPH (2002). Corporate governance in Asia: A survey. International Review of Finance, 3(2): 71-103. https://doi.org/10.1111/1468-2443.00034 [Google Scholar]

- Cornett MM, McNutt JJ, and Tehranian H (2009). Corporate governance and earnings management at large US bank holding companies. Journal of Corporate Finance, 15(4): 412-430. https://doi.org/10.1016/j.jcorpfin.2009.04.003 [Google Scholar]

- DeAngelo H, DeAngelo L, and Skinner DJ (1994). Accounting choice in troubled companies. Journal of Accounting and Economics, 17(1-2): 113-143. https://doi.org/10.1016/0165-4101(94)90007-8 [Google Scholar]

- Dechow PM and Dichev ID (2002). The quality of accruals and earnings: The role of accrual estimation errors. The Accounting Review, 77(s-1): 35-59. https://doi.org/10.2308/accr.2002.77.s-1.35 [Google Scholar]

- Doyle JT, Ge W, and McVay S (2007). Accruals quality and internal control over financial reporting. The Accounting Review, 82(5): 1141–1170. https://doi.org/10.2308/accr.2007.82.5.1141 [Google Scholar]

- Efendi J, Srivastava A, and Swanson EP (2007). Why do corporate managers misstate financial statements? The role of option compensation and other factors. Journal of Financial Economics, 85(3): 667-708. https://doi.org/10.1016/j.jfineco.2006.05.009 [Google Scholar]

- Erickson M, Hanlon M, and Maydew E (2004). How much will firms pay for earnings that do not exist? Evidence of taxes paid on allegedly fraudulent earnings. The Accounting Review, 79(2): 387-40. https://doi.org/10.2308/accr.2004.79.2.387 [Google Scholar]

- Ewert R and Wagenhofer A (2012). Earnings management, conservatism, and earnings quality. Foundations and Trends® in Accounting, 6(2): 65-186. https://doi.org/10.1561/1400000025 [Google Scholar]

- Francis J, Hanna JD, and Vincent L (1996). Causes and effects of discretionary asset write-offs. Journal of Accounting Research, 34: 117-134. https://doi.org/10.2307/2491429 [Google Scholar]

- Francis J, LaFond R, Olsson P, and Schipper K (2005). The market pricing of accruals quality. Journal of Accounting and Economics, 39(2): 295-327. https://doi.org/10.1016/j.jacceco.2004.06.003 [Google Scholar]

- Freeman R (1984). Strategic management: A stakeholder approach. Pitman, Boston, USA. [Google Scholar]

- Friedlan JM (1994). Accounting choices of issuers of initial public offerings. Contemporary Accounting Research, 11(1): 1-31. https://doi.org/10.1111/j.1911-3846.1994.tb00434.x [Google Scholar]

- Gulzar MA (2011). Corporate governance characteristics and earnings management: Empirical evidence from Chinese listed firms. International Journal of Accounting and Financial Reporting, 1(1): 133-151. https://doi.org/10.5296/ijafr.v1i1.854 [Google Scholar]

- Hamidzadeh S and Zeinali M (2015). The asset structure and liquidity effect on financial reporting quality at listed companies in Tehran Stock Exchange. Arabian Journal of Business Management and Review, 4(7): 121-127. https://doi.org/10.12816/0019078 [Google Scholar]

- Humeedat M (2018). Earnings management to avoid financial distress and improve profitability: Evidence from Jordan. International Business Research, 11(2): 222-230. https://doi.org/10.5539/ibr.v11n2p222 [Google Scholar]

- Jensen MC and Meckling WH (1978). Can the corporation survive? Financial Analysts Journal, 34(1): 31-37. https://doi.org/10.2469/faj.v34.n1.31 [Google Scholar]

- Jiang W, Lee P, and Anandarajan A (2008). The association between corporate governance and earnings quality: Further evidence using the GOV-Score. Advances in Accounting, 24(2): 191-201. https://doi.org/10.1016/j.adiac.2008.08.011 [Google Scholar]

- John K and Senbet LW (1998). Corporate governance and board effectiveness. Journal of Banking and Finance, 22(4): 371-403. https://doi.org/10.1016/S0378-4266(98)00005-3 [Google Scholar]

- Jones JJ (1991). Earnings management during import relief investigations. Journal of Accounting Research, 29(2): 193-228. https://doi.org/10.2307/2491047 [Google Scholar]

- Kankanamage CA (2015). The relationship between board characteristics and earnings management: Evidence from Sri Lankan listed companies. Kelaniya Journal of Management, 4(2): 36-43. https://doi.org/10.4038/kjm.v4i2.7499 [Google Scholar]

- Krishnan GV and Visvanathan G (2008). Does the SOX definition of an accounting expert matter? The association between audit committee directors' accounting expertise and accounting conservatism. Contemporary Accounting Research, 25(3): 827-858. https://doi.org/10.1506/car.25.3.7 [Google Scholar]

- Lin JW, Li JF, and Yang JS (2006). The effect of audit committee performance on earnings quality. Managerial Auditing Journal, 21(9): 921-933. https://doi.org/10.1108/02686900610705019 [Google Scholar]

- Liu M, Shi Y, Wilson C, and Wu Z (2017). Does family involvement explain why corporate social responsibility affects earnings management? Journal of Business Research, 75: 8-16. https://doi.org/10.1016/j.jbusres.2017.02.001 [Google Scholar]

- Lobo GJ and Zhou J (2006). Did conservatism in financial reporting increase after the Sarbanes Oxley Act? Initial evidence. Accounting Horizons, 20(1): 57-73. https://doi.org/10.2308/acch.2006.20.1.57 [Google Scholar]

- Mashayekhi B and Bazaz MS (2008). Corporate governance and firm performance in Iran. Journal of Contemporary Accounting and Economics, 4(2): 156-172. https://doi.org/10.1016/S1815-5669(10)70033-3 [Google Scholar]

- Nugroho BY and Eko U (2011). Board characteristics and earning management. Journal of Administrative Science and Organization, 18(1): 1-10. [Google Scholar]

- Parte-Esteban L and García CF (2014). The influence of firm characteristics on earnings quality. International Journal of Hospitality Management, 42: 50-60. https://doi.org/10.1016/j.ijhm.2014.06.008 [Google Scholar]

- Radzi SN, Islam MA, and Ibrahim S (2011). Earning quality in public listed companies: A study on Malaysia exchange for securities dealing and automated quotation. International Journal of Economics and Finance, 3(2): 233-244. https://doi.org/10.5539/ijef.v3n2p233 [Google Scholar]

- Richardson Scott A and Sloan RG (2003). External financing and future stock returns. Working Paper, University of Pennsylvania, Pennsylvania, USA. https://doi.org/10.2139/ssrn.383240 [Google Scholar]

- Ross SA (1973). The economic theory of agency: The principal's problem. The American Economic Review, 63(2): 134-139. [Google Scholar]

- Teets WR (2002). Quality of earnings: An introduction to the Issues in Accounting Education special issue. Issues in Accounting Education, 17(4): 355-361. https://doi.org/10.2308/iace.2002.17.4.335 [Google Scholar]

- Tendeloo BV and Vanstraelen A (2008). Earnings management and audit quality in Europe: Evidence from the private client segment market. European Accounting Review, 17(3): 447-469. https://doi.org/10.1080/09638180802016684 [Google Scholar]

- Waweru NM and Riro GK (2013). Corporate governance, firm characteristics and earnings management in an emerging economy. Journal of Applied Management Accounting Research, 11(1): 43-64. [Google Scholar]

- Xiao H and Xi J (2021). The COVID-19 and earnings management: China's evidence. Journal of Accounting and Taxation, 13(2): 59-77. [Google Scholar]

- Xie B, Davidson W, and DaDalt P (2003). Earnings management and corporate governance: The roles of the board and the audit committee. Journal of Corporate Finance, 9(3): 295-317. https://doi.org/10.1016/S0929-1199(02)00006-8 [Google Scholar]

- Yermack D (1996). Higher market valuation of companies with a small board of directors. Journal of Financial Economics, 40(2): 185-211. https://doi.org/10.1016/0304-405X(95)00844-5 [Google Scholar]