International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 1 (January 2025), Pages: 7-18

----------------------------------------------

Original Research Paper

Explaining REIT returns in emerging economies: A Fama-French approach with foreign investment and political stability

Author(s):

Affiliation(s):

College of Business, Effat University, Jeddah, Saudi Arabia

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0009-0007-6610-0054

Corresponding author's ORCID profile: https://orcid.org/0009-0007-6610-0054

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.01.002

Abstract

This study examines the applicability of the Fama-French 3-factor model to Real Estate Investment Trusts (REITs) in emerging economies using monthly data from January 2016 to December 2023 for 23 REITs across five emerging markets. A Generalized Method of Moments (GMM) (system) approach assesses the impact of 12 explanatory variables, including traditional factors like market, value, size, and momentum premiums, as well as emerging market-specific factors such as the Morgan Stanley Capital International (MSCI) Emerging Markets Currency Index and Bloomberg Commodity Ex-Agriculture Index. Control variables like political stability, foreign direct investment, and portfolio investment are also included. The results show that value premium, foreign direct investment, portfolio investment, and commodity prices positively influence REIT excess returns, while momentum premium and political instability negatively affect them. These findings highlight the combined importance of traditional and emerging market-specific factors, emphasizing the critical role of stable political conditions for REIT performance. This research contributes valuable insights for investors and policymakers in understanding REIT dynamics in emerging markets.

© 2024 The Authors. Published by IASE.

This is an

Keywords

REIT performance, Emerging markets, Fama-French model, Political stability, Investment factors

Article history

Received 20 July 2024, Received in revised form 21 November 2024, Accepted 7 December 2024

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Baghlaf N, Shaheen R, and Daou LE (2025). Explaining REIT returns in emerging economies: A Fama-French approach with foreign investment and political stability. International Journal of Advanced and Applied Sciences, 12(1): 7-18

Figures

{kind=link}

Tables

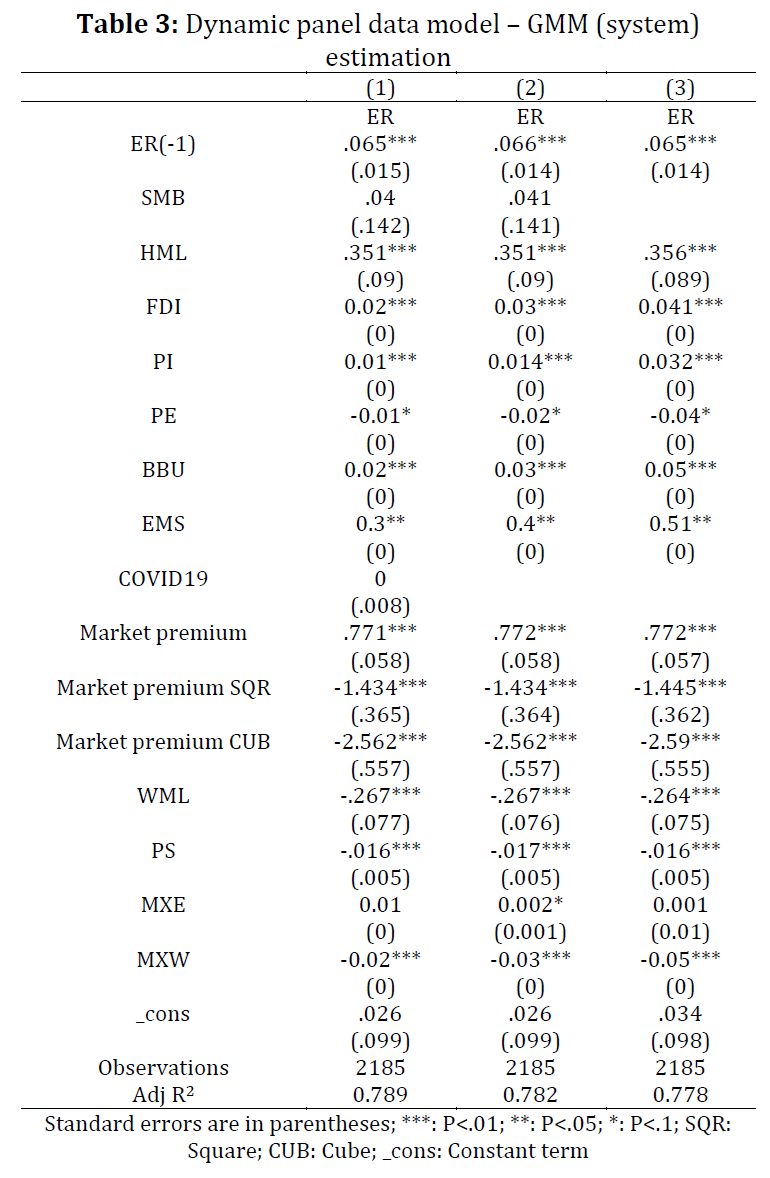

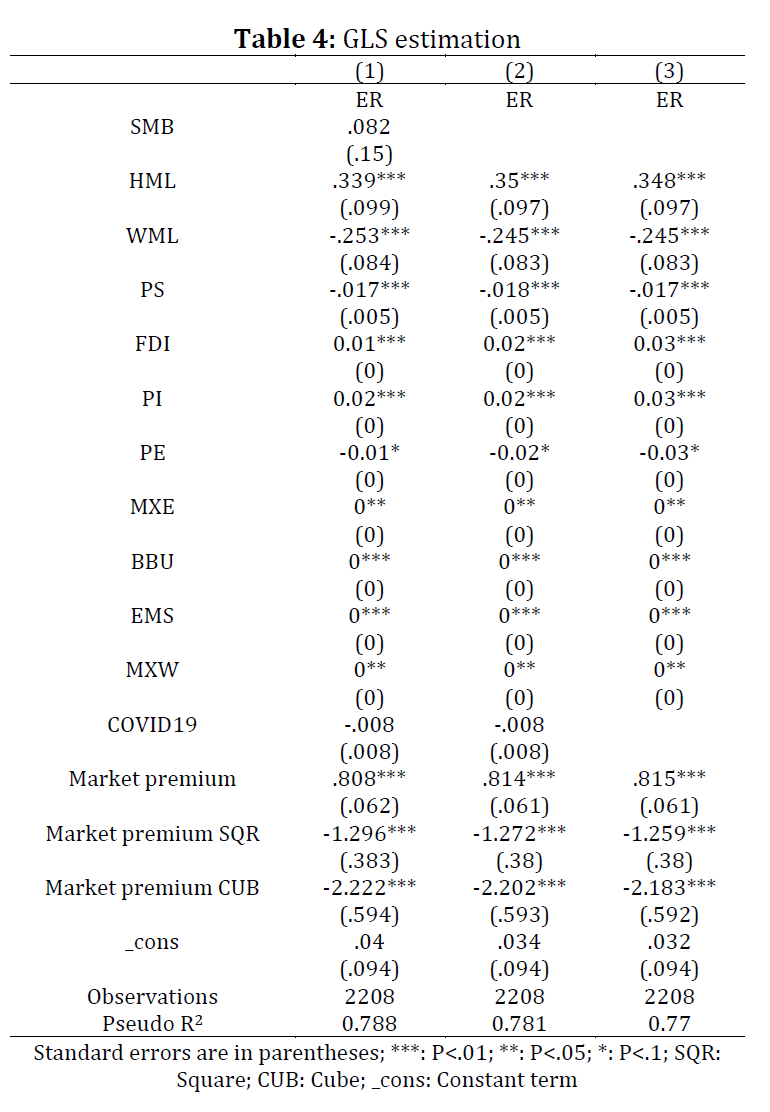

Table 1 Table 2 Table 3 Table 4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (36)

- Aldaarmi A, Abbod M, and Salameh H (2015). Implement Fama and French and capital asset pricing models in Saudi Arabia stock market. The Journal of Applied Business Research, 31(3): 953-968. https://doi.org/10.19030/jabr.v31i3.9228 [Google Scholar]

- Allen MT, Madura J, and Springer TM (2000). REIT characteristics and the sensitivity of REIT returns. The Journal of Real Estate Finance and Economics, 21: 141-152. https://doi.org/10.1023/A:1007839809578 [Google Scholar]

- Bhargava V and Weeks HS (2022). Short-term REIT performance under pandemic conditions. Journal of Real Estate Portfolio Management, 28(1): 62-77. https://doi.org/10.1080/10835547.2022.2064594 [Google Scholar]

- Block RL (2011). Investing in REITs: Real estate investment trusts. John Wiley and Sons, Hoboken, USA. https://doi.org/10.1002/9781119202325 [Google Scholar]

- Blundell R and Bond S (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1): 115-143. https://doi.org/10.1016/S0304-4076(98)00009-8 [Google Scholar]

- Bouri E, Demirer R, Gupta R, and Nel J (2021). COVID-19 pandemic and investor herding in international stock markets. Risks, 9(9): 168. https://doi.org/10.3390/risks9090168 [Google Scholar]

- Carhart MM (1997). On persistence in mutual fund performance. The Journal of Finance, 52(1): 57-82. https://doi.org/10.1111/j.1540-6261.1997.tb03808.x [Google Scholar]

- Chaudhry MK, Bhargava V, and Weeks HS (2022). Impact of economic forces and fundamental variables on REIT returns. Applied Economics, 54(53): 6179-6201. https://doi.org/10.1080/00036846.2022.2059438 [Google Scholar]

- Chen NF and Zhang F (1998). Risk and return of value stocks. The Journal of Business, 71(4): 501-535. https://doi.org/10.1086/209755 [Google Scholar]

- Chui AC, Titman S, and Wei KJ (2003). Intra-industry momentum: The case of REITs. Journal of Financial Markets, 6(3): 363-387. https://doi.org/10.1016/S1386-4181(03)00002-8 [Google Scholar]

- Clayton J and MacKinnon G (2003). The relative importance of stock, bond and real estate factors in explaining REIT returns. The Journal of Real Estate Finance and Economics, 27: 39-60. https://doi.org/10.1023/A:1023607412927 [Google Scholar]

- Coşkun Y, Selcuk-Kestel AS, and Yilmaz B (2017). Diversification benefit and return performance of REITs using CAPM and Fama-French: Evidence from Turkey. Borsa Istanbul Review, 17(4): 199-215. https://doi.org/10.1016/j.bir.2017.08.003 [Google Scholar]

- Eun C, Wang L, and Zhang T (2022). House price growth synchronization and business cycle alignment. The Journal of Real Estate Finance and Economics, 65: 675-710. https://doi.org/10.1007/s11146-021-09849-x [Google Scholar]

- Fama EF and French KR (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1): 3-56. https://doi.org/10.1016/0304-405X(93)90023-5 [Google Scholar]

- Goebel PR, Harrison DM, Mercer JM, and Whitby RJ (2013). REIT momentum and characteristic-related REIT returns. The Journal of Real Estate Finance and Economics, 47: 564-581. https://doi.org/10.1007/s11146-012-9371-2 [Google Scholar]

- Gyourko J and Keim DB (1992). What does the stock market tell us about real estate returns? Real Estate Economics, 20(3): 457-485. https://doi.org/10.1111/1540-6229.00591 [Google Scholar]

- Harrison DM, Panasian CA, and Seiler MJ (2011). Further evidence on the capital structure of REITs. Real Estate Economics, 39(1): 133-166. https://doi.org/10.1111/j.1540-6229.2010.00289.x [Google Scholar]

- He F and Neo KT (2021). Application of the Fama-French model to Singapore REITs. Ph.D. Dissertation, Massachusetts Institute of Technology, Cambridge, USA. [Google Scholar]

- Idzorek TM and Kowara M (2013). Factor-based asset allocation vs. asset-class-based asset allocation. Financial Analysts Journal, 69(3): 19-29. https://doi.org/10.2469/faj.v69.n3.7 [Google Scholar]

- Ijasan K, Junior PO, Tweneboah G, and Adam AM (2021). How does South Africa's real estate investment trusts integrate with major global REITs markets? A time-frequency approach. Scientific African, 14: e00993. https://doi.org/10.1016/j.sciaf.2021.e00993 [Google Scholar]

- Jackson LA (2020). An application of the Fama–French three-factor model to lodging REITs: A 20-year analysis. Tourism and Hospitality Research, 20(1): 31-40. https://doi.org/10.1177/1467358418798141 [Google Scholar]

- Jegadeesh N and Titman S (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance, 48: 65-91. https://doi.org/10.1111/j.1540-6261.1993.tb04702.x [Google Scholar]

- Karolyi GA and Sanders AB (1998). The variation of economic risk premiums in real estate returns. The Journal of Real Estate Finance and Economics, 17: 245-262. https://doi.org/10.1023/A:1007776907309 [Google Scholar]

- Khan S and Siddiqui DA (2019). Factor affecting the performance of REITs: An evidence from different markets. https://doi.org/10.2139/ssrn.3397481 [Google Scholar]

- Lakonishok J, Shleifer A, and Vishny RW (1994). Contrarian investment, extrapolation, and risk. The Journal of Finance, 49(5): 1541-1578. https://doi.org/10.1111/j.1540-6261.1994.tb04772.x [Google Scholar]

- Liu X and Zhang C (2017). Corporate governance, social responsibility information disclosure, and enterprise value in China. Journal of Cleaner Production, 142: 1075-1084. https://doi.org/10.1016/j.jclepro.2016.09.102 [Google Scholar]

- McMillan MG, Pinto JE, Pirie W, and Venter GVD (2011). Investments principles of portfolio and equity analysis. 1st Edition, John Wiley and Sons, Hoboken, USA. [Google Scholar]

- Novy-Marx R (2013). The other side of value: The gross profitability premium. Journal of Financial Economics, 108(1): 1-28. https://doi.org/10.1016/j.jfineco.2013.01.003 [Google Scholar]

- Okoro C and Ayaba MM (2023). Research trends and directions on real estate investment trusts' performance risks. Sustainability, 15(6): 5436. https://doi.org/10.3390/su15065436 [Google Scholar]

- Ooi J, Webb J, and Zhou D (2007). Extrapolation theory and the pricing of REIT stocks. Journal of Real Estate Research, 29(1): 27-56. https://doi.org/10.1080/10835547.2007.12091192 [Google Scholar]

- Salisu AA, Akinsomi O, Ametefe FK, and Hammed YS (2024). Gold market volatility and REITs' returns during tranquil and turbulent episodes. International Review of Financial Analysis, 95: 103348. https://doi.org/10.1016/j.irfa.2024.103348 [Google Scholar]

- Shen J, Hui EC, and Fan K (2021). The beta anomaly in the REIT market. The Journal of Real Estate Finance and Economics, 63: 414-436. https://doi.org/10.1007/s11146-020-09784-3 [Google Scholar]

- Shleifer A and Vishny RW (1997). The limits of arbitrage. The Journal of Finance, 52: 35-55. https://doi.org/10.1111/j.1540-6261.1997.tb03807.x [Google Scholar]

- Titman S, Tompaidis S, and Tsyplakov S (2005). Determinants of credit spreads in commercial mortgages. Real Estate Economics, 33(4): 711-738. https://doi.org/10.1111/j.1540-6229.2005.00136.x [Google Scholar]

- Zhang W, Li B, and Roca E (2023). Moments and momentum in the returns of securitized real estate: A cross-country study of risk factors driving real estate investment trusts before and during COVID-19. Heliyon, 9(8): e18476. https://doi.org/10.1016/j.heliyon.2023.e18476 [Google Scholar] PMid:37529343 PMCid:PMC10388167

- Zhang Y and Hansz JA (2022). Industry concentration and US REIT returns. Real Estate Economics, 50(1): 247-267. https://doi.org/10.1111/1540-6229.12278 [Google Scholar]