International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 11, Issue 9 (September 2024), Pages: 66-75

----------------------------------------------

Original Research Paper

Accounting outsourcing intensity in Vietnam: Empirical evidence from Vietnamese small and medium-sized enterprises

Author(s):

Affiliation(s):

1School of Accounting and Auditing, National Economics University, Hanoi, Vietnam

2Faculty of Finance and Banking, Thuongmai University, Hanoi, Vietnam

3Faculty of Economics and International Business, Thuongmai University, Hanoi, Vietnam

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-1626-6167

Corresponding author's ORCID profile: https://orcid.org/0000-0002-1626-6167

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2024.09.008

Abstract

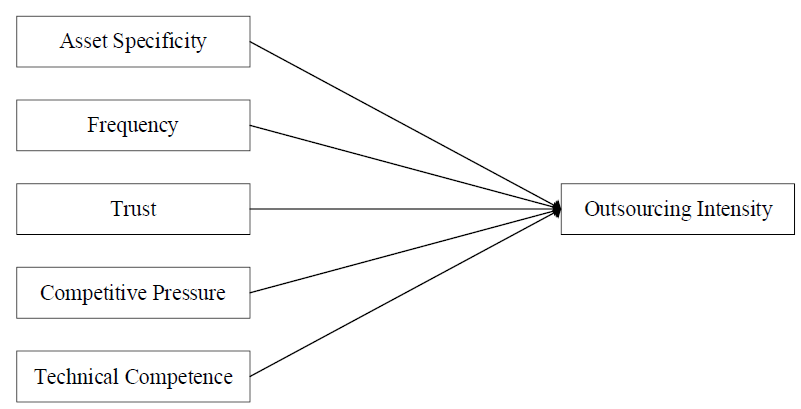

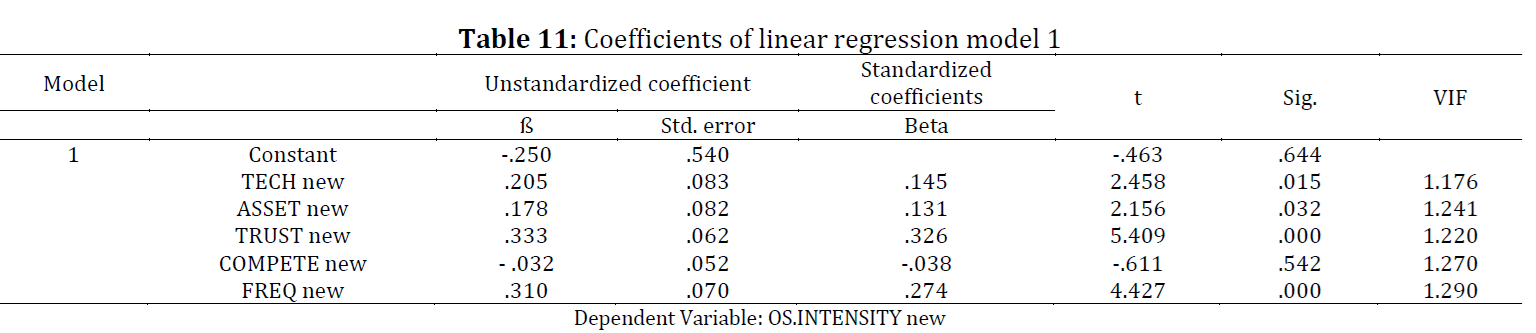

This study focuses on developing a strategic management tool for small and medium-sized enterprises (SMEs), where outsourcing is seen as an effective method. Outsourcing allows SMEs to concentrate on their core strengths and compete despite limited resources. In Vietnam, SMEs make up over ninety percent of all businesses and play a key role in the economy. However, they face challenges due to limited resources, especially in managing accounting functions. This research examines the factors influencing the level of outsourcing among SMEs in Vietnam based on two key theories: Transaction Cost Theory (TCE) and the Resource-Based View (RBV). A sample of 236 questionnaires was analyzed using SPSS and regression models. The findings revealed positive and significant relationships between outsourcing intensity (OS.Intensity) and four factors: asset specificity (AS), frequency of accounting tasks (FREQ), trust (TRUST), and technology competence (TECH). The study supports the trend of accounting outsourcing for Vietnamese SMEs, allowing them to enhance their internal strengths despite resource constraints. Future research to gain a deeper understanding of accounting outsourcing is also suggested.

© 2024 The Authors. Published by IASE.

This is an

Keywords

Outsourcing intensity, Small and medium-sized enterprises, Transaction cost theory, Resource-based view, Accounting functions

Article history

Received 26 February 2024, Received in revised form 17 August 2024, Accepted 3 September 2024

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Nguyen LH, Tran CQ, Nguyen TL, and Doan NM (2024). Accounting outsourcing intensity in Vietnam: Empirical evidence from Vietnamese small and medium-sized enterprises. International Journal of Advanced and Applied Sciences, 11(9): 66-75

Figures

{kind=link}

Tables

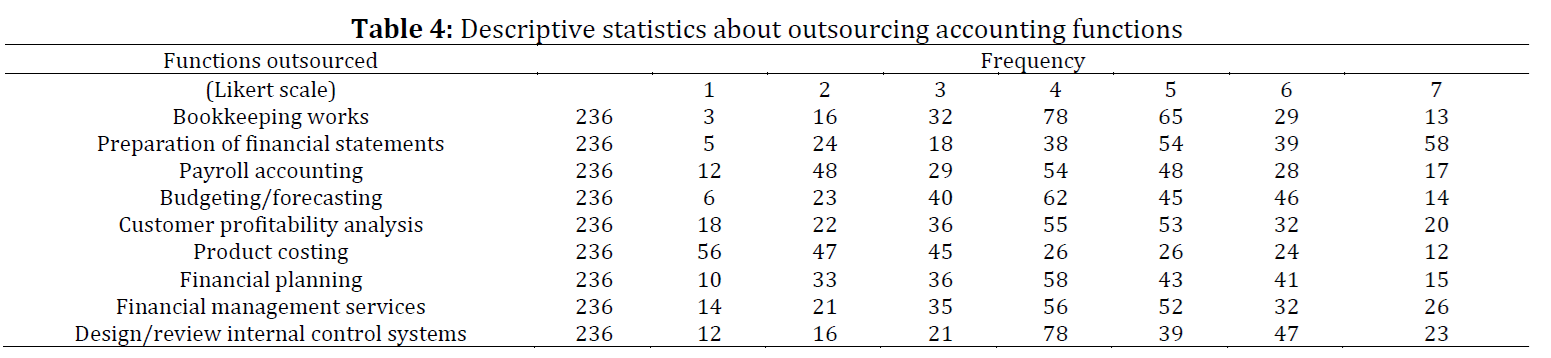

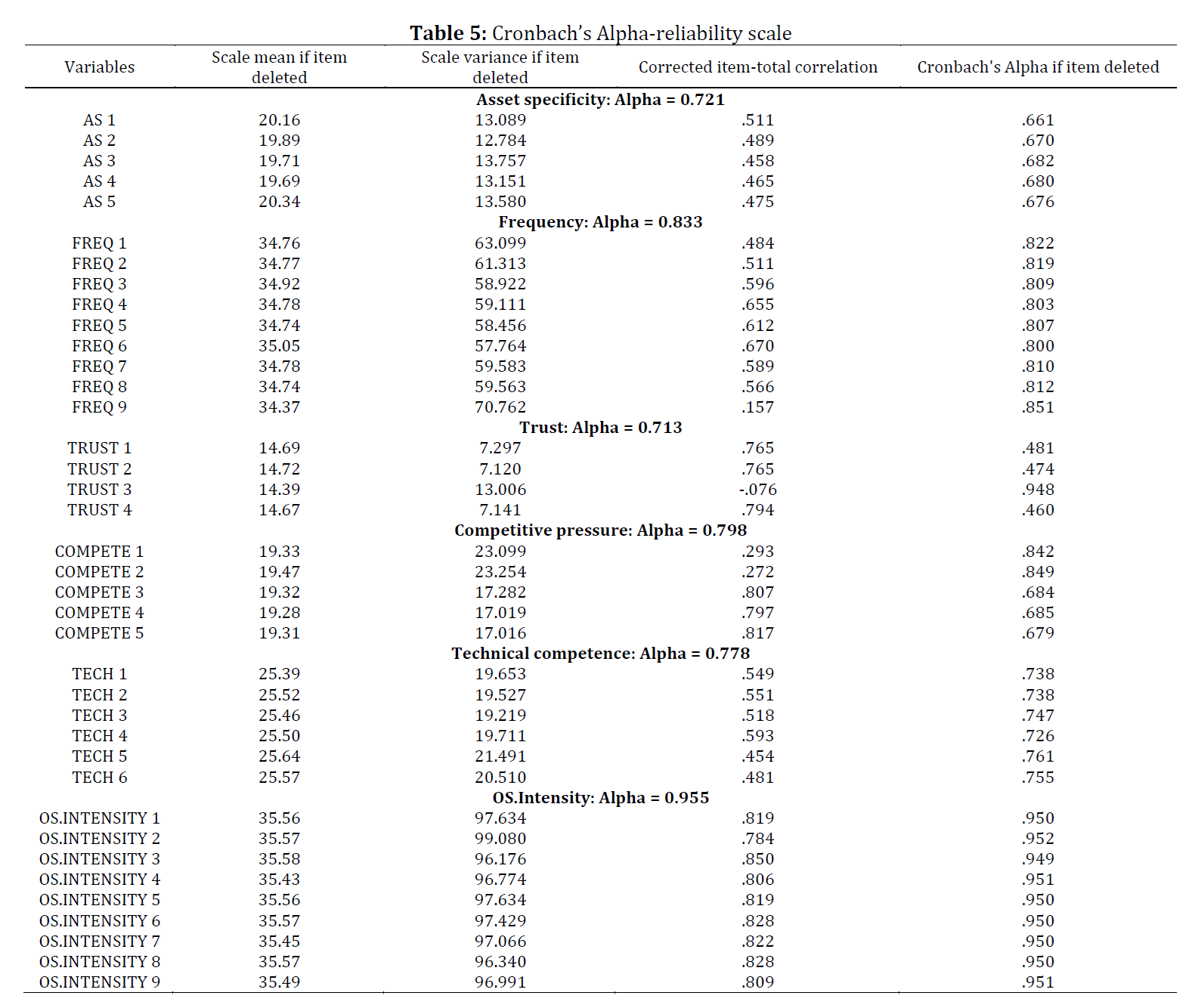

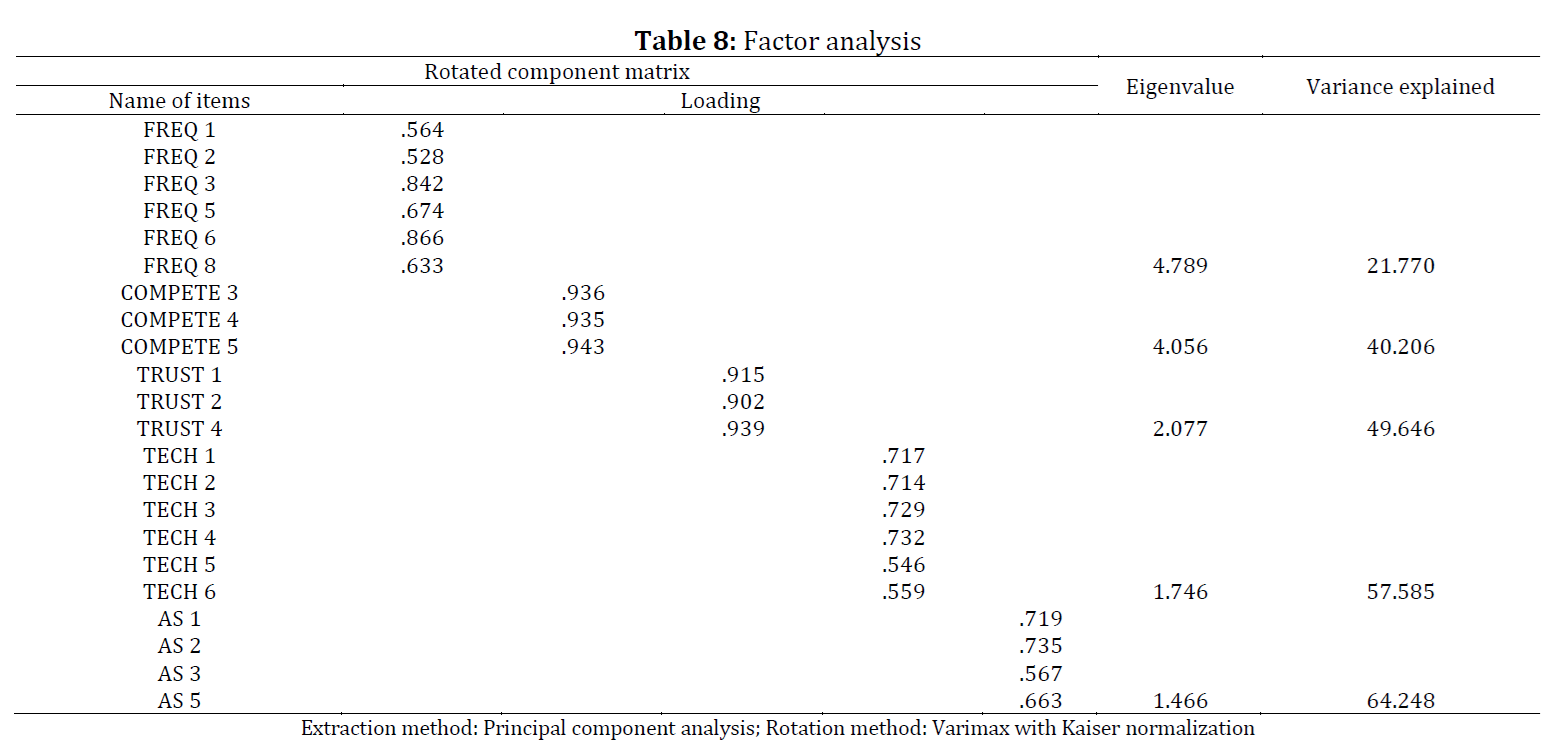

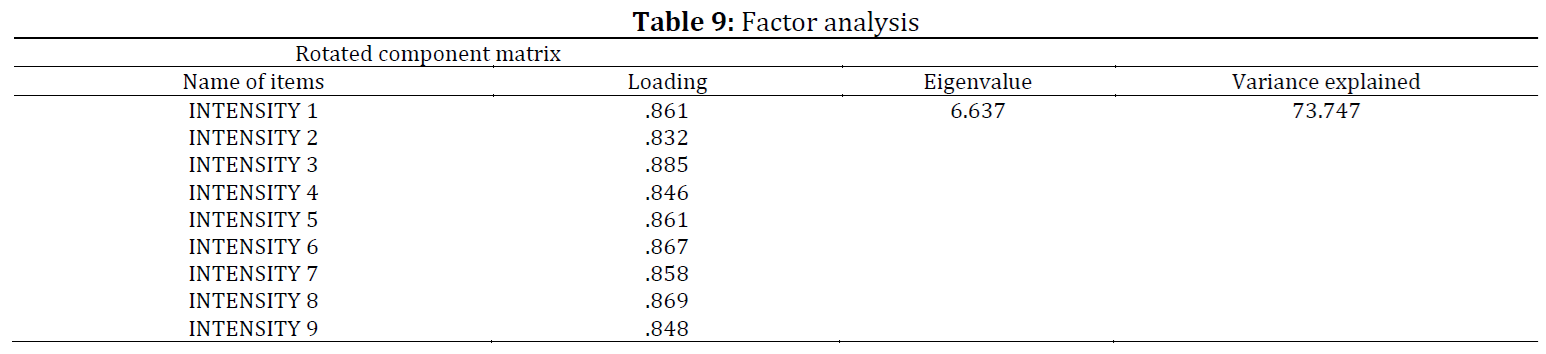

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8 Table 9 Table 10 Table 11

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (44)

- Adekoya O and Ojediran S (2024). Outsourcing accounting functions and the quality of financial reporting for SMEs in Lagos State. European Journal of Accounting, Auditing and Finance Research, 12(5): 82-100. https://doi.org/10.37745/ejaafr.2013/vol12n582100 [Google Scholar]

- Anderson SJ and McKenzie D (2022). Improving business practices and the boundary of the entrepreneur: A randomized experiment comparing training, consulting, insourcing, and outsourcing. Journal of Political Economy, 130(1): 157-209. https://doi.org/10.1086/717044 [Google Scholar]

- Bagieńska A (2016). The demand for professional knowledge as a key factor of the development of outsourcing of financial and accounting services in Poland. Business, Management and Education, 14(1): 19-33. https://doi.org/10.3846/bme.2016.313 [Google Scholar]

- Barney J (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1): 99-120. https://doi.org/10.1177/014920639101700108 [Google Scholar]

- Berry AJ, Sweeting R, and Goto J (2006). The effect of business advisers on the performance of SMEs. Journal of Small Business and Enterprise Development, 13(1): 33-47. https://doi.org/10.1108/14626000610645298 [Google Scholar]

- Blackburn R, Carey P, and Tanewski GA (2010). Business advice to SMEs: Professional competence, trust and ethics. ACCA Research Report No. 119, Association of Chartered Certified Accountants, London, UK. [Google Scholar]

- Bolcu LD and Boharu MR (2021). Outsourcing of the accounting and financial function. Ovidius University Annals, Economic Sciences Series, 21(2): 953-961. https://doi.org/10.61801/OUAESS.2021.2.130 [Google Scholar]

- Burko K (2022). Advantages and risks of accounting outsourcing. Three Seas Economic Journal, 3(2): 44-51. https://doi.org/10.30525/2661-5150/2022-2-6 [Google Scholar]

- Carey P, Subramaniam N, and Ching KCW (2006). Internal audit outsourcing in Australia. Accounting and Finance, 46(1): 11-30. https://doi.org/10.1111/j.1467-629X.2006.00159.x [Google Scholar]

- Coase RH (1937). The nature of the firm. Economica, 4(16): 386-405. https://doi.org/10.1111/j.1468-0335.1937.tb00002.x [Google Scholar]

- Daou A, Karuranga E, and Su Z (2013). Intellectual capital in Mexican SMEs from the perspective of the resource-based and dynamic capabilities views. Journal of Applied Business Research, 29(6): 1673-1688. https://doi.org/10.19030/jabr.v29i6.8206 [Google Scholar]

- Dekker HC, Kawai T, and Sakaguchi J (2018). Contracting abroad: A comparative analysis of contract design in host and home country outsourcing relations. Management Accounting Research, 40: 47-61. https://doi.org/10.1016/j.mar.2017.09.003 [Google Scholar]

- Espino-Rodríguez TF and Padrón-Robaina V (2005). A resource-based view of outsourcing and its implications for organizational performance in the hotel sector. Tourism Management, 26(5): 707-721. https://doi.org/10.1016/j.tourman.2004.03.013 [Google Scholar]

- Espino-Rodríguez TF and Rodríguez‐Díaz M (2008). Effects of internal and relational capabilities on outsourcing: An integrated model. Industrial Management and Data Systems, 108(3): 328-345. https://doi.org/10.1108/02635570810858750 [Google Scholar]

- Everaert P, Sarens G, and Rommel J (2010). Using transaction cost economics to explain outsourcing of accounting. Small Business Economics, 35: 93-112. https://doi.org/10.1007/s11187-008-9149-3 [Google Scholar]

- Gooderham PN, Tobiassen A, Døving E, and Nordhaug O (2004). Accountants as sources of business advice for small firms. International Small Business Journal, 22(1): 5-22. https://doi.org/10.1177/0266242604039478 [Google Scholar]

- Gottschalk P and Solli‐Sæther H (2006). Maturity model for IT outsourcing relationships. Industrial Management and Data Systems, 106(2): 200-212. https://doi.org/10.1108/02635570610649853 [Google Scholar]

- Greenberg PS, Greenberg RH, and Lederer Antonucci Y (2008). The role of trust in the governance of business process outsourcing relationships: A transaction cost economics approach. Business Process Management Journal, 14(5): 593-608. https://doi.org/10.1108/14637150810903011 [Google Scholar]

- Hancox M and Hackney R (1999). Information technology outsourcing: Conceptualizing practice in the public and private sector. In the 32nd Annual Hawaii International Conference on Systems Sciences: Abstracts and CD-ROM of Full Papers, IEEE, Maui, USA: 1-15. https://doi.org/10.1109/HICSS.1999.772971 [Google Scholar]

- Jayabalan J, Raman M, Dorasamy M, and Ching NKC (2009). Outsourcing of accounting functions amongst SME companies in Malaysia: An exploratory study. Accountancy Business and the Public Interest, 8(2): 96-114. [Google Scholar]

- Jiang B, Belohlav JA, and Young ST (2007). Outsourcing impact on manufacturing firms’ value: Evidence from Japan. Journal of Operations Management, 25(4): 885-900. https://doi.org/10.1016/j.jom.2006.12.002 [Google Scholar]

- Kamyabi Y and Devi SS (2011). An empirical investigation of accounting outsourcing in Iranian SMEs: Transaction cost economics and resource-based views. International Journal of Business and Management, 6(3): 81-94. https://doi.org/10.5539/ijbm.v6n3p81 [Google Scholar]

- Kang M, Wu X, and Hong P (2009). Strategic outsourcing practices of multi‐national corporations (MNCs) in China. Strategic Outsourcing: An International Journal, 2(3): 240-256. https://doi.org/10.1108/17538290911005153 [Google Scholar]

- Kim J, So S, and Lee Y (2007). The effects of trust on the intention of adopting business process outsourcing: An empirical study. International Journal of Computer Science and Network Security, 7(10): 118-123. [Google Scholar]

- Lamminmaki D (2005). Why do hotels outsource? An investigation using asset specificity. International Journal of Contemporary Hospitality Management, 17(6): 516-528. https://doi.org/10.1108/09596110510612158 [Google Scholar]

- Lamminmaki D (2007). Outsourcing in Australian hotels: A transaction cost economics perspective. Journal of Hospitality and Tourism Research, 31(1): 73-110. https://doi.org/10.1177/1096348006296714 [Google Scholar]

- Lamminmaki D (2008). Accounting and the management of outsourcing: An empirical study in the hotel industry. Management Accounting Research, 19(2): 163-181. https://doi.org/10.1016/j.mar.2008.02.002 [Google Scholar]

- Logan MS (2000). Using agency theory to design successful outsourcing relationships. The International Journal of Logistics Management, 11(2): 21-32. https://doi.org/10.1108/09574090010806137 [Google Scholar]

- Lowe P and Talbot H (2000). Providing advice and information in support of rural microbusinesses. Research report, University of Newcastle, Callaghan, Australia. [Google Scholar]

- McIvor R (2009). How the transaction cost and resource-based theories of the firm inform outsourcing evaluation. Journal of Operations Management, 27(1): 45-63. https://doi.org/10.1016/j.jom.2008.03.004 [Google Scholar]

- Nagle F, Seamans R, and Tadelis S (2020). Transaction cost economics in the digital economy: A research agenda. Working Paper 21-009, Harvard Business School, Boston, USA. https://doi.org/10.2139/ssrn.3661856 [Google Scholar]

- Nicholson B, Jones J, and Espenlaub S (2006). Transaction costs and control of outsourced accounting: Case evidence from India. Management Accounting Research, 17(3): 238-258. https://doi.org/10.1016/j.mar.2006.05.002 [Google Scholar]

- Poppo L and Zenger T (1998). Testing alternative theories of the firm: Transaction cost, knowledge‐based, and measurement explanations for make‐or‐buy decisions in information services. Strategic Management Journal, 19(9): 853-877. https://doi.org/10.1002/(SICI)1097-0266(199809)19:9<853::AID-SMJ977>3.0.CO;2-B [Google Scholar]

- Reeves KA, Caliskan F, and Ozcan O (2010). Outsourcing distribution and logistics services within the automotive supplier industry. Transportation Research Part E: Logistics and Transportation Review, 46(3): 459-468. https://doi.org/10.1016/j.tre.2009.10.001 [Google Scholar]

- Rogosic A (2019). Accounting outsourcing issues. Eurasian Journal of Business and Management, 7(3): 44-53. https://doi.org/10.15604/ejbm.2019.07.03.005 [Google Scholar]

- Rousseau DM, Sitkin SB, Burt RS, and Camerer C (1998). Not so different after all: A cross-discipline view of trust. Academy of Management Review, 23(3): 393-404. https://doi.org/10.5465/amr.1998.926617 [Google Scholar]

- Scott JM and Irwin D (2009). Discouraged advisees? The influence of gender, ethnicity, and education in the use of advice and finance by UK SMEs. Environment and Planning C: Government and Policy, 27(2): 230-245. https://doi.org/10.1068/c0806b [Google Scholar]

- Sian S and Roberts C (2009). UK small owner‐managed businesses: Accounting and financial reporting needs. Journal of Small Business and Enterprise Development, 16(2): 289-305. https://doi.org/10.1108/14626000910956065 [Google Scholar]

- Spekle RF, Van Elten HJ, and Kruis AM (2007). Sourcing of internal auditing: An empirical study. Management Accounting Research, 18(1): 102-124. https://doi.org/10.1016/j.mar.2006.10.001 [Google Scholar]

- Stratman JK (2008). Facilitating offshoring with enterprise technologies: Reducing operational friction in the governance and production of services. Journal of Operations Management, 26(2): 275-287. https://doi.org/10.1016/j.jom.2007.02.006 [Google Scholar]

- Tomašević I, Đurović S, Abramović N, Weis L, and Koval V (2023). Factors influencing accounting outsourcing using the transaction cost economics model. International Journal of Financial Studies, 11(2): 61. https://doi.org/10.3390/ijfs11020061 [Google Scholar]

- Verwaal E, Verdu AJ, and Recter A (2008). Transaction costs and organisational learning in strategic outsourcing relationships. International Journal of Technology Management, 41(1-2): 38-54. https://doi.org/10.1504/IJTM.2008.015983 [Google Scholar]

- Widener SK and Selto FH (1999). Management control systems and boundaries of the firm: Why do firms outsource internal auditing activities? Journal of Management Accounting Research, 11: 45-73. [Google Scholar]

- Williamson OE (1983). Credible commitments: Using hostages to support exchange. The American Economic Review, 73(4): 519-540. [Google Scholar]