International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 11, Issue 8 (August 2024), Pages: 220-228

----------------------------------------------

Original Research Paper

The impact of Reserve Bank of India officials' resignations on financial sector returns: An event-study analysis

Author(s):

Affiliation(s):

1Insurance and Banking Department, College of Business Studies, Public Authority for Applied Education and Training, Ardiya, Kuwait

2Economics Department, College of Business Administration, Kuwait University, Al-Shadadiya, Kuwait

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-4920-3867

Corresponding author's ORCID profile: https://orcid.org/0000-0002-4920-3867

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2024.08.023

Abstract

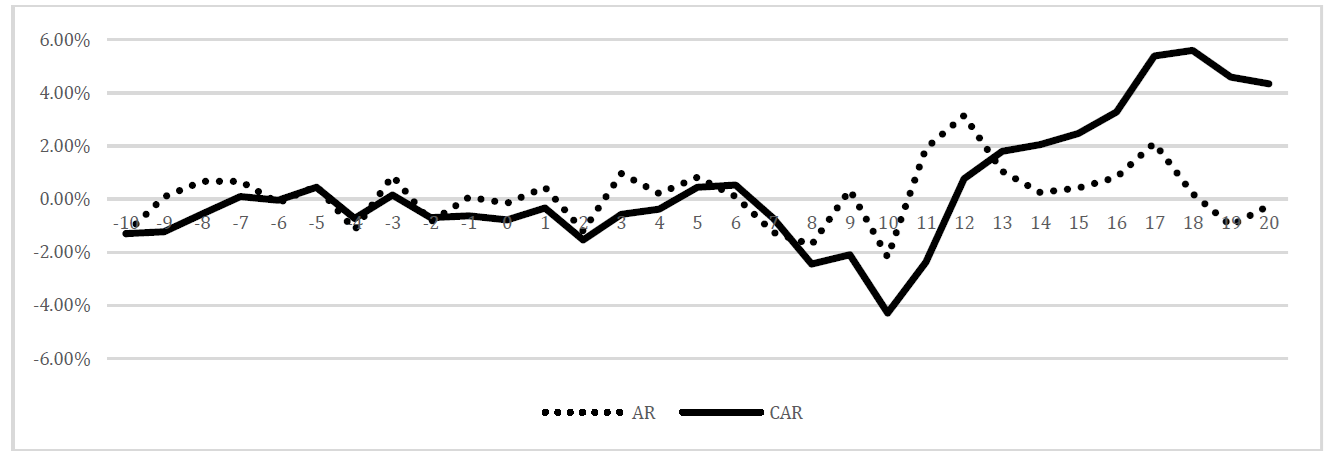

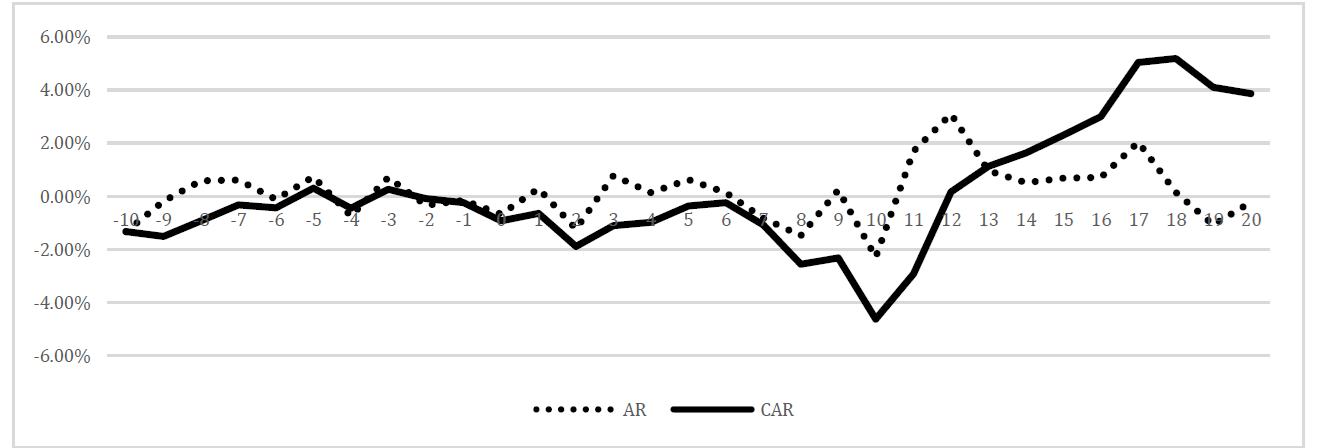

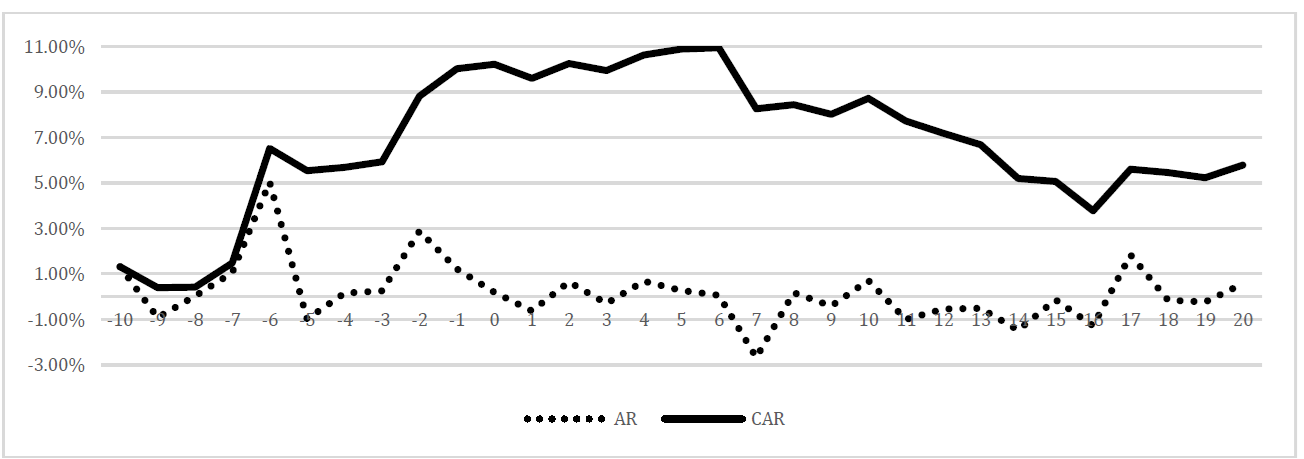

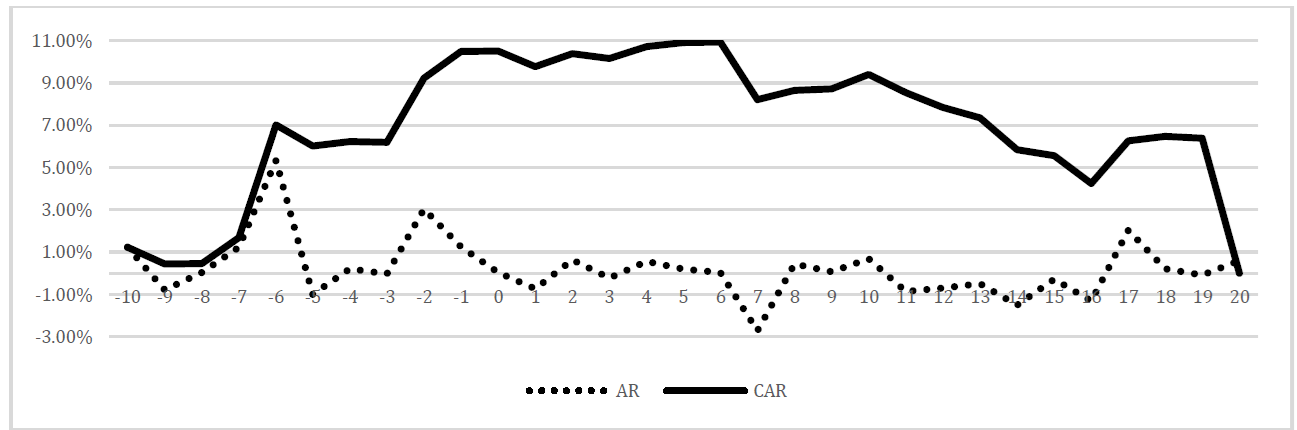

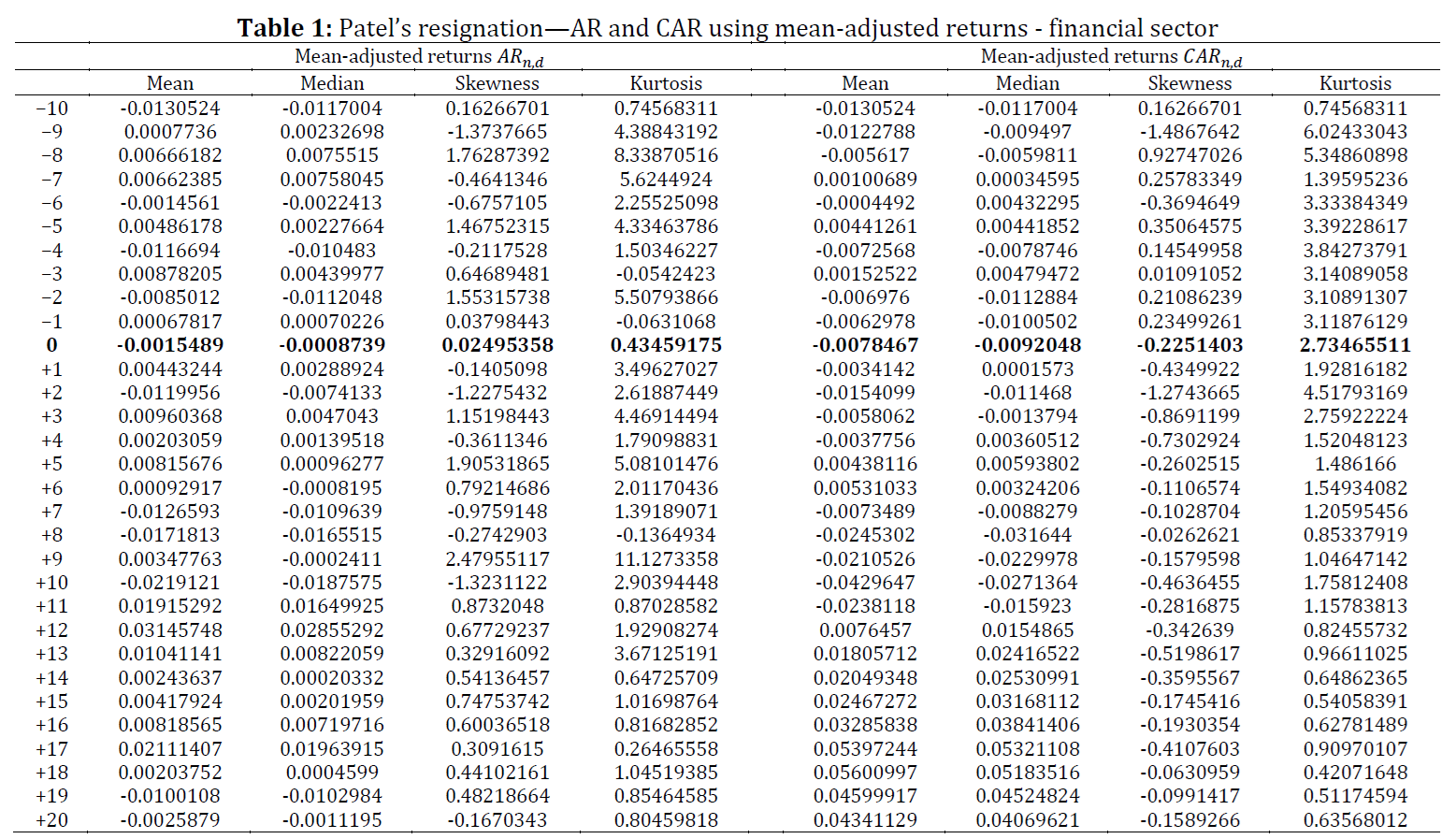

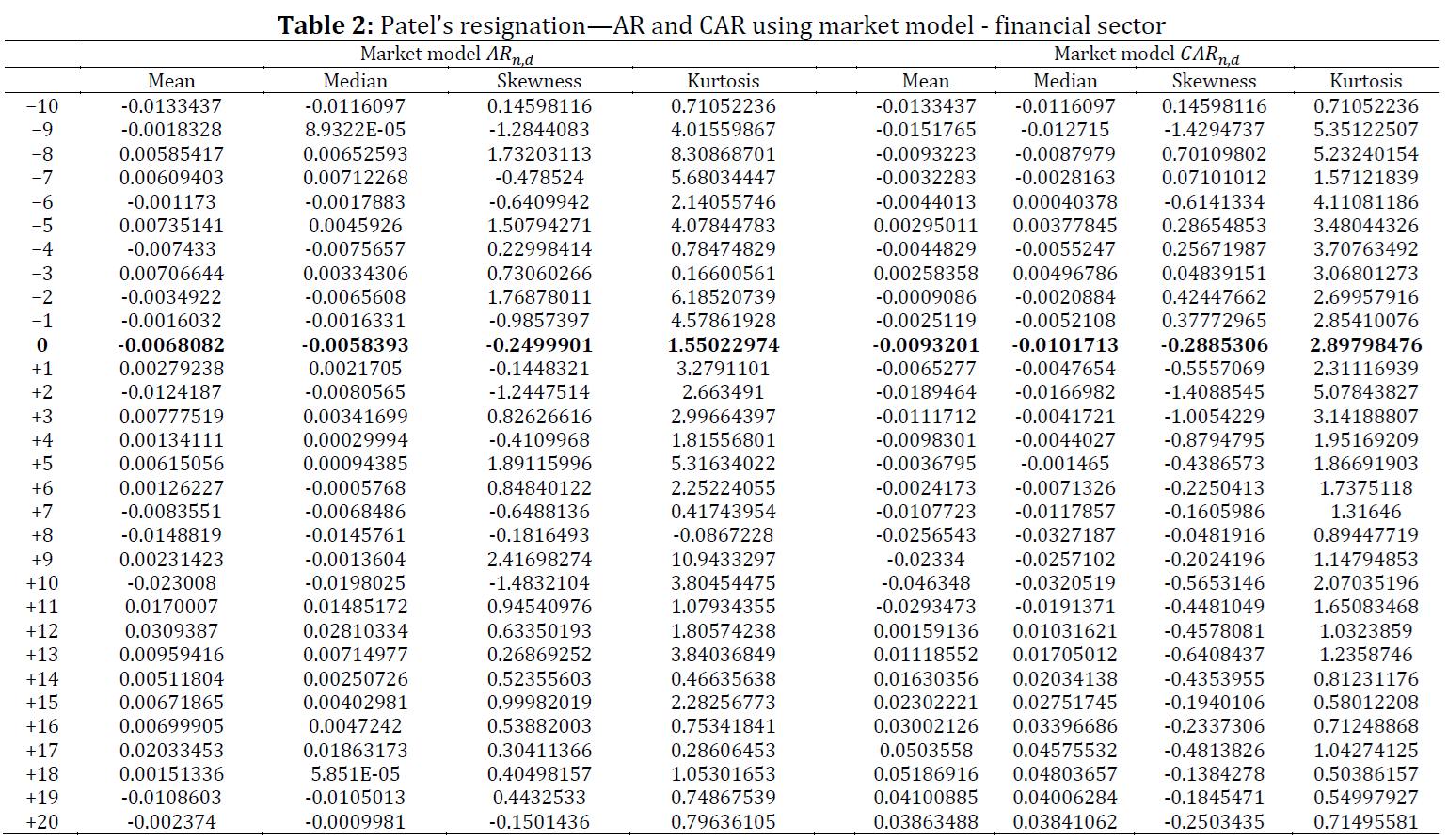

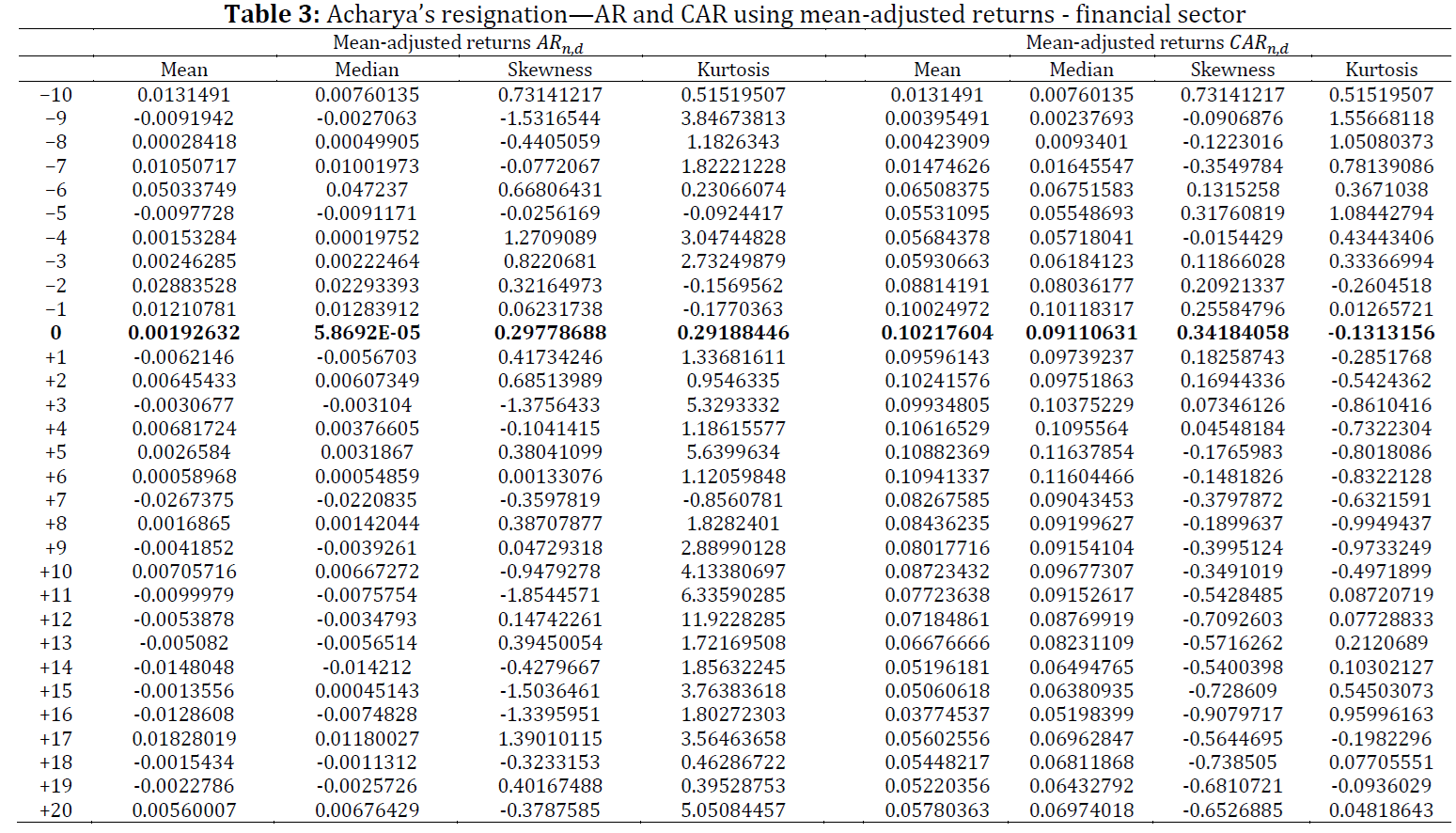

In this study, we examine the short-term effects of the resignations of high-ranking officials from the Reserve Bank of India (RBI) on financial sector returns. We apply a commonly used event-study method to analyze financial sector stocks during the period from February 16, 2018, to July 22, 2019. The findings reveal that the financial sector was sensitive to the resignations of RBI Governor Urjit Patel and Deputy Governor Viral Acharya, both strong supporters of the RBI's independence. Patel’s resignation caused a significant negative impact on cumulative abnormal returns, while Acharya’s resignation led to a significant positive impact on these returns. Our results suggest that central bank independence (CBI) may have varied short-term effects on financial sector performance. It is, therefore, important for both politicians and investors to understand the implications of our findings in order to fully grasp the political and economic consequences of central bank independence and the credibility of monetary policy on financial sector outcomes. For future research, we suggest exploring the effects of these resignations on other financial indicators, such as bond yields, exchange rates, and interest rates, using alternative methods.

© 2024 The Authors. Published by IASE.

This is an

Keywords

Central bank independence, Financial sector returns, Event-study method, Cumulative abnormal returns, Resignation effects

Article history

Received 27 April 2024, Received in revised form 25 August 2024, Accepted 27 August 2024

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Bash A, Faras R, Al-Awadhi AM, and AlAli MS (2024). The impact of Reserve Bank of India officials' resignations on financial sector returns: An event-study analysis. International Journal of Advanced and Applied Sciences, 11(8): 220-228

Figures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (31)

- Agoba AM, Abor JY, Osei K, Sa-Aadu J, Amoah B, and Dzeha GCO (2019). Central bank independence, elections and fiscal policy in Africa: Examining the moderating role of political institutions. International Journal of Emerging Markets, 14(5): 809-830. https://doi.org/10.1108/IJOEM-08-2018-0423 [Google Scholar]

- Alesina A and Summers LH (1993). Central bank independence and macroeconomic performance: Some comparative evidence. Journal of Money, Credit and Banking, 25(2): 151. https://doi.org/10.2307/2077833 [Google Scholar]

- Anwar CJ (2023). Heterogeneity effect of central bank independence on inflation in developing countries. Global Journal of Emerging Market Economies, 15(1): 38-52. https://doi.org/10.1177/09749101221082049 [Google Scholar]

- Bartholdy J, Olsen D, and Peare P (2011). Conducting event studies on a small stock exchange. European Journal of Finance, 13(3): 227-252. https://doi.org/10.1080/13518470600880176 [Google Scholar]

- Bash A and Al-Awadhi AM (2023). Central bank independence and stock market outcomes: An event study on Borsa Istanbul. Cogent Economics and Finance, 11(1): 2186032. https://doi.org/10.1080/23322039.2023.2186032 [Google Scholar]

- Berger H, De Haan J, and Eijffinger SC (2001). Central bank independence: An update of theory and evidence. Journal of Economic Surveys, 15(1): 3-40. https://doi.org/10.1111/1467-6419.00131 [Google Scholar]

- Berger W and Kißmer F. (2019). Central bank independence and financial stability: A tale of perfect harmony? European Journal of Political Economy, 31: 109-118. https://doi.org/10.1016/j.ejpoleco.2013.04.004 [Google Scholar]

- Bhat AA, Khan JI, Bhat SA, and Parray WA (2023). Central bank independence and its impact on fiscal deficit: Evidence from India. Studia Universitatis “Vasile Goldis” Arad–Economics Series, 33(2): 71-94. https://doi.org/10.2478/sues-2023-0009 [Google Scholar]

- Bodea C and Hicks R (2015). Price stability and central bank independence: Discipline, credibility, and democratic institutions. International Organization, 69(1): 35-61. https://doi.org/10.1017/S0020818314000277 [Google Scholar]

- Brown SJ and Warner JB (1985). Using daily stock returns: The case of event studies. Journal of Financial Economics, 14(1): 3-31. https://doi.org/10.1016/0304-405X(85)90042-X [Google Scholar]

- Dodd P and Warner JB (1983). On corporate governance: A study of proxy contests. Journal of Financial Economics, 11(1-4): 401-438. https://doi.org/10.1016/0304-405X(83)90018-1 [Google Scholar]

- Förch T and Sunde U (2012). Central bank independence and stock market returns in emerging economies. Economics Letters, 115(1): 77-80. https://doi.org/10.1016/j.econlet.2011.11.030 [Google Scholar]

- Garcia MTV and Costa PMMR (2019). Central bank independence and stock market returns in developed countries. International Review of Applied Economics, 33(3): 335–352. https://doi.org/10.1080/02692171.2018.1493093 [Google Scholar]

- Gyeke-Dako A, Agbloyor EK, Agoba AM, Turkson F, and Abbey E (2022). Central bank independence, inflation, and poverty in Africa. Journal of Emerging Market Finance, 21(2): 211–236. https://doi.org/10.1177/09726527221078434 [Google Scholar]

- Harris T and Hardin JW (2013). Exact Wilcoxon signed-rank and Wilcoxon Mann–Whitney ranksum tests. The Stata Journal, 13(2): 337–343. https://doi.org/10.1177/1536867X1301300208 [Google Scholar]

- Ismail I and Suhardjo H (2001). The impact of domestic political events on an emerging stock market: The case of Indonesia. In the Proceedings of Asia Pacific Management Conference, Singapore, Singapore: 235–262. [Google Scholar]

- Klomp J and De Haan J (2010). Inflation and central bank independence: A meta‐regression analysis. Journal of Economic Surveys, 24(4): 593–621. https://doi.org/10.1111/j.1467-6419.2009.00597.x [Google Scholar]

- Kurihara Y, Morikawa K, and Takaya S (2012). Central bank’s independence and stock prices. Modern Economy, 3(6): 793–797. https://doi.org/10.4236/me.2012.36101 [Google Scholar]

- Kuttner KN and Posen AS (2010). Do markets care who chairs the central bank? Journal of Money, Credit and Banking, 42(2–3): 347–371. https://doi.org/10.1111/j.1538-4616.2009.00290.x [Google Scholar]

- Mackinlay AC (1997). Event studies in economics and finance. Journal of Economic Literature, 35(1): 13–39. [Google Scholar]

- Masciandaro D and Romelli D (2015). Ups and downs of central bank independence from the great inflation to the great recession: Theory, institutions and empirics. Financial History Review, 22(3): 259–289. https://doi.org/10.1017/S0968565015000177 [Google Scholar]

- Maxfield S (1997). Gatekeepers of growth: The international political economy of central banking in developing countries. Princeton University Press, Princeton, USA. https://doi.org/10.1515/9781400822287 [Google Scholar]

- Maynes E and Rumsey J (1993). Conducting event studies with thinly traded stocks. Journal of Banking and Finance, 17(1): 145–157. https://doi.org/10.1016/0378-4266(93)90085-R [Google Scholar]

- Mishkin F (2004). Can Inflation targeting work in emerging market countries? NBER Working Paper, National Bureau of Economic Research, Cambridge, USA. https://doi.org/10.3386/w10646 [Google Scholar]

- Moser C and Dreher A (2010). Do markets care about central bank governor changes? Evidence from emerging markets. Journal of Money, Credit and Banking, 42(8): 1589–1612. https://doi.org/10.1111/j.1538-4616.2010.00355.x [Google Scholar]

- Mukhametov O (2021). Relationship between central bank independence and foreign direct investment inflows. Asian Economic and Financial Review, 11(5): 396–405. https://doi.org/10.18488/journal.aefr.2021.115.396.405 [Google Scholar]

- Nazir M, Younus H, Kaleem A, and Anwar Z (2014). Impact of political events on stock market returns: Empirical evidence from Pakistan. Journal of Economic and Administrative Sciences, 30(1): 60–78. https://doi.org/10.1108/JEAS-03-2013-0011 [Google Scholar]

- Sargent T and Wallace N (1981). Some unpleasant monetarist arithmetic. Federal Reserve Bank of Minneapolis Quarterly Review, 5(1): 1–17. https://doi.org/10.21034/qr.531 [Google Scholar]

- Strong C and Yayi C (2021). Central bank independence, fiscal deficits and currency union: Lessons from Africa. Journal of Macroeconomics, 68: 103313. https://doi.org/10.1016/j.jmacro.2021.103313 [Google Scholar]

- Strong CO (2021). Political influence, central bank independence and inflation in Africa: A comparative analysis. European Journal of Political Economy, 69: 102004. https://doi.org/10.1016/j.ejpoleco.2021.102004 [Google Scholar]

- Ueda K and Valencia F (2014). Central bank independence and macro-prudential regulation. Economics Letters, 125(2): 327–330. https://doi.org/10.1016/j.econlet.2013.12.038 [Google Scholar]