International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 11, Issue 11 (November 2024), Pages: 198-208

----------------------------------------------

Original Research Paper

The impact of digital transformation on the accounting system effectiveness

Author(s):

Affiliation(s):

Applied College, Imam Mohammad Ibn Saud Islamic University, Riyadh, Saudi Arabia

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0009-0007-2540-4983

Corresponding author's ORCID profile: https://orcid.org/0009-0007-2540-4983

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2024.11.021

Abstract

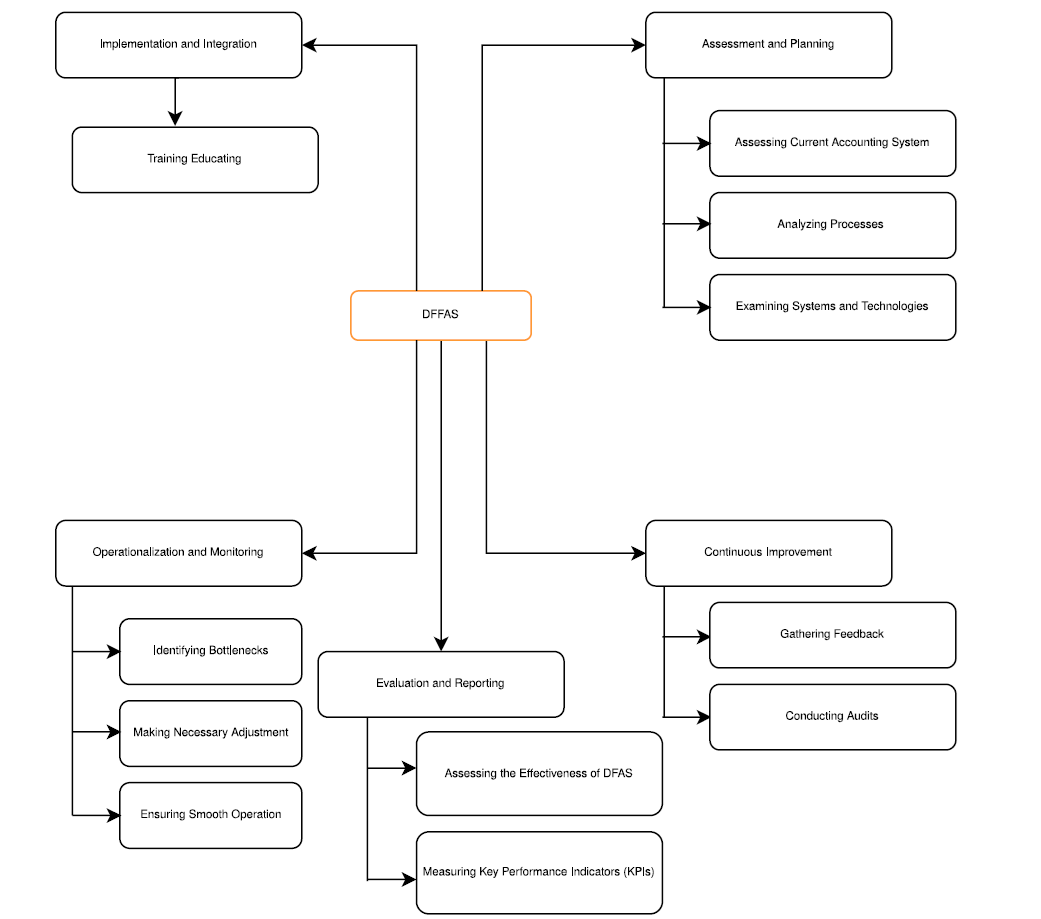

In today's rapidly changing digital landscape, most businesses in various industries have embraced digital transformation to improve their operations and efficiency. The accounting industry also has opportunities to enhance the effectiveness of its systems with new technologies. This study introduces a new framework called the Digital Transformation Framework for Accounting System Effectiveness (DTFASE), developed using design science research. The framework consists of five main stages: assessment and planning, implementation and integration, operationalization and monitoring, continuous improvement, and evaluation and reporting. Its purpose is to guide organizations in systematically transforming their accounting systems to boost overall effectiveness. By using this framework, organizations can fully leverage digital technologies to optimize their accounting processes.

© 2024 The Authors. Published by IASE.

This is an

Keywords

Digital transformation, Accounting systems, Framework development, Process optimization, System effectiveness

Article history

Received 15 July 2024, Received in revised form 29 October 2024, Accepted 8 November 2024

Acknowledgment

This work was supported and funded by the Deanship of Scientific Research at Imam Mohammad Ibn Saud Islamic University (IMSIU) (IMSIU, RG23O35).

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Alotaibi KO (2024). The impact of digital transformation on the accounting system effectiveness. International Journal of Advanced and Applied Sciences, 11(11): 198-208

Figures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

{kind=link}

{kind=link}

----------------------------------------------

References (41)

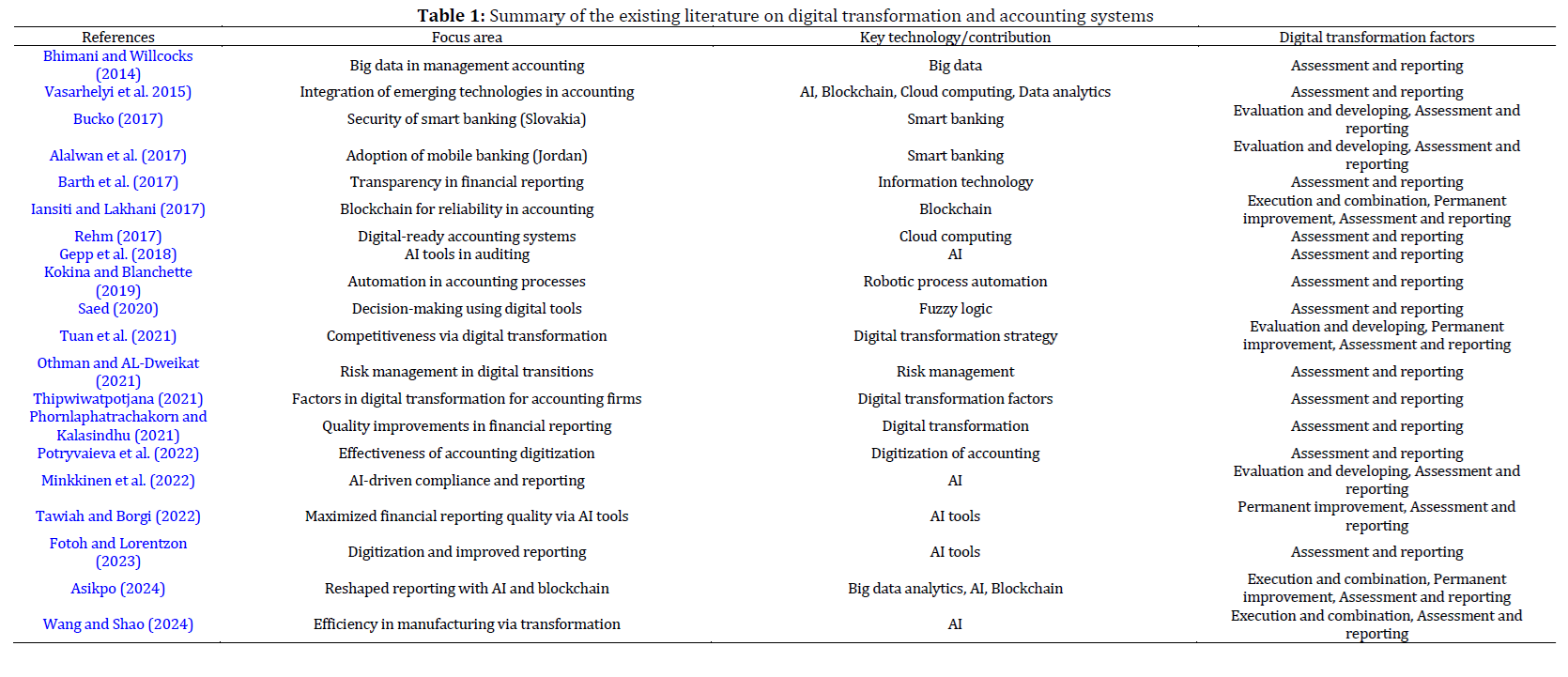

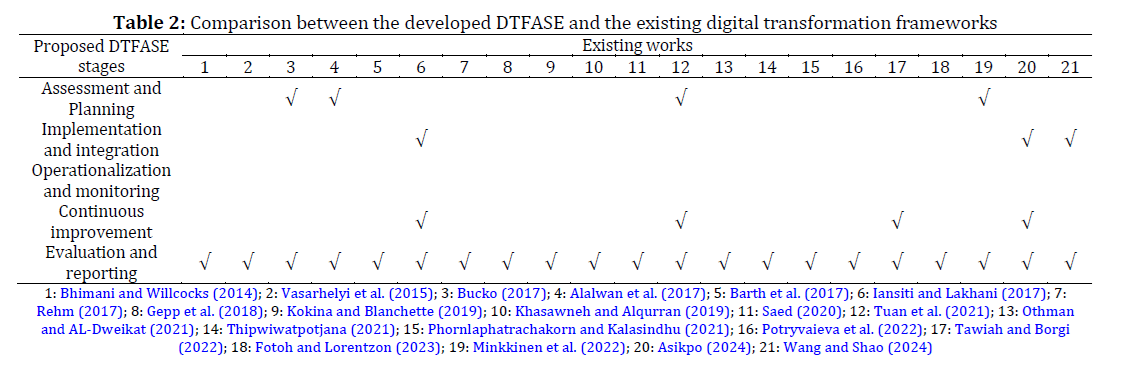

- Alalwan AA, Dwivedi YK, and Rana NP (2017). Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. International Journal of Information Management, 37(3): 99-110. https://doi.org/10.1016/j.ijinfomgt.2017.01.002 [Google Scholar]

- Asikpo NA (2024). Impact of digital transformation on financial reporting in the 21st century. International Journal of Comparative Studies and Smart Education, 1(1): 34-45. [Google Scholar]

- Barth ME, Cahan SF, Chen L, and Venter ER (2017). The economic consequences associated with integrated report quality: Capital market and real effects. Accounting, Organizations and Society, 62: 43-64. https://doi.org/10.1016/j.aos.2017.08.005 [Google Scholar]

- Bhimani A and Willcocks L (2014). Digitisation, 'Big Data' and the transformation of accounting information. Accounting and business research, 44(4): 469-490. https://doi.org/10.1080/00014788.2014.910051 [Google Scholar]

- Bonsu MOA, Wang Y, and Guo Y (2023). Does fintech lead to better accounting practices? Empirical evidence. Accounting Research Journal, 36(2/3): 129-147. https://doi.org/10.1108/ARJ-07-2022-0178 [Google Scholar]

- Bucko J (2017). Security of smart banking applications in Slovakia. Journal of Theoretical and Applied Electronic Commerce Research, 12(1): 42-52. https://doi.org/10.4067/S0718-18762017000100004 [Google Scholar]

- Coglianese C and Ben Dor LM (2020). AI in adjudication and administration. Brooklyn Law Review, 86: 791-838. [Google Scholar]

- Decman N, Mališ SS, and Sacer IM (2019). Digitalization of accounting and tax processes-challenges and opportunities for accountants and tax administrators. In the Proceedings of FEB Zagreb International Odyssey Conference on Economics and Business, University of Zagreb, Faculty of Economics and Business, 1(1): 30-40. [Google Scholar]

- Demiröz S and Heupel T (2017). Digital Transformation and its radical changes for external management accounting: A consideration of small and medium-sized enterprises. In the Proceedings of the 7th FDIBA Conference, Sofia, Bulgaria: 57-59. [Google Scholar]

- El-Manaseer SA, Al-Kayid JH, Al Khawatreh AM, and Shamim M (2023). The impact of digital transformation on combating tax evasion (electronic billing system as a model). In: Alareeni BAM and Elgedawy I (Eds.), Artificial intelligence (AI) and finance: 679-690. Springer Nature Switzerland, Cham, Switzerland. https://doi.org/10.1007/978-3-031-39158-3_63 [Google Scholar]

- Fernandez D and Aman A (2018). Impacts of robotic process automation on global accounting services. Asian Journal of Accounting and Governance, 9: 123–131. https://doi.org/10.17576/AJAG-2018-09-11 [Google Scholar]

- Fotoh LE and Lorentzon JI (2023). Audit digitalization and its consequences on the audit expectation gap: A critical perspective. Accounting Horizons, 37(1): 43-69. https://doi.org/10.2308/HORIZONS-2021-027 [Google Scholar]

- Gepp A, Linnenluecke MK, O'Neill TJ, and Smith T (2018). Big data techniques in auditing research and practice: Current trends and future opportunities. Journal of Accounting Literature, 40(1): 102-115. https://doi.org/10.1016/j.acclit.2017.05.003 [Google Scholar]

- Gulin D, Hladika M, and Valenta I (2019). Digitalization and the challenges for the accounting profession. ENTRENOVA- Enterprise Research Innovation, 5(1): 428-437. https://doi.org/10.2139/ssrn.3492237 [Google Scholar]

- Hadi AH, Ali MN, Al-shiblawi GAK, Flayyih HH, and Talab HR (2023). The effects of information technology adoption on the financial reporting: Moderating role of audit risk. International Journal of Economics and Finance Studies, 15(1): 47-63. [Google Scholar]

- Iansiti M and Lakhani KR (2017). The truth about blockchain. Harvard Business Review, 95(1): 118-127. [Google Scholar]

- Jans M, Aysolmaz B, Corten M, Joshi A, and van Peteghem M (2023). Digitalization in accounting–Warmly embraced or coldly ignored? Accounting, Auditing and Accountability Journal, 36(9): 61-85. https://doi.org/10.1108/AAAJ-11-2020-4998 [Google Scholar]

- Kaya CT, Türkyılmaz M, and Birol B (2019). Impact of RPA technologies on accounting systems. Muhasebe ve Finansman Dergisi, (82): 235-250. https://doi.org/10.25095/mufad.536083 [Google Scholar]

- Khasawneh M and Alqurran T (2019). Factors influencing consumers' intention to adopt and use mobile banking applications in Jordanian Islamic banks. European Journal of Scientific Research, 152(4): 384-393. [Google Scholar]

- Knudsen ES, Lien LB, Timmermans B, Belik I, and Pandey S (2021). Stability in turbulent times? The effect of digitalization on the sustainability of competitive advantage. Journal of Business Research, 128: 360-369. https://doi.org/10.1016/j.jbusres.2021.02.008 [Google Scholar]

- Kokina J and Blanchette S (2019). Early evidence of digital labor in accounting: Innovation with robotic process automation. International Journal of Accounting Information Systems, 35: 100431. https://doi.org/10.1016/j.accinf.2019.100431 [Google Scholar]

- Kruskopf S, Lobbas C, Meinander H, Söderling K, Martikainen M, and Lehner O (2020). Digital accounting and the human factor: Theory and practice. ACRN Journal of Finance and Risk Perspectives, 9(1): 78-89. https://doi.org/10.35944/jofrp.2020.9.1.006 [Google Scholar]

- Lazarova V (2019). Digitalization and digital transformation in accounting. Ikonomiceski i Sotsialni Alternativi, (2): 97-106. [Google Scholar]

- Liguori M and Steccolini I (2011). Accounting change: Explaining the outcomes, interpreting the process. Accounting, Auditing and Accountability Journal, 25(1): 27-70. https://doi.org/10.1108/09513571211191743 [Google Scholar]

- Mardawi Z, Seguí-Mas E, and Tormo-Carbó G (2023). Wave after wave: Unboxing 40 years of auditing ethics research. Meditari Accountancy Research, 31(6): 1886-1918. https://doi.org/10.1108/MEDAR-05-2022-1698 [Google Scholar]

- Minkkinen M, Laine J, and Mäntymäki M (2022). Continuous auditing of artificial intelligence: A conceptualization and assessment of tools and frameworks. Digital Society, 1: 21. https://doi.org/10.1007/s44206-022-00022-2 [Google Scholar]

- Mohammad SJ, Hamad AK, Borgi H, Thu PA, Sial MS, and Alhadidi AA (2020). How artificial intelligence changes the future of accounting industry. International Journal of Economics and Business Administration, 8(3): 478-488. https://doi.org/10.35808/ijeba/538 [Google Scholar]

- Msweli NT and Mawela T (2021). Financial inclusion of the elderly: Exploring the role of mobile banking adoption. Acta Informatica Pragensia, 10(1): 1-21. https://doi.org/10.18267/j.aip.143 [Google Scholar]

- Othman OHOAL and Dweikat MFS (2021). The impact of digital transformation risk management on the credibility of accounting information in Jordanian commercial banks. Psychology and Education Journal, 58(2): 3893-3904. [Google Scholar]

- Peppard J and Ward J (2004). Beyond strategic information systems: Towards an IS capability. The Journal of Strategic Information Systems, 13(2): 167-194. https://doi.org/10.1016/j.jsis.2004.02.002 [Google Scholar]

- Phornlaphatrachakorn K and Na Kalasindhu K (2021). Digital accounting, financial reporting quality and digital transformation: Evidence from Thai listed firms. The Journal of Asian Finance, Economics and Business, 8(8): 409-419. [Google Scholar]

- Potryvaieva N, Kozachenko L, Nedbaylo I, and Nesterchuk I (2022). Digitization of accounting in the management of business processes of enterprises of the agro-industrial complex. Ukrainian Black Sea Region Agrarian Science, 26(1): 79-88. https://doi.org/10.56407/2313-092X/2022-26(1)-8 [Google Scholar]

- Rehm SV (2017). Accounting information systems and how to prepare for digital transformation. In: Quinn M and Strauss E (Eds.), The Routledge companion to accounting information systems: 69-80. Routledge, Oxfordshire, UK. https://doi.org/10.4324/9781315647210-6 [Google Scholar]

- Rejman Petrovic D, Krstic A, Nedeljković I, and Mimovic P (2024). Efficiency of digital business transformation in the Republic of Serbia. VINE Journal of Information and Knowledge Management Systems, 54(4): 725-744. https://doi.org/10.1108/VJIKMS-12-2021-0292 [Google Scholar]

- Saed KAM (2020). Assessment of the impact made by the digital transformation of the accounting system on the decision-making system of the enterprise. Management, 5(6): 29-35. [Google Scholar]

- Tawiah V and Borgi H (2022). Impact of XBRL adoption on financial reporting quality: A global evidence. Accounting Research Journal, 35(6): 815-833. https://doi.org/10.1108/ARJ-01-2022-0002 [Google Scholar]

- Thipwiwatpotjana S (2021). Digital transformation of accounting firms: The perspective of employees from quality accounting firms in Thailand. Human Behavior, Development and Society, 22(1): 53-62. [Google Scholar]

- Tian Z, Qiu L, and Wang L (2024). Drivers and influencers of blockchain and cloud-based business sustainability accounting in China: Enhancing practices and promoting adoption. PLOS ONE, 19(1): e0295802. https://doi.org/10.1371/journal.pone.0295802 [Google Scholar] PMid:38166081 PMCid:PMC10760918

- Tuan NM, Hung NQ, and Hang NT (2021). Digital transformation in the business: A solution for developing cash accounting information systems and digitizing documents. Science and Technology Development Journal, 24(2): 1975-1987. https://doi.org/10.32508/stdj.v24i2.2526 [Google Scholar]

- Vasarhelyi MA, Kogan A, and Tuttle BM (2015). Big data in accounting: An overview. Accounting Horizons, 29(2): 381-396. https://doi.org/10.2308/acch-51071 [Google Scholar]

- Wang D and Shao X (2024). Research on the impact of digital transformation on the production efficiency of manufacturing enterprises: Institution-based analysis of the threshold effect. International Review of Economics and Finance, 91: 883-897. https://doi.org/10.1016/j.iref.2024.01.046 [Google Scholar]