International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 11, Issue 11 (November 2024), Pages: 187-197

----------------------------------------------

Original Research Paper

Factors influencing trade union fund collection to ensure social security for workers: Perspectives from Vietnamese trade union finance officers

Author(s):

Affiliation(s):

Faculty of Accounting, Trade Union University, Hanoi, Vietnam

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0003-3647-8041

Corresponding author's ORCID profile: https://orcid.org/0000-0003-3647-8041

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2024.11.020

Abstract

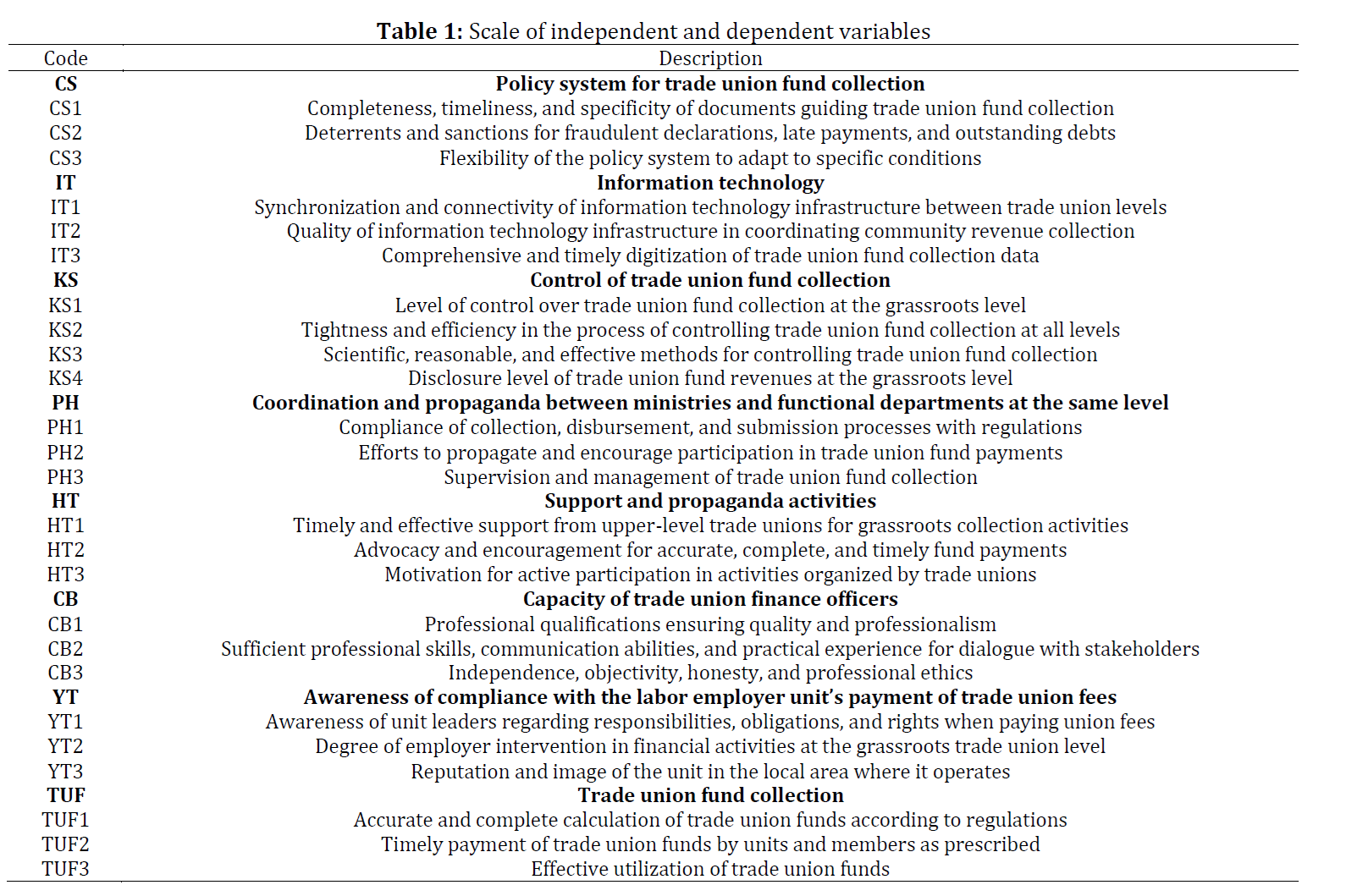

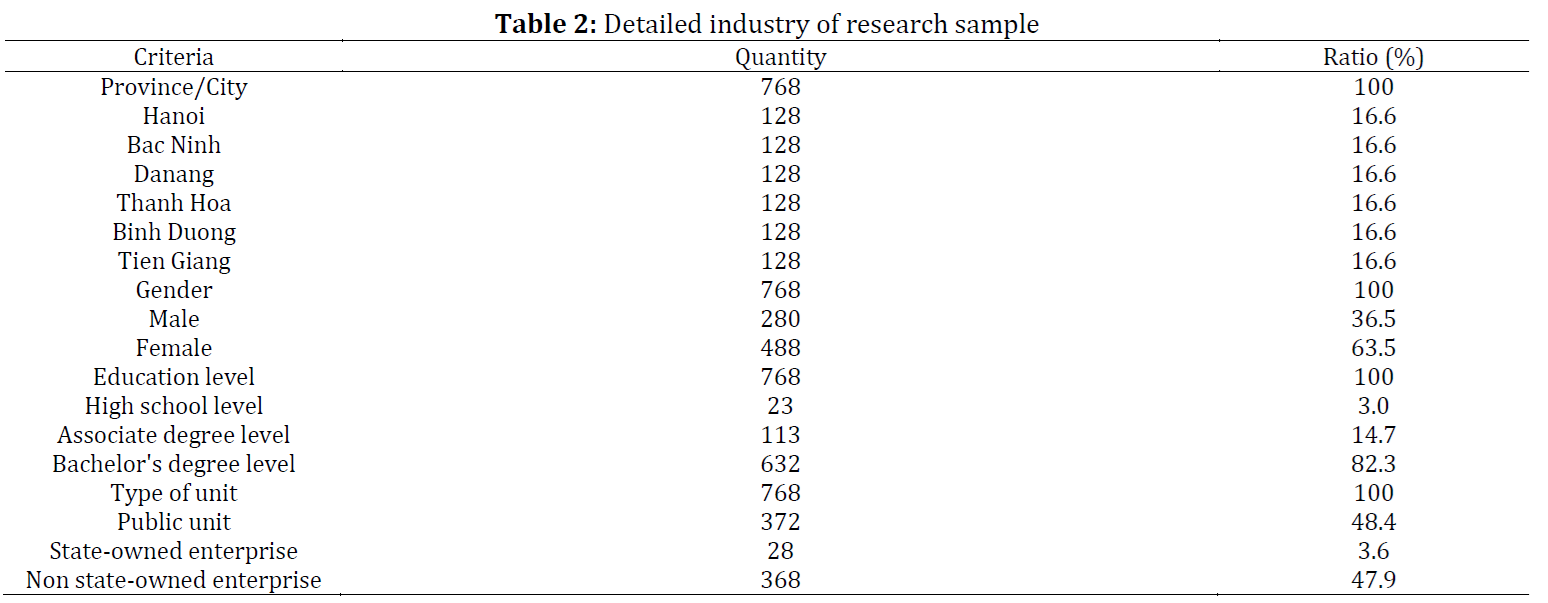

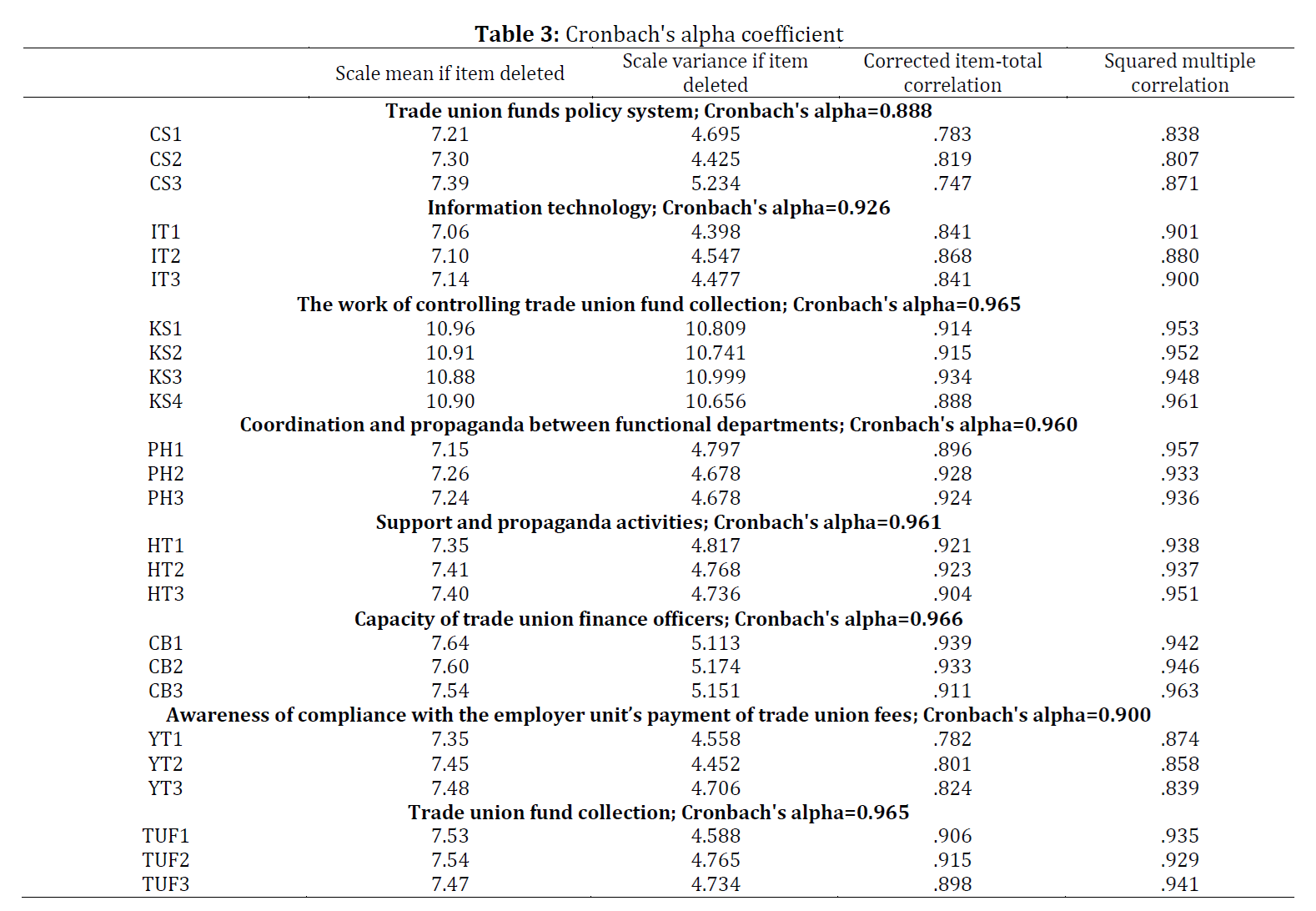

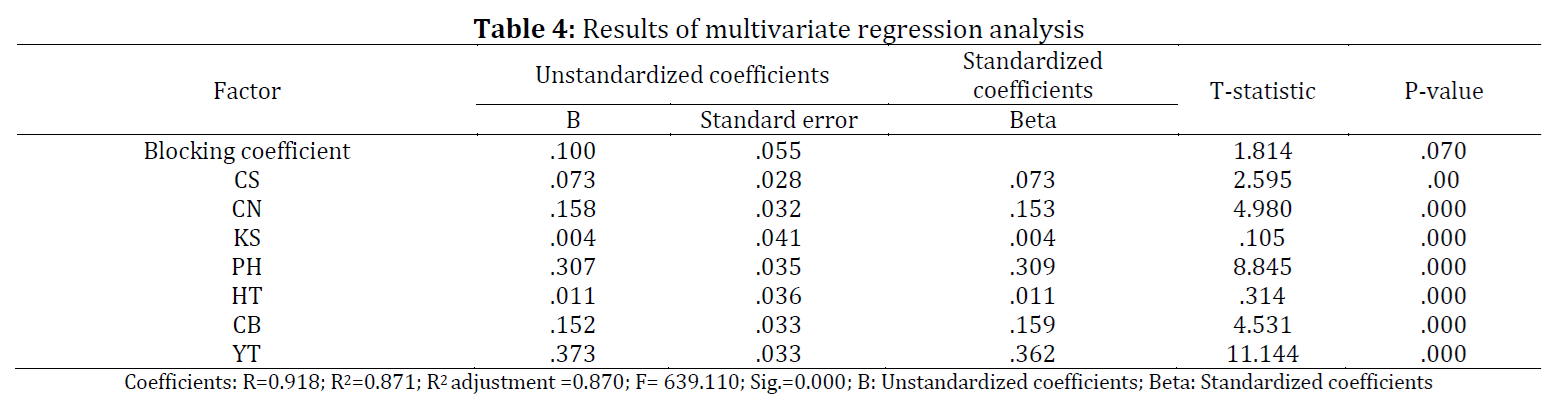

The study aims to identify factors affecting the collection of trade union funds to enhance social security for employees. Data for the research were gathered through a survey of 768 trade union finance officers. The methods used included descriptive statistics, Cronbach's Alpha testing, and multivariate regression analysis. The findings reveal seven key factors that positively influence trade union fund collection: the financial policy system of the trade union, information technology, fund collection controls, coordination with ministries and relevant departments, the skills and capacity of trade union finance officers, support and awareness campaigns, and employers' compliance with union fee payments. Based on these results, the authors suggest recommendations to strengthen fund collection, ensuring sufficient financial resources for trade unions to effectively fulfill their roles and responsibilities.

© 2024 The Authors. Published by IASE.

This is an

Keywords

Trade union funds, Social security, Financial policies, Information technology, Employer compliance

Article history

Received 21 July 2024, Received in revised form 21 October 2024, Accepted 7 November 2024

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Chau HTM, Anh VTK, and Chau TTV (2024). Factors influencing trade union fund collection to ensure social security for workers: Perspectives from Vietnamese trade union finance officers. International Journal of Advanced and Applied Sciences, 11(11): 187-197

Figures

No Figure

Tables

Table 1 Table 2 Table 3 Table 4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (29)

- Al-Ghazali BM and Sohail MS (2021). The impact of employees’ perceptions of CSR on career satisfaction: Evidence from Saudi Arabia. Sustainability, 13(9): 5235. https://doi.org/10.3390/su13095235 [Google Scholar]

- Ball A and Craig R (2010). Using neo-institutionalism to advance social and environmental accounting. Critical Perspectives on Accounting, 21: 283-293. https://doi.org/10.1016/j.cpa.2009.11.006 [Google Scholar]

- Berthod O (2016). Institutional theory of organizations. In: Farazmand A (Ed.), Global encyclopedia of public administration, public policy, and governance: 1–5. Springer, Berlin, Germany. https://doi.org/10.1007/978-3-319-31816-5_63-1 [Google Scholar]

- Brown DL, Dillard JF, and Marshall RS (2005). Strategically informed, environmentally conscious information requirements for accounting information systems. Journal of Information Systems, 19: 79-103. https://doi.org/10.2308/jis.2005.19.2.79 [Google Scholar]

- Chenhall RH (2003). Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Accounting Organizations and Society, 28: 127-168. https://doi.org/10.1016/S0361-3682(01)00027-7 [Google Scholar]

- Choi JS, Kwak YM, and Choe C (2010). Corporate social responsibility and corporate financial performance: Evidence from Korea. Australian Journal of Management, 35: 291-311. https://doi.org/10.1177/0312896210384681 [Google Scholar]

- Cristobal E, Flavian C, and Guinaliu M (2007). Perceived e‐service quality (PeSQ) measurement validation and effects on consumer satisfaction and web site loyalty. Managing Service Quality: An International Journal, 17: 317-340. https://doi.org/10.1108/09604520710744326 [Google Scholar]

- Deegan C (2014). An overview of legitimacy theory as applied within the social and environmental accounting literature. In: Laine M and Tregidga H (Eds.), Sustainability accounting and accountability: 248-272. 2nd Edition, Routledge, London, UK. [Google Scholar]

- Delmas M and Toffel MW (2004). Stakeholders and environmental management practices: An institutional framework. Business Strategy and the Environment, 13: 209-222. https://doi.org/10.1002/bse.409 [Google Scholar]

- DiMaggio PJ and Powell WW (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48: 147-160. https://doi.org/10.2307/2095101 [Google Scholar]

- Fernando S and Lawrence S (2014). A theoretical framework for CSR practices: Integrating legitimacy theory, stakeholder theory and institutional theory. Journal of Theoretical Accounting Research, 10: 149-178. [Google Scholar]

- Freeman RE (2004). A stakeholder theory of the modern corporation. In: Beauchamp TL, Bowie NE, and Arnold DG (Eds.), Ethical theory and business: 56-65. Prentice Hall, Upper Saddle River, USA. [Google Scholar]

- Gray R (1992). Accounting and environmentalism: An exploration of the challenge of gently accounting for accountability, transparency and sustainability. Accounting Organizations and Society, 17: 399-425. https://doi.org/10.1016/0361-3682(92)90038-T [Google Scholar]

- Hair JF, Black WC, Babin BJ, and Anderson RE (2010). Multivariate data analysis: A global perspective. Prentice Hall, Upper Saddle River, USA. [Google Scholar]

- Hansen VJ (2020). The unintended consequences of internal controls reporting on tax decision making. The Journal of the American Taxation Association, 42(1): 83-102. https://doi.org/10.2308/atax-52514 [Google Scholar]

- Hodder A and Edwards P (2015). The essence of trade unions: understanding identity, ideology and purpose. Work, Employment and Society, 29(5): 843-854. https://doi.org/10.1177/0950017014568142 [Google Scholar]

- Hoffman AJ (2001). Linking organizational and field-level analyses: The diffusion of corporate environmental practice. Organization and Environment, 14: 133-156. https://doi.org/10.1177/1086026601142001 [Google Scholar]

- Hossen MM, Chan TJ, and Hasan NA (2020). Mediating role of job satisfaction on internal corporate social responsibility practices and employee engagement in higher education sector. Contemporary Management Research, 16(3): 207-227. https://doi.org/10.7903/cmr.20334 [Google Scholar]

- Huang YY (2022). The management and use of trade union funds in public institutions. Proceedings of Business and Economic Studies, 5(2): 28-35. https://doi.org/10.26689/pbes.v5i2.3816 [Google Scholar]

- Jarvis R and Rigby M (2012). The provision of human resources and employment advice to small and medium-sized enterprises: The role of small and medium-sized practices of accountants. International Small Business Journal, 30(8): 944-956. https://doi.org/10.1177/0266242612445403 [Google Scholar]

- Kunz J (2020). Corporate social responsibility and employees motivation—Broadening the perspective. Schmalenbach Business Review, 72: 159-191. https://doi.org/10.1007/s41464-020-00089-9 [Google Scholar]

- Niap D (2006). Environmental management accounting for an Australian cogeneration company. Ph.D. Dissertation, RMIT University, Melbourne, Australia. [Google Scholar]

- Scapens RW and Jazayeri M (2003). ERP systems and management accounting change: Opportunities or impacts? A research note. European Accounting Review, 12: 201-233. https://doi.org/10.1080/0963818031000087907 [Google Scholar]

- Snell D and Gekara V (2020). Unions and corporate social responsibility in a liberal market context: The case of Ford’s shutdown in Australia. Journal of Industrial Relations, 62(5): 713-734. https://doi.org/10.1177/0022185619896383 [Google Scholar]

- Viere T, von Enden J, and Schaltegger S (2011). Life cycle and supply chain information in environmental management accounting: A coffee case study. In: Burritt R, Schaltegger S, Bennett M, Pohjola T, and Csutora M (Eds.), Environmental management accounting and supply chain management: 23-40. Springer, Dordrecht, Netherlands. https://doi.org/10.1007/978-94-007-1390-1_2 [Google Scholar]

- Wang J and Coffey BS (1992). Board composition and corporate philanthropy. Journal of Business Ethics, 11: 771-778. https://doi.org/10.1007/BF00872309 [Google Scholar]

- Warren JD, Moffitt KC, and Byrnes P (2015). How big data will change accounting. Accounting Horizons, 29: 397-407. https://doi.org/10.2308/acch-51069 [Google Scholar]

- Wolters T, Kokubu K, and Kurasaka T (2002). Corporate environmental accounting: A Japanese perspective. In: Bennett M and Bouma JJ (Eds.), Environmental management accounting: Informational and institutional developments: 161-173. Springer, Dordrecht, Netherlands. https://doi.org/10.1007/0-306-48022-0_12 [Google Scholar]

- Wong LT and Fryxell GE (2004). Stakeholder influences on environmental management practices: A study of fleet operations in Hong Kong (SAR) China. Transportation Journal, 43: 22-35. [Google Scholar]