International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 10, Issue 8 (August 2023), Pages: 112-120

----------------------------------------------

Original Research Paper

Spillover effects of internal audit effectiveness among commercial banks

Author(s):

Hanh Hoang Thanh *, Dung Ngo Tien

Affiliation(s):

Accounting Auditing Department, Academy of Policy and Development, Hanoi, Vietnam

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-7034-0105

Corresponding author's ORCID profile: https://orcid.org/0000-0001-7034-0105

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2023.08.013

Abstract:

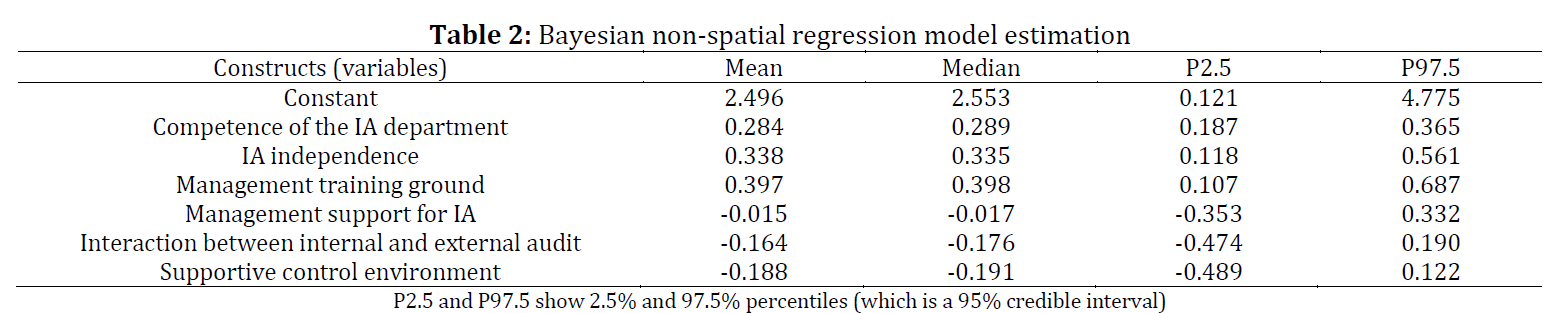

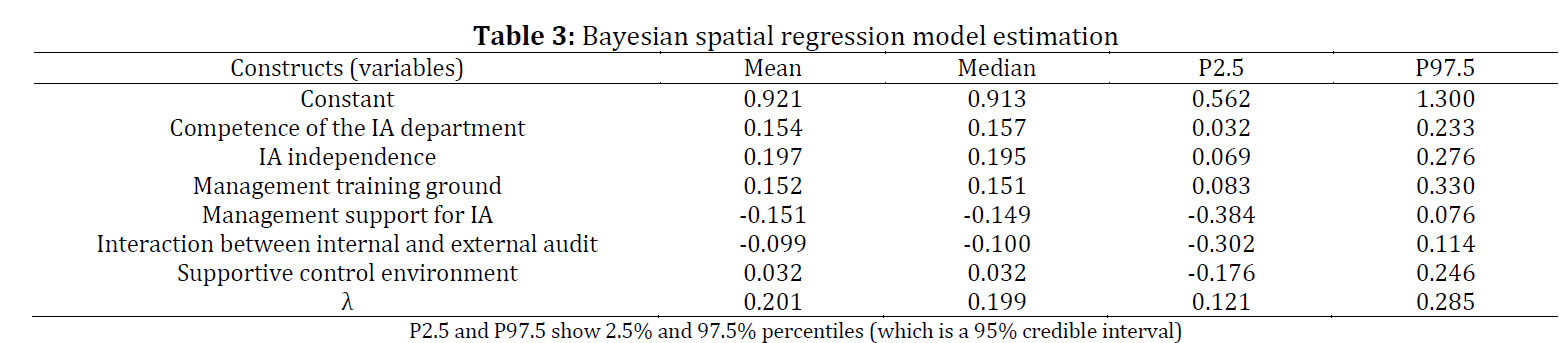

This study explores the multifaceted landscape of factors influencing the effectiveness of internal audit within the context of Vietnamese commercial banks. While a plethora of literature exists on the determinants of internal audit effectiveness, an unexplored dimension is the examination of spillover effects amongst companies operating within the same industry. This research addresses this gap by investigating not only the factors that impact the effectiveness of internal audit in Vietnamese commercial banks but also the inter-bank spillover effects of such effectiveness. Utilizing data obtained from 24 commercial banks listed on the Vietnam Stock Exchange and Vietnam Upcom (The Unlisted Public Company Market), we employ a Bayesian spatial regression model (a robust analytical tool) to conduct comprehensive analyses of the interrelationships and co-movements of internal audit effectiveness across these banks. Our findings offer empirical support for the positive effects of key determinants, namely, the "Competence of the IA Department," "IA Independence," and "Management Training Ground," on the effectiveness of internal audit in Vietnamese commercial banks. Notably, our results also validate the significant positive inter-bank spillover effect of internal audit effectiveness. This underscores the importance for banks to collectively prioritize measures aimed at enhancing the quality of internal audit, including the establishment of a joint internal audit association and the organization of collaborative training initiatives for internal audit personnel.

© 2023 The Authors. Published by IASE.

This is an

Keywords: Internal audit, Effectiveness, Commercial banks, Spillover effects

Article History: Received 16 January 2023, Received in revised form 11 June 2023, Accepted 10 July 2023

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Thanh HH and Tien DN (2023). Spillover effects of internal audit effectiveness among commercial banks. International Journal of Advanced and Applied Sciences, 10(8): 112-120

Figures

{kind=link}

{kind=link}

Tables

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (26)

- Abdo H (2016). Accounting for extractive industries: Has IFRS 6 harmonised accounting practices by extractive industries? Australian Accounting Review, 26(4): 346-359. https://doi.org/10.1111/auar.12106 [Google Scholar]

- Al-Twaijry AA, Brierley JA, and Gwilliam DR (2003). The development of internal audit in Saudi Arabia: An institutional theory perspective. Critical Perspectives on Accounting, 14(5): 507-531. https://doi.org/10.1016/S1045-2354(02)00158-2 [Google Scholar]

- Alzeban A and Gwilliam D (2014). Factors affecting the internal audit effectiveness: A survey of the Saudi public sector. Journal of International Accounting, Auditing and Taxation, 23(2): 74-86. https://doi.org/10.1016/j.intaccaudtax.2014.06.001 [Google Scholar]

- Arena M and Azzone G (2009). Identifying organizational drivers of internal audit effectiveness. International Journal of Auditing, 13(1): 43-60. https://doi.org/10.1111/j.1099-1123.2008.00392.x [Google Scholar]

- Baheri J, Sudarmanto, and Wekke IS (2017). The effect of management support to effectiveness of internal audit for public universities. Journal of Engineering and Applied Sciences, 12(7): 1696-1700. [Google Scholar]

- Barišić I and Tušek B (2016). The importance of the supportive control environment for internal audit effectiveness–The case of Croatian companies. Economic Research-Ekonomska Istraživanja, 29(1): 1021-1037. https://doi.org/10.1080/1331677X.2016.1211954 [Google Scholar]

- Beckmerhagen IA, Berg HP, Karapetrovic SV, and Willborn WO (2004). On the effectiveness of quality management system audits. The TQM Magazine, 16(1): 14-25. https://doi.org/10.1108/09544780410511443 [Google Scholar]

- Cohen A and Sayag G (2010). The effectiveness of internal auditing: An empirical examination of its determinants in Israeli organisations. Australian Accounting Review, 20(3): 296-307. https://doi.org/10.1111/j.1835-2561.2010.00092.x [Google Scholar]

- Dejnaronk J, Little HT, Mujtaba BG, and McClelland R (2016). Factors influencing the effectiveness of the internal audit function in Thailand. Journal of Business and Policy Research, 11(2): 80-93. https://doi.org/10.21102/jbpr.2016.12.112.05 [Google Scholar]

- Dellai H and Omri MAB (2016). Factors affecting the internal audit effectiveness in Tunisian organizations. Research Journal of Finance and Accounting, 7(16): 208-211. [Google Scholar]

- Dittenhofer M (2001). Internal auditing effectiveness: An expansion of present methods. Managerial Auditing Journal, 16(8): 443–450. https://doi.org/10.1108/EUM0000000006064 [Google Scholar]

- D'Onza G, Selim GM, Melville R, and Allegrini M (2015). A study on Internal auditor perceptions of the function ability to add value. International Journal of Auditing, 19(3): 182-194. https://doi.org/10.1111/ijau.12048 [Google Scholar]

- Fallah MH and Ibrahim S (2004). Knowledge spillover and innovation in technological clusters. In Proceedings, IAMOT 2004 Conference, Washington, USA: 1-16. [Google Scholar]

- Kelejian HH and Prucha IR (1998). A generalized spatial two-stage least squares procedure for estimating a spatial autoregressive model with autoregressive disturbances. The Journal of Real Estate Finance and Economics, 17(1): 99-121. [Google Scholar]

- Kelejian HH and Prucha IR (1999). A generalized moments estimator for the autoregressive parameter in a spatial model. International Economic Review, 40(2): 509-533. https://doi.org/10.1111/1468-2354.00027 [Google Scholar]

- Kuschnig N (2022). Bayesian spatial econometrics: A software architecture. Journal of Spatial Econometrics, 3: 6. https://doi.org/10.1007/s43071-022-00023-w [Google Scholar]

- Lee LF (2004). Asymptotic distributions of quasi‐maximum likelihood estimators for spatial autoregressive models. Econometrica, 72(6): 1899-1925. https://doi.org/10.1111/j.1468-0262.2004.00558.x [Google Scholar]

- Lenz R and Hahn U (2015). A synthesis of empirical internal audit effectiveness literature pointing to new research opportunities. Managerial Auditing Journal, 30(1): 5-33. https://doi.org/10.1108/MAJ-08-2014-1072 [Google Scholar]

- LeSage JP and Pace RK (2009). Introduction to spatial econometrics. Chapman and Hall/CRC, London, UK. https://doi.org/10.1201/9781420064254 [Google Scholar]

- Mihret DG and Yismaw AW (2007). Internal audit effectiveness: An Ethiopian public sector case study. Managerial Auditing Journal, 22(5): 470-484. https://doi.org/10.1108/02686900710750757 [Google Scholar]

- Paape L (2007). Corporate governance: The impact on the role, position, and scope of services of the internal audit function. Erasmus Research Institute of Management, Erasmus University Rotterdam, Rotterdam, Netherlands. [Google Scholar]

- Ross J, Ziebart D, and Meder A (2019). A new measure of firm-group accounting closeness. Review of Quantitative Finance and Accounting, 52(4): 1137-1161. https://doi.org/10.1007/s11156-018-0739-0 [Google Scholar]

- Shu F, Li Q, Wang Q, and Zhang H (2010). Measurement and analysis of process audit: A case study. In the International Conference on New Modeling Concepts for Today’s Software Processes: Software Process, Springer, Paderborn, Germany: 285-296. https://doi.org/10.1007/978-3-642-14347-2_25 [Google Scholar]

- Turetken O, Jethefer S, and Ozkan B (2020). Internal audit effectiveness: Operationalization and influencing factors. Managerial Auditing Journal, 35(2): 238-271. https://doi.org/10.1108/MAJ-08-2018-1980 [Google Scholar]

- Yee CS, Sujan A, James K, and Leung JK (2008). Perceptions of Singaporean internal audit customers regarding the role and effectiveness of internal audit. Asian Journal of Business and Accounting, 1(2): 147-174. [Google Scholar]

- Zollo M and Reuer JJ (2010). Experience spillovers across corporate development activities. Organization Science, 21(6): 1195-1212. https://doi.org/10.1287/orsc.1090.0474 [Google Scholar]