International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 10, Issue 8 (August 2023), Pages: 71-77

----------------------------------------------

Original Research Paper

The impact of digital evolution and FinTech on banking performance: A cross-country analysis

Author(s):

Mohammed Ibrahim Alattass *

Affiliation(s):

Department of Management Information System, College of Business, University of Jeddah, Jeddah, Saudi Arabia

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0009-0002-6285-3183

Corresponding author's ORCID profile: https://orcid.org/0009-0002-6285-3183

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2023.08.008

Abstract:

Amidst the intricate web of economic dynamics, the significance of banking performance resonates deeply, serving as a linchpin for a nation's financial equilibrium and economic prosperity. The imperative of vigilantly tracking the trajectory of banks' performance emerges as this vigilance underpins the stabilization and fortification of credit institutions. In the contemporary milieu, a landscape characterized by rapid transformations and economic nuances, the digital sphere is propelling a substantial metamorphosis, thus catalyzing an imperative for the assimilation of financial technology (FinTech) within financial services, particularly within banking institutions. This empirical study embarks upon a discerning journey, harnessing a cross-country lens and a panel dataset encompassing five prominent nations spanning the years 2017 to 2019. The central inquiry pertains to the nuanced interplay between the digital milieu, FinTech deployment, and the fabric of banking performance. The empirical analysis reveals a noteworthy confluence: the utilization of digital platforms and FinTech solutions bears a detrimental association with the performance of banking entities categorized as high-performing. Moreover, this inquiry unveils a nexus between FinTech variables, including solidity, inflation informer, and total productivity factors, with an adverse impact on Banks' Performance. However, a silver lining emerges as the study highlights the augmentation of bank financial performance through the confluence of liquidity, Gross Domestic Product (GDP), and FinTech credit infusion. Emanating from these insights, the implications cascade expansively. For bank custodians and stakeholders, an enriched comprehension of the intricate interplay between FinTech and performance crystallizes, thereby fortifying the resilience of financial institutions against adversities through performance augmentation.

© 2023 The Authors. Published by IASE.

This is an

Keywords: Banking performance, Financial stability, Economic prosperity, Digital transformation, FinTech impact

Article History: Received 10 March 2023, Received in revised form 20 June 2023, Accepted 27 June 2023

Acknowledgment

This work was funded by the University of Jeddah, Jeddah, Saudi Arabia, under grant No. UJ-23-SHR-60. The authors, therefore, thank the University of Jeddah for its technical and financial support.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Alattass MI (2023). The impact of digital evolution and FinTech on banking performance: A cross-country analysis. International Journal of Advanced and Applied Sciences, 10(8): 71-77

Figures

No Figures

Tables

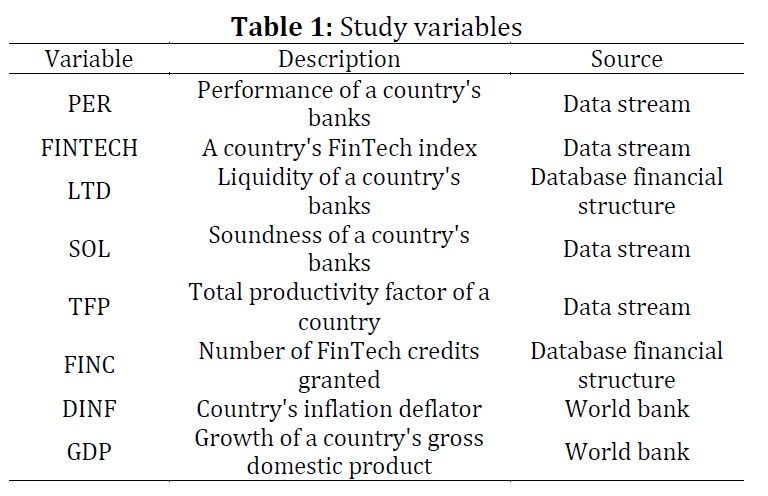

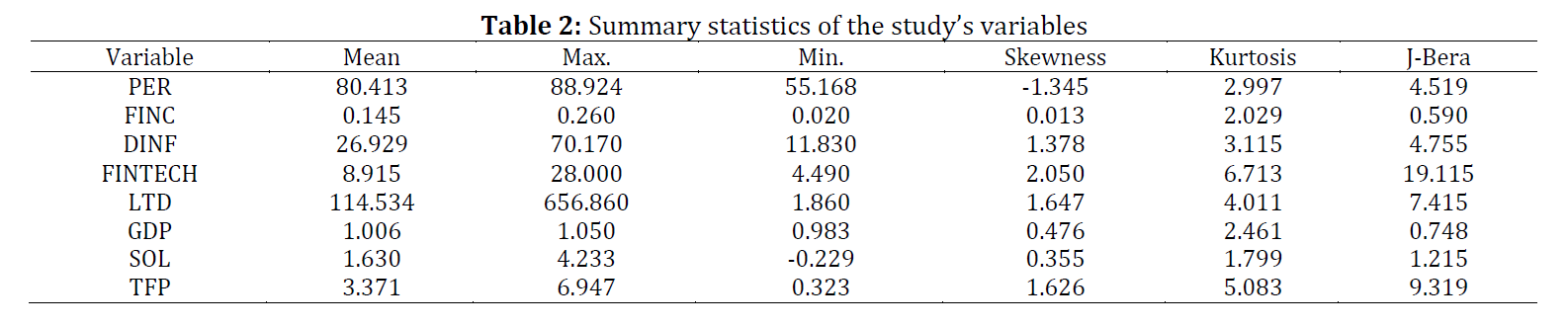

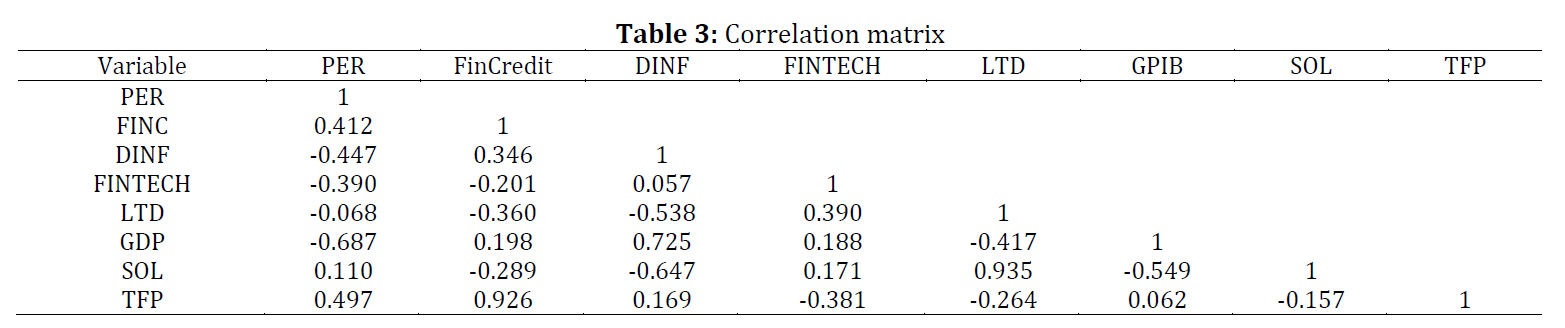

Table 1 Table 2 Table 3 Table 4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (26)

- Abreu M and Mendes V (2001). Commercial bank interest margins and profitability: Evidence for some EU countries. In the Pan-European Conference Jointly Organised by the IEFS-UK and University of Macedonia Economic and Social Sciences, Thessaloniki, Greece, 34(2): 17-20. [Google Scholar]

- An J, Hou W, and Liu X (2022). Historical determinants of FinTech development: Evidence from initial coin offerings. Finance Research Letters, 46: 102472. https://doi.org/10.1016/j.frl.2021.102472 [Google Scholar]

- Barroso M and Laborda J (2022). Digital transformation and the emergence of the FinTech sector: Systematic literature review. Digital Business, 2(2): 100028. https://doi.org/10.1016/j.digbus.2022.100028 [Google Scholar]

- Basdekis C, Christopoulos A, Katsampoxakis I, and Vlachou A (2022). FinTech’s rapid growth and its effect on the banking sector. Journal of Banking and Financial Technology, 6(2): 159-176. https://doi.org/10.1007/s42786-022-00045-w [Google Scholar] PMCid:PMC9707245

- Berger AN and Bouwman CH (2013). How does capital affect bank performance during financial crises? Journal of Financial Economics, 109(1): 146-176. https://doi.org/10.1016/j.jfineco.2013.02.008 [Google Scholar]

- Cull R, Peria MMSM, and Verrier J (2017). Bank ownership: Trends and implications. International Monetary Fund, Washington, USA. https://doi.org/10.5089/9781475588125.001 [Google Scholar]

- Demir A, Pesqué-Cela V, Altunbas Y, and Murinde V (2022). FinTech, financial inclusion and income inequality: A quantile regression approach. The European Journal of Finance, 28(1): 86-107. https://doi.org/10.1080/1351847X.2020.1772335 [Google Scholar]

- Dietrich A and Wanzenried G (2014). The determinants of commercial banking profitability in low-, middle-, and high-income countries. The Quarterly Review of Economics and Finance, 54(3): 337-354. https://doi.org/10.1016/j.qref.2014.03.001 [Google Scholar]

- Gomber P, Kauffman RJ, Parker C, and Weber BW (2018). On the FinTech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. Journal of Management Information Systems, 35(1): 220-265. https://doi.org/10.1080/07421222.2018.1440766 [Google Scholar]

- Gonzalez L and Loureiro YK (2014). When can a photo increase credit? The impact of lender and borrower profiles on online peer-to-peer loans. Journal of Behavioral and Experimental Finance, 2: 44-58. https://doi.org/10.1016/j.jbef.2014.04.002 [Google Scholar]

- Hsieh SH and Lee CT (2021). Hey Alexa: Examining the effect of perceived socialness in usage intentions of AI assistant-enabled smart speaker. Journal of Research in Interactive Marketing, 15(2): 267-294. https://doi.org/10.1108/JRIM-11-2019-0179 [Google Scholar]

- Iannotta G, Nocera G, and Sironi A (2007). Ownership structure, risk and performance in the European banking industry. Journal of Banking and Finance, 31(7): 2127-2149. https://doi.org/10.1016/j.jbankfin.2006.07.013 [Google Scholar]

- Kijek T and Matras-Bolibok A (2019). The relationship between TFP and innovation performance: Evidence from EU regions. Equilibrium. Quarterly Journal of Economics and Economic Policy, 14(4): 695-709. https://doi.org/10.24136/eq.2019.032 [Google Scholar]

- Köster H and Pelster M (2017). Financial penalties and bank performance. Journal of Banking and Finance, 79: 57-73. https://doi.org/10.1016/j.jbankfin.2017.02.009 [Google Scholar]

- Lee I and Shin YJ (2018). FinTech: Ecosystem, business models, investment decisions, and challenges. Business Horizons, 61(1): 35-46. https://doi.org/10.1016/j.bushor.2017.09.003 [Google Scholar]

- Matousek R and Xiang D (2021). The challenges and competitiveness of FinTech companies in Europe, UK and USA: An overview. In: Pompella M and Matousek R (Eds.), The Palgrave handbook of FinTech and Blockchain: 87-107. Palgrave Macmillan, Cham, Switzerland. https://doi.org/10.1007/978-3-030-66433-6_5 [Google Scholar]

- Mehran H and Thakor A (2011). Bank capital and value in the cross-section. The Review of Financial Studies, 24(4): 1019-1067. https://doi.org/10.1093/rfs/hhq022 [Google Scholar]

- Naceur SB (2003). The determinants of the Tunisian banking industry profitability: Panel evidence. Paper presented at the Economic Research Forum (ERF) 10th Annual Conference, Marrakesh, Morocco. Available online at: http://www.mafhoum.com/press6/174E11.pdf

- Naceur SB and Omran M (2011). The effects of bank regulations, competition, and financial reforms on banks' performance. Emerging Markets Review, 12(1): 1-20. https://doi.org/10.1016/j.ememar.2010.08.002 [Google Scholar]

- Noman AHM, Chowdhury MM, Chowdhury NJ, Kabir MJ, and Pervin S (2015). The effect of bank specific and macroeconomic determinants of banking profitability: A study on Bangladesh. International Journal of Business and Management, 10(6): 287-297. https://doi.org/10.5539/ijbm.v10n6p287 [Google Scholar]

- PeiZhi W and Ramzan M (2020). Do corporate governance structure and capital structure matter for the performance of the firms? An empirical testing with the contemplation of outliers. PLOS ONE, 15(2): e0229157. https://doi.org/10.1371/journal.pone.0229157 [Google Scholar] PMid:32106228 PMCid:PMC7046277

- Puschmann T, Hoffmann CH, and Khmarskyi V (2020). How green FinTech can alleviate the impact of climate change: The case of Switzerland. Sustainability, 12(24): 10691. https://doi.org/10.3390/su122410691 [Google Scholar]

- Scott JW and Arias JC (2011). Banking profitability determinants. Business Intelligence Journal, 4(2): 209-230. [Google Scholar]

- Talavera O, Yin S, and Zhang M (2018). Age diversity, directors' personal values, and bank performance. International Review of Financial Analysis, 55: 60-79. https://doi.org/10.1016/j.irfa.2017.10.007 [Google Scholar]

- Thai VH, Dinh VT, Nguyen VS, Nguyen MH, Nguyen CT, and Pham TLP (2021). The influence of earning management and surplus free cash flow on the banking sector performance. Polish Journal of Management Studies, 23(1): 403-417. https://doi.org/10.17512/pjms.2021.23.1.25 [Google Scholar]

- Varma P, Nijjer S, Sood K, Grima S, and Rupeika-Apoga R (2022). Thematic analysis of financial technology (FinTech) influence on the banking industry. Risks, 10(10): 186. https://doi.org/10.3390/risks10100186 [Google Scholar]