International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 10, Issue 11 (November 2023), Pages: 59-66

----------------------------------------------

Original Research Paper

The cascade effect: Are the U.S. economy and global stock markets vulnerable to the collapse of First Republic Bank?

Author(s):

Affiliation(s):

1Department of Business Administration, National College of Business Administration and Economics (NCBA&E) Lahore, Sub-Campus Multan, Pakistan

2Finance Department, College of Business and Administration (CBA), University of Business and Technology (UBT), Jeddah, Saudi Arabia

3Department of Economics, King Abdulaziz University, Jeddah, Saudi Arabia

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-6320-4295

Corresponding author's ORCID profile: https://orcid.org/0000-0001-6320-4295

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2023.11.008

Abstract

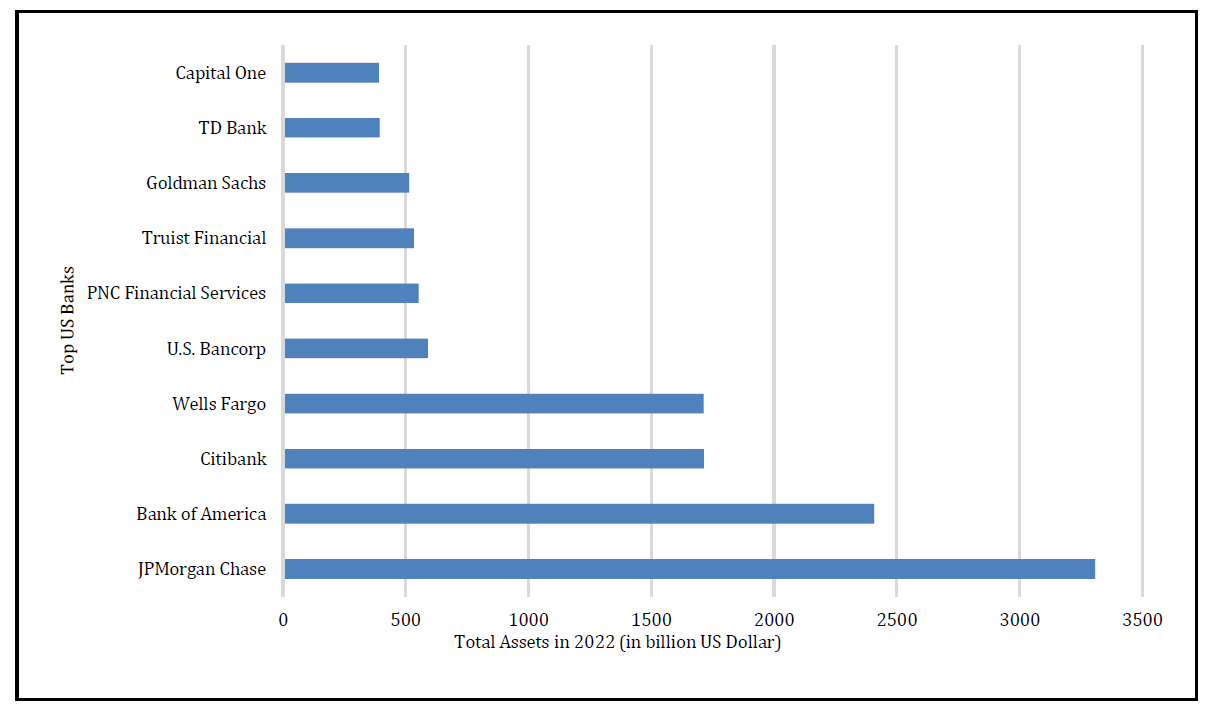

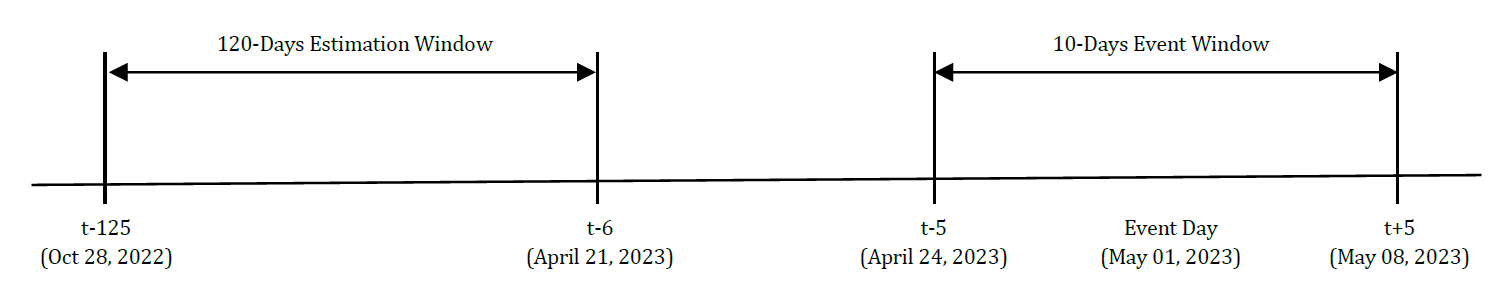

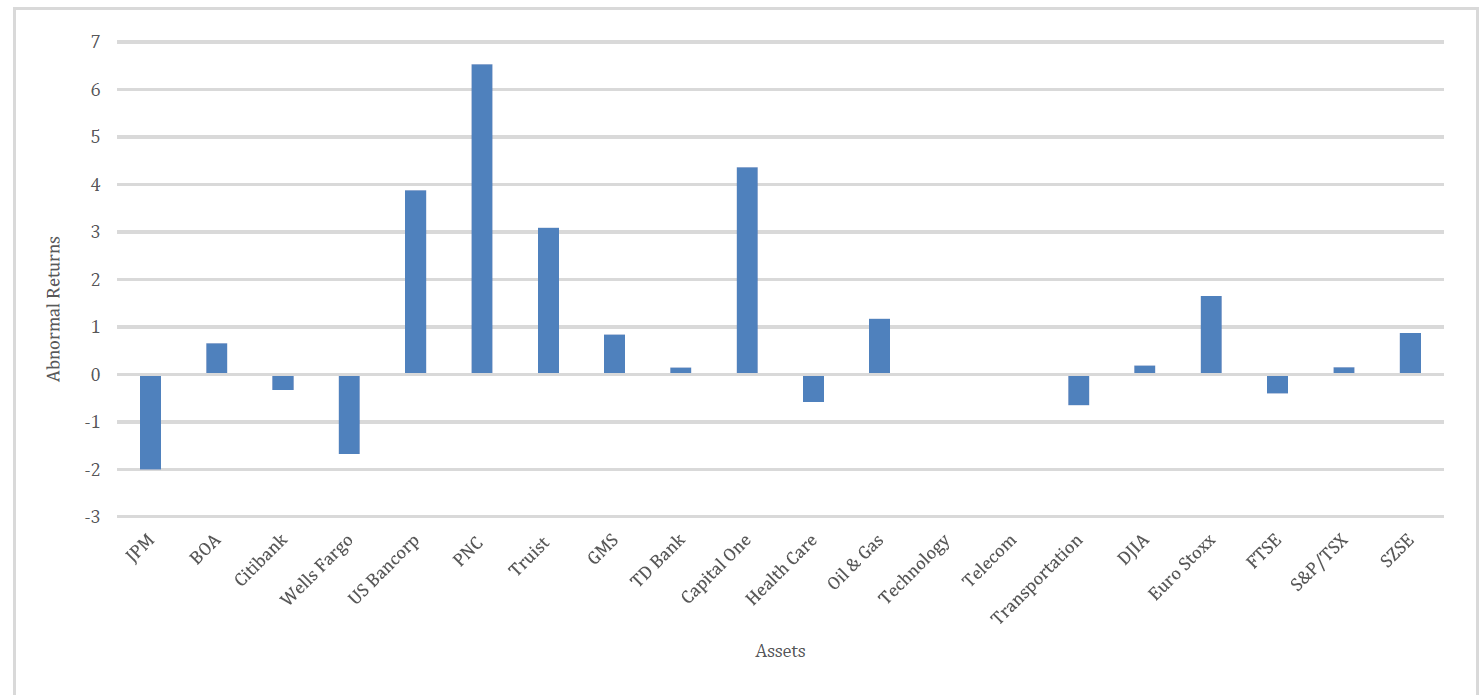

Following the collapse of Silicon Valley Bank and Signature Bank, First Republic Bank collapsed and is considered the second-largest bank failure in U.S. history. These bank runs can have a cascading or contagion effect on other large banks, and U.S. banking crises can flare up again. We examine the effect of the First Republic bank run on top U.S. banks, U.S. stock indices, and global stock indices using standard event study methodology. We report abnormal returns and cumulative abnormal returns for the event day (t = May 01, 2023) and the 10-day event window (t-5 to t+5), respectively, using data from the 120-day estimation window. The results indicate that on the event day, only JP Morgan Bank's returns were negative, while other banks acted as safe havens for investors. No significant change in returns on the event day is observed for U.S. sector indices (except for the healthcare sector) and global stock exchanges, except for the European and Chinese markets. During the event window, the occurrence of the event significantly affects bank returns after the event date, but no significant effect is found before the event date. Similarly, the healthcare and transportation sectors are more affected than other sectors, while the U.S. and Canadian stock markets seem to be more susceptible to the bank run. Overall, the results suggest that the U.S. government should take decisive initiatives to stop the ripple effect and protect the entire financial system.

© 2023 The Authors. Published by IASE.

This is an

Keywords

First Republic Bank, Bank collapse, Event study, Abnormal returns, U.S. financial crises, Efficient market

Article history

Received 7 July 2023, Received in revised form 19 October 2023, Accepted 23 October 2023

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Omar AB, Akeel H, and Khoj H (2023). The cascade effect: Are the U.S. economy and global stock markets vulnerable to the collapse of First Republic Bank? International Journal of Advanced and Applied Sciences, 10(11): 59-66

Figures

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (31)

- Abbassi W, Kumari V, and Pandey DK (2023). What makes firms vulnerable to the Russia–Ukraine crisis? The Journal of Risk Finance, 24(1): 24-39. https://doi.org/10.1108/JRF-05-2022-0108 [Google Scholar]

- Akyildirim E, Conlon T, Corbet S, and Goodell JW (2023). Understanding the FTX exchange collapse: A dynamic connectedness approach. Finance Research Letters, 53: 103643. https://doi.org/10.1016/j.frl.2023.103643 [Google Scholar]

- Alabbad A and Schertler A (2022). COVID-19 and bank performance in dual-banking countries: An empirical analysis. Journal of Business Economics, 92(9): 1511-1557. https://doi.org/10.1007/s11573-022-01093-w [Google Scholar] PMid:38013977 PMCid:PMC9069428

- Anwer Z, AZMI S, and Nobanee H (2023). On the impact of Silicon Valley Bank failure: Evidence on the reaction of major global asset classes. https://doi.org/10.2139/ssrn.4410761 [Google Scholar]

- Boubaker S, Goodell JW, Pandey DK, and Kumari V (2022). Heterogeneous impacts of wars on global equity markets: Evidence from the invasion of Ukraine. Finance Research Letters, 48: 102934. https://doi.org/10.1016/j.frl.2022.102934 [Google Scholar]

- Chortane SG and Pandey DK (2022). Does the Russia-Ukraine war lead to currency asymmetries? A US dollar tale. The Journal of Economic Asymmetries, 26: e00265. https://doi.org/10.1016/j.jeca.2022.e00265 [Google Scholar]

- Conlon T, Corbet S, and McGee RJ (2020). Are cryptocurrencies a safe haven for equity markets? An international perspective from the COVID-19 pandemic. Research in International Business and Finance, 54: 101248. https://doi.org/10.1016/j.ribaf.2020.101248 [Google Scholar] PMid:34170988 PMCid:PMC7271856

- Dai PF, Goodell JW, Huynh LDT, Liu Z, and Corbet S (2023). Understanding the transmission of crash risk between cryptocurrency and equity markets. Financial Review, 58(3): 539-573. https://doi.org/10.1111/fire.12340 [Google Scholar]

- Fama EF (1970). Efficient capital markets: A review of theory and empirical work. The Journal of Finance, 25(2): 383-417. https://doi.org/10.1111/j.1540-6261.1970.tb00518.x [Google Scholar]

- Fernandez-Perez A, Gilbert A, Indriawan I, and Nguyen NH (2021). COVID-19 pandemic and stock market response: A culture effect. Journal of Behavioral and Experimental Finance, 29: 100454. https://doi.org/10.1016/j.jbef.2020.100454 [Google Scholar] PMid:33520663 PMCid:PMC7831684

- Ganie IR, Wani TA, and Yadav MP (2022). Impact of COVID-19 outbreak on the stock market: An evidence from select economies. Business Perspectives and Research. https://doi.org/10.1177/22785337211073635 [Google Scholar]

- Gao X, Ren Y, and Umar M (2022). To what extent does COVID-19 drive stock market volatility? A comparison between the U.S. and China. Economic Research-Ekonomska Istraživanja, 35(1): 1686-1706. https://doi.org/10.1080/1331677X.2021.1906730 [Google Scholar]

- Heyden KJ and Heyden T (2021). Market reactions to the arrival and containment of COVID-19: An event study. Finance Research Letters, 38: 101745. https://doi.org/10.1016/j.frl.2020.101745 [Google Scholar] PMid:32895606 PMCid:PMC7467079

- Jokipii T and Monnin P (2013). The impact of banking sector stability on the real economy. Journal of International Money and Finance, 32: 1-16. https://doi.org/10.1016/j.jimonfin.2012.02.008 [Google Scholar]

- Khoj H and Akeel H (2020). Testing weak-form market efficiency: The case of Saudi Arabia. Asian Economic and Financial Review, 10(6): 644-653. https://doi.org/10.18488/journal.aefr.2020.106.644.653 [Google Scholar]

- Kumari V, Kumar G, and Pandey DK (2023). Are the European Union stock markets vulnerable to the Russia–Ukraine war? Journal of Behavioral and Experimental Finance, 37: 100793. https://doi.org/10.1016/j.jbef.2023.100793 [Google Scholar]

- MacKinlay AC (1997). Event studies in economics and finance. Journal of Economic Literature, 35(1): 13-39. [Google Scholar]

- Mazur M, Dang M, and Vega M (2021). COVID-19 and the March 2020 stock market crash. Evidence from S&P1500. Finance Research Letters, 38: 101690. https://doi.org/10.1016/j.frl.2020.101690 [Google Scholar] PMid:32837377 PMCid:PMC7343658

- Moshirian F and Wu Q (2012). Banking industry volatility and economic growth. Research in International Business and Finance, 26(3): 428-442. https://doi.org/10.1016/j.ribaf.2012.01.004 [Google Scholar]

- Omar AB, Ali A, Mouneer S, Kouser R, and Al-Faryan MAS (2022b). Is stock market development sensitive to macroeconomic indicators? A fresh evidence using ARDL bounds testing approach. PLOS ONE, 17(10): e0275708. https://doi.org/10.1371/journal.pone.0275708 [Google Scholar] PMid:36260625 PMCid:PMC9581411

- Omar AB, Huang S, Salameh AA, Khurram H, and Fareed M (2022a). Stock market forecasting using the random forest and deep neural network models before and during the COVID-19 period. Frontiers in Environmental Science, 10: 917047. https://doi.org/10.3389/fenvs.2022.917047 [Google Scholar]

- Pandey DK and Kumari V (2021). Event study on the reaction of the developed and emerging stock markets to the 2019-nCoV outbreak. International Review of Economics and Finance, 71: 467-483. https://doi.org/10.1016/j.iref.2020.09.014 [Google Scholar] PMCid:PMC7521415

- Pandey DK, Hassan MK, Kumari V, and Hasan R (2023). Repercussions of the Silicon Valley Bank collapse on global stock markets. Finance Research Letters, 55: 104013. https://doi.org/10.1016/j.frl.2023.104013 [Google Scholar]

- Sami M and Abdallah W (2021). How does the cryptocurrency market affect the stock market performance in the MENA region? Journal of Economic and Administrative Sciences, 37(4): 741-753. https://doi.org/10.1108/JEAS-07-2019-0078 [Google Scholar]

- Sun M and Zhang C (2022). Comprehensive analysis of global stock market reactions to the Russia-Ukraine war. Applied Economics Letters, 30(18): 2673-2680. https://doi.org/10.1080/13504851.2022.2103077 [Google Scholar]

- Yadav MP, Rao A, Abedin MZ, Tabassum S, and Lucey B (2023). The domino effect: Analyzing the impact of Silicon Valley Bank's fall on top equity indices around the world. Finance Research Letters, 55(Part B): 103952. https://doi.org/10.1016/j.frl.2023.103952 [Google Scholar]

- Yousaf I and Goodell JW (2023a). Reputational contagion and the fall of FTX: Examining the response of tokens to the delegitimization of FTT. Finance Research Letters, 54: 103704. https://doi.org/10.1016/j.frl.2023.103704 [Google Scholar]

- Yousaf I and Goodell JW (2023b). Responses of U.S. equity market sectors to the Silicon Valley Bank implosion. Finance Research Letters, 55(Part B): 103934. https://doi.org/10.1016/j.frl.2023.103934 [Google Scholar]

- Yousaf I, Patel R, and Yarovaya L (2022). The reaction of G20+ stock markets to the Russia–Ukraine conflict “black-swan” event: Evidence from event study approach. Journal of Behavioral and Experimental Finance, 35: 100723. https://doi.org/10.1016/j.jbef.2022.100723 [Google Scholar]

- Yousaf I, Riaz Y, and Goodell JW (2023a). The impact of the SVB collapse on global financial markets: Substantial but narrow. Finance Research Letters, 55(Part B): 103948. https://doi.org/10.1016/j.frl.2023.103948 [Google Scholar]

- Yousaf I, Riaz Y, and Goodell JW (2023b). What do responses of financial markets to the collapse of FTX say about investor interest in cryptocurrencies? Event-study evidence. Finance Research Letters, 53: 103661. https://doi.org/10.1016/j.frl.2023.103661 [Google Scholar]